403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Jewelry Market Size, Share, Growth, Analysis, Report, 2034

| Company | Investment/ Funding Value (USD) | Timeline (2025) | Key Activity |

|---|---|---|---|

| Grown Brilliance | USD 60 million | March 2025 | Secured growth capital to expand lab-grown diamond jewelry retail network and strengthen omnichannel distribution across North America. |

| VRAI | USD 50 million | May 2025 | Raised funding to scale lab-grown diamond production and expand AI-driven customization platforms for personalized jewelry design. |

| Blue Nile | USD 45 million | April 2025 | Investment directed toward digital platform enhancement and AI-based jewelry recommendation systems to improve online customer conversion. |

| CaratLane | USD 120 million | February 2025 | Expanded retail footprint and strengthened omnichannel jewelry ecosystem across tier-1 and tier-2 cities in India. |

| Market Metric | Details & Data (2025-2034) |

|---|---|

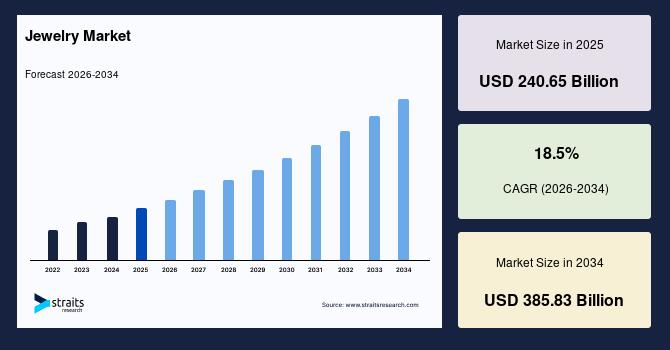

| 2025 Market Valuation | USD 240.65 Billion |

| Estimated 2026 Value | USD 242.22 Billion |

| Projected 2034 Value | USD 385.83 Billion |

| CAGR (2026-2034) | 18.5% |

| Study Period | 2022-2034 |

| Dominant Region | Asia Pacific |

| Fastest Growing Region | Europe |

| Key Market Players | Cartier (France), Graff Diamonds Limited (UK), Damas Jewellery (UAE), Titan Company (India), Malabar Gold and Diamonds Limited (India) |

Download Free Sample Report to Get Detailed Insights.

Jewelry Market Dynamics Market DriversRising Wedding & Cultural Ornament Cycles and Increasing Demand for Branded Certified Jewelry Drives Market

Wedding and cultural ornament cycles continue to play a strong role in shaping jewelry demand across regions. Traditional ceremonies, seasonal festivals, and family events create repeated purchase occasions throughout the year. Households allocate a significant share of spending toward gold and gemstone ornaments during these events. Social customs also encourage gifting of jewelry, strengthening consistent consumption patterns. As a result, jewelry market growth is supported by increasing wedding-related expenditure and cultural purchasing cycles.

The demand for branded and certified jewelry is rising as buyers prioritize trust, authenticity, and quality assurance in purchases. Hallmarking and certification systems help customers differentiate genuine products from imitations in a fragmented retail environment. Established brands are gaining preference due to consistent design standards and verified material sourcing. Retailers are also improving transparency through certification tags and digital authentication tools.

Certification Systems for Precious Metals, By Country

| Country | Certification System | Governing Authority | Details |

|---|---|---|---|

| India | BIS Hallmark | Bureau of Indian Standards (BIS) | Mandatory hallmarking for many gold jewelry categories. The hallmark includes BIS logo, purity/fineness mark, assay center mark, and HUID (Hallmark Unique Identification) code. |

| UK | UK Hallmarking System | Assay Office London, Birmingham Assay Office, Assay Office Edinburgh, Assay Office Sheffield | One of the world's oldest hallmarking systems. Precious metal articles must be independently tested and hallmarked by authorized assay offices before sale. |

| Switzerland | Swiss Precious Metal Control Mark | Central Office for Precious Metals Control | Precious metals are regulated under the Federal Act on the Control of Precious Metals. Official control marks verify fineness standards for precious metal products. |

| UAE | Dubai Central Laboratory Certification | Dubai Municipality | Gold and jewelry products are tested and certified through Dubai's precious metals quality-control framework, supporting Dubai's role as a major global gold trading hub. |

| Saudi Arabia | SASO Precious Metals Certification | Saudi Standards, Metrology and Quality Organization (SASO) | Precious metal products are subject to quality and purity verification requirements before entering the Saudi market. |

| China | National Jewelry and Jade Quality Supervision System | National Gemstone Testing Center (NGTC) | Precious metal jewelry is regulated through national quality supervision and purity-marking requirements. |

| Singapore | Singapore Assay & Hallmarking Scheme | Singapore Assay Office | Provides independent testing and hallmarking services for precious metal products including gold, silver, platinum, and palladium. |

| Australia | Voluntary Precious Metal Marking System | Industry-led certification and assay providers | Australia does not operate a mandatory national hallmarking regime. Jewelry is generally sold with manufacturer purity declarations and independent assay certification where required. |

| Canada | Precious Metals Marking Program | Competition Bureau Canada | Precious metal products must comply with fineness-marking requirements and consumer protection regulations governing purity claims. |

| US | FTC Precious Metals Compliance Framework | Federal Trade Commission (FTC) | No mandatory government hallmarking system. Jewelry purity claims must comply with FTC Guides for the Jewelry, Precious Metals, and Pewter Industries. |

| France | French Hallmarking System | French Customs and Assay Authorities | Precious metal products bear official hallmarks indicating metal type and fineness, with oversight from customs authorities. |

| Italy | Italian Precious Metal Hallmarking System | Italian Chamber of Commerce | Jewelry must carry a maker's identification mark and precious metal fineness mark in accordance with Italian regulations. |

| Turkey | Turkish Assay and Hallmarking System | Turkish Ministry of Trade and accredited assay institutions | Precious metal products are subject to purity testing and hallmarking requirements prior to commercialization. |

Market Restraints

Volatile Prices and Strict Hallmarking Compliance Requirements Restrain Market

Price fluctuations in gold, silver, and gemstones create uncertainty in jewelry production planning. Manufacturers face difficulty in maintaining stable product pricing across collections. Sudden cost increases reduce profit margins for retailers and wholesalers. Small and mid-sized players experience higher pressure due to limited hedging capacity. Consumer demand often shifts when retail prices change unexpectedly in short cycles. This instability affects long-term inventory planning and sourcing strategies across global markets.

Mandatory certification standards increase operational complexity for jewelry manufacturers and retailers. Additional testing and documentation processes extend product launch timelines. Compliance costs rise due to repeated quality verification procedures across regions. Smaller workshops often struggle to meet evolving regulatory benchmarks. Differences in hallmarking rules create coordination challenges for exporters.

Market Opportunities

Rising 3D Printing Prototyping and Expansion of Direct-to-Consumer Platforms Offer Growth Opportunities for Jewelry Market Players

A key jewelry market growth opportunity stems from 3D printing, which improves design development across manufacturing units. Designers can create detailed prototypes in shorter production cycles, reducing traditional development delays. This method helps in testing complex patterns before final casting, improving design accuracy. Small and mid-sized brands use this approach to reduce material wastage during early-stage production. Custom jewelry segments benefit from faster model adjustments based on customer feedback.

Direct-to-consumer jewelry platforms are increasing access between brands and end users without retail intermediaries. Consumers are exploring wider design collections through digital storefronts with simplified purchase processes. Brands are using online channels to present personalized collections and limited-edition pieces. This model helps reduce distribution layers and improves pricing transparency for buyers. Social media integration is supporting stronger customer engagement and brand visibility.

Market Challenges

Synthetic Diamond Price Disruption and Rising Online Counterfeit Risks Challenges Jewelry Market Growth

Synthetic diamonds are creating uneven pricing pressure across the jewelry value chain. Their lower production cost changes traditional pricing benchmarks in the luxury segment. Consumers start comparing lab-created stones with natural diamonds more frequently. This shift reduces the perceived exclusivity of natural stones in certain categories. Retailers face difficulty in maintaining stable margins due to rapid price adjustments.

Digital jewelry platforms are increasingly exposed to imitation product listings. Counterfeit sellers use similar visuals and branding styles to attract buyers. This creates confusion during online purchase decisions among customers. Trust issues grow when product authenticity becomes difficult to verify. Luxury brands face pressure to strengthen verification and traceability systems. The issue also affects customer confidence in e-commerce jewelry ecosystems.

Jewelry Regional Outlook Asia Pacific Jewelry MarketAsia Pacific: Market Dominance Led by Livestream Commerce for Jewelry Sales and Digital Gold Investment Platforms

The Asia Pacific jewelry market accounted for the largest regional share of 43.80% in 2025 due to strong cultural affinity toward gold and gemstone-based ornament ownership. Jewelry remains closely associated with weddings, festivals, gifting traditions, and long-term wealth preservation in several countries. Consumer spending on precious ornaments remains resilient despite fluctuations in economic conditions. The expanding retail networks and rising household incomes further strengthen market leadership.

China Jewelry MarketThe China jewelry market size was estimated at USD 123.5 billion in 2025 due to increasing penetration of livestream commerce for jewelry sales. Digital influencers and real-time product demonstrations allow brands to reach wider audiences while improving buyer confidence. According to the China Internet Network Information Center (CNNIC), China had over 800 million livestream commerce users, making it one of the largest digital retail ecosystems globally.

India Jewelry MarketThe India jewelry market size was estimated at USD 92.8 billion in 2025. The expansion of digital gold investment platforms supporting purchasing flexibility is contributing to market development. Consumers increasingly accumulate fractional gold through mobile applications and later convert holdings into physical jewelry purchases. According to the World Gold Council, India remains one of the world's largest gold-consuming countries, with annual gold demand exceeding 700 tons in recent years.

Europe Jewelry MarketEurope: Fastest Growth Driven by Precision-certified Jewelry Craftsmanship and Personalized Jewelry Customization Services

The Europe jewelry market is expected to grow at a CAGR of 6.12% during the forecast period, showcasing the fastest regional growth. The increasing influence of minimalist and lifestyle-based jewelry trends is shaping purchasing decisions across the region. Consumers are favoring versatile pieces suited for daily wear rather than occasion-specific ornaments. Contemporary aesthetics and understated luxury designs continue to gain popularity among younger demographics. Strong fashion industry influence and growing demand for sustainable jewelry collections further support regional market growth.

Germany Jewelry MarketThe Germany jewelry market size was estimated at USD 11.41 billion in 2025 due to a strong preference for precision-certified jewelry. Buyers place significant emphasis on quality assurance, manufacturing accuracy, and authenticated materials when making purchasing decisions. For example, Wellendorff continues to emphasize handcrafted precision and certified production standards. These characteristics strengthen consumer confidence and sustain demand for premium jewelry offerings.

UK Jewelry MarketThe UK jewelry market size was estimated at USD 10.20 billion in 2025. The increasing adoption of personalized jewelry customization services is supporting market expansion. Consumers are seeking engraved, bespoke, and made-to-order products that reflect individual preferences and gifting occasions. According to the UK's National Association of Jewellers (NAJ), customized and personalized jewelry categories have experienced growth as consumers increasingly value uniqueness in luxury purchases. For example, Pandora has expanded customizable charm and personalization offerings across the UK market.

France Jewelry MarketThe France jewelry market size was estimated at USD 8.91 billion in 2025, driven by the rising preference for heritage-inspired jewelry collections. Consumers are increasingly attracted to designs that reflect historical artistry, traditional craftsmanship, and iconic luxury aesthetics. According to the French luxury goods federation Comité Colbert, heritage and craftsmanship remain among the strongest purchase considerations within the country's luxury sector. This demand supports premium positioning and reinforces influence within the global jewelry industry.

Jewelry Market Segmentation Analysis By Product TypeRings accounted for the largest product type segment share of 32.17% in 2025. The growing demand for stackable and modular ring designs among younger consumers continues to support segment leadership. Buyers increasingly prefer combining multiple rings to create personalized looks that can be changed according to fashion preferences. Modular collections encourage repeat purchases because additional pieces can be added over time.

The earrings segment is projected to grow at a CAGR of 8.9% during the forecast period due to increasing demand for multiple-ear piercing trend. Consumers with several piercings often purchase different styles for coordinated ear arrangements, resulting in higher buying frequency. Fashion trends continue to promote layered ear styling using studs, hoops, and cuffs.

By Materrial type, gold jewelry accounted for a share of 48.26% in 2025. High liquidity and ease of resale through established bullion and jewelry networks remain important growth drivers where consumers value gold jewelry because it can be readily exchanged, pledged, or sold through widespread dealer networks. This accessibility reduces perceived financial risk associated with purchases.

The diamond jewelry segment is projected to register a CAGR of 6.12% during the forecast period due to expanding availability of innovative diamond cuts and contemporary settings. Manufacturers are introducing distinctive shapes, asymmetrical designs, and modern mounting techniques that appeal to evolving consumer preferences.

By Price RangeBy price range, mid-range jewelry accounted for a share of 56.33% in 2025 due to the expansion of organized retail and branded jewelry chains. The store expansion into emerging urban locations improves accessibility and brand visibility. Well-structured retail formats also enhance customer confidence by offering transparent purchasing experiences, after-sales services, and consistent quality standards, supporting sustained growth.

The luxury/premium jewelry segment is projected to grow at a CAGR of 10.5% during the forecast period, driven by growing interest in high-value collectibles featuring artistic craftsmanship. This is driving demand among affluent buyers, where consumers increasingly view exceptional jewelry pieces as wearable art that combines exclusivity with long-term value.

By Distribution ChannelBy distribution channel, offline retail is expected to grow at a CAGR of 18.11% during the forecast period. The availability of exclusive showroom collections and limited-edition pieces and physical stores offer curated displays that are often unavailable on digital platforms, attracting consumers seeking uniqueness in stores. Premium boutiques and brand outlets use exclusive designs to enhance footfall and purchase intent.

The online retail segment is projected to expand at a CAGR of 11.6% during the forecast period due to convenient access to exclusive online launches and digital-only collections. Consumers increasingly engage with platform-exclusive jewelry drops that are not available in physical stores. E-commerce channels enable instant browsing and purchasing across global catalogs.

By End UserThe women segment is expected to grow at a CAGR of 13.2% during the forecast period due to the expanding role of jewelry in daily lifestyle, and professional appearance styling continues to strengthen this dominance. Jewelry is increasingly used as an essential part of office wear, social events, and daily fashion expression. Brands are designing versatile collections that suit both formal and casual settings, enhancing purchase frequency.

The men segment is projected to grow at a CAGR of 7.9% during the forecast period, driven by the expansion of tailored designer collections. Jewelry brands are introducing rings, bracelets, chains, and cuff accessories designed with masculine aesthetics and minimal styling. This diversification is increasing acceptance among younger male consumers.

Competitive LandscapeThe jewelry market competitive landscape is moderately fragmented, with a mix of global luxury houses, branded jewelry retailers, regional chains, independent jewelers, and digital-first jewelry companies competing across diverse consumer segments. Established players compete primarily on brand heritage, craftsmanship, certification standards, exclusive collections, and retail network strength. Emerging companies focus on customization, lab-grown diamonds, direct-to-consumer sales models, and technology-enabled shopping experiences. Market participation is also increasing among niche brands specializing in sustainable sourcing and personalized designs. The jewelry market ecosystem is shaped by evolving consumer preferences and expanding online channels.

List of Key and Emerging Players in Jewelry Market-

Cartier (France)

Graff Diamonds Limited (UK)

Damas Jewellery (UAE)

Titan Company (India)

Malabar Gold and Diamonds Limited (India)

De Beers Group (UK)

LVMH (France)

Swarovski (Austria)

Kalyan Jewellers (India)

Pandora (Denmark)

September 2025: ORRA Fine Jewellery entered a collaboration with Salesforce to launch the ORRA Connected digital transformation initiative.

September 2025: Pandora announced the expansion of its North American operations through a new state-of-the-art distribution center in Maryland, US.

October 2025: Swarovski expanded its Creators Lab collaboration platform by partnering with seven global brands, including Oakley, PUMA, Off-White, and A Bathing Ape.

Report Scope| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 240.65 Billion |

| Market Size in 2026 | USD 242.22 Billion |

| Market Size in 2034 | USD 385.83 Billion |

| CAGR | 18.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Product Type, By Material Type, By Price Range, By Distribution Channel, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Jewelry Market Segments By Product Type-

Rings

Necklaces

Earrings

Bracelets

Pendants

Others

-

Gold Jewelry

Silver Jewelry

Platinum Jewelry

Diamond Jewelry

Gemstone Jewelry

Others

-

Luxury/Premium Jewelry

Mid-range Jewelry

Mass/Affordable Jewelry

-

Offline Retail

Online Retail

-

Men

Women

Children

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment