403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Inertial Navigation System Market Size, Share, Growth, 2034

| Company | Recent Activity | Timeline | Details | Value |

|---|---|---|---|---|

| Advanced Navigation | Series C Funding | March 2026 | Raised Series C funding to scale Positioning, Navigation and Timing (PNT) technologies and expand AI-enabled autonomous navigation systems for aerospace, defense, and robotics applications | USD 110 million |

| iNGage | Seed Funding | September 2025 | Secured seed funding to industrialize MEMS-based inertial navigation sensors for GNSS-denied autonomous systems, including INS/IMU applications | USD 7 million (€6 million) |

| Silicon Microgravity | Early-stage Funding | April 2025 | Raised funding to commercialize MEMS-based inertial and gravity sensors for navigation-grade applications in aerospace & defense markets | USD 3.7 million |

| Market Metric | Details & Data (2025-2034) |

|---|---|

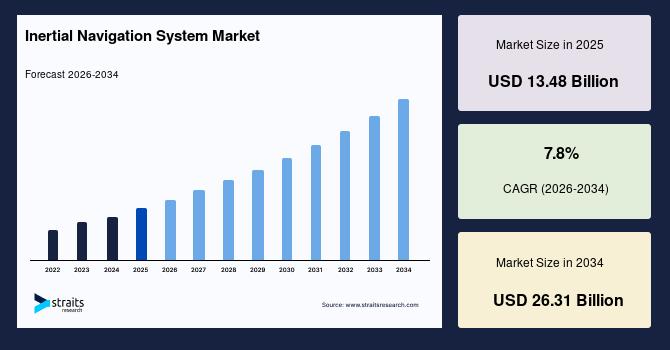

| 2025 Market Valuation | USD 13.48 Billion |

| Estimated 2026 Value | USD 14.42 Billion |

| Projected 2034 Value | USD 26.31 Billion |

| CAGR (2026-2034) | 7.8% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Honeywell International Inc. (US), Northrop Grumman Corporation (US), Lockheed Martin Corporation (US), Raytheon Technologies Corporation (US), Collins Aerospace (US) |

Download Free Sample Report to Get Detailed Insights.

Inertial Navigation System Market Dynamics Market DriversExpansion of Time-sensitive Networking in Mobility Systems and Demand from Hypersonic Vehicle Development Programs Drives Market

Growth of Time-Sensitive Networking (TSN) in aerospace and autonomous mobility systems is increasing demand for deterministic, low-latency communication across avionics and onboard vehicle networks. The IEEE 802.1DP aerospace TSN standard supports synchronized data exchange between inertial navigation systems, sensors, and flight controllers, improving navigation accuracy and real-time decision-making in UAVs and advanced aircraft platforms. TSN-based avionics architectures are also helping reduce communication delays and timing uncertainty in distributed flight systems.

The development of hypersonic vehicles is driving demand for ultra-high-precision inertial navigation systems capable of operating under extreme speed, acceleration, and thermal conditions where GNSS signals become unreliable. These platforms require continuous high-rate inertial updates to maintain stable guidance and trajectory control during Mach 5+ flight operations. Advanced INS architectures integrated with deterministic communication systems are being explored to minimize latency and improve navigation stability in mission-critical defense platforms.

Market RestraintsHigh Validation Requirements for Autonomous Systems and Complex Integration with Multi-sensor Architectures Restrain Market

High validation requirements for autonomous systems increase because inertial navigation systems must meet strict safety, reliability, and certification standards in aerospace, defense, and automotive applications. This process involves extensive simulation, field testing, redundancy checks, and long certification cycles before deployment approval. As a result, product development timelines become longer and compliance costs increase for manufacturers. This slows down the commercial rollout of advanced INS solutions, especially in emerging autonomous mobility platforms where rapid iteration is required.

Complex integration with multi-sensor architectures arises because modern navigation systems combine INS with GNSS, LiDAR, radar, vision sensors, and onboard computing units for higher accuracy. This requires precise synchronization, calibration, and software compatibility across multiple data streams to ensure consistent positioning output. The integration challenges increase system design complexity and raise engineering overhead for OEMs and system developers. This reduces adoption speed and creates barriers for smaller players in deploying advanced INS solutions in autonomous and connected platforms.

Market OpportunitiesExpansion in Smart Infrastructure Monitoring Systems and Integration with Digital Twin Ecosystems Offer Growth Opportunities for Market Players

Expansion in smart infrastructure monitoring systems increases as governments and private operators adopt advanced sensing technologies to improve the safety and efficiency of critical assets such as bridges, tunnels, railways, and dams. Inertial navigation systems are embedded into structural health monitoring solutions to detect micro-vibrations, displacement, and long-term structural shifts with high precision. This creates a new application scope for INS beyond aerospace and defense, particularly in civil engineering and smart city infrastructure management.

Integration with digital twin ecosystems is expanding as industries adopt virtual replicas of physical systems to improve monitoring, simulation, and operational efficiency. Inertial navigation systems provide real-time motion and orientation data that helps synchronise physical assets with their digital counterparts, improving simulation accuracy and predictive analytics. For example, INS data is used in aerospace digital twins for aircraft flight behavior modeling and in robotics for warehouse automation simulation. This strengthens system optimization, reduces maintenance downtime, and improves design validation across industrial and mobility applications.

Market ChallengesLimited Real-World Data for Algorithm Training and High Dependency on Continuous Firmware Optimization Challenges Market Growth

Limited real-world data for algorithm training arises because inertial navigation systems operating in extreme environments such as deep space, underwater, and high-speed defense platforms generate scarce and often non-standardized datasets. This restricts the ability of developers to train and validate AI-based navigation models under diverse operational conditions. Thus, the system performance may vary when deployed outside simulated environments, reducing confidence among end users. This slows the adoption of advanced INS solutions in emerging autonomous and safety-critical applications.

High dependency on continuous firmware optimization occurs because inertial navigation systems rely heavily on software algorithms to correct drift, calibrate sensors, and improve positioning accuracy in real time. This requires frequent updates, tuning, and system validation to maintain optimal performance across different platforms and operating conditions. However, continuous engineering support increases lifecycle complexity for manufacturers and end users. This reduces scalability and slows broader adoption, especially in cost-sensitive commercial and industrial applications.

Inertial Navigation System Regional Outlook North America Inertial Navigation System MarketNorth America: Market Dominance Led by Strong Defense Modernization Programs and Rising Investment in Sovereign Aerospace Capability

The North America inertial navigation system market accounted for the largest regional share of 37.18% in 2025 due to its strong ecosystem of aerospace, defense, and advanced mobility industries supported by continuous technological advancement and large-scale government programs. The region shows high deployment of inertial navigation systems in military aircraft, missiles, spacecraft, and autonomous platforms, driven by modernization initiatives and rising focus on GPS-denied navigation capability. The presence of major companies such as Honeywell and Northrop Grumman supports continuous innovation in high-precision navigation technologies. Strong investment in space exploration programs and increasing use of autonomous defense systems further strengthen demand.

US Inertial Navigation System MarketThe US inertial navigation system market size was estimated at USD 4.95 billion in 2025. The market is driven by strong defense modernization programs, rapid expansion of autonomous platforms, and increasing reliance on GPS-denied navigation technologies across aerospace and military systems. Demand is rising as INS is integrated into next-generation unmanned aerial systems and advanced mission-critical platforms. Honeywell's launch of its HGuide o480 single-card resilient inertial navigation system is designed for UAVs and autonomous systems to deliver high-accuracy navigation in compact form factors under GNSS-denied conditions. This reflects the growing shift toward resilient, software-enhanced navigation architectures in US defense and aerospace applications.

Canada Inertial Navigation System MarketThe Canada inertial navigation system market size was estimated at USD 0.58 billion in 2025 due to rising investment in sovereign aerospace capability, Arctic surveillance, and advanced dual-use navigation technologies. The country is strengthening its defense and aerospace research infrastructure to support autonomous systems and GPS-denied navigation environments. A major 2026 development is the National Research Council of Canada acquiring a Bombardier Global 6500 aircraft for defense and aerospace research, which will be used as a flying laboratory to test advanced navigation, sensing, and surveillance technologies. This initiative supports development of next-generation inertial navigation applications for extreme and remote operational conditions.

Asia Pacific Inertial Navigation System MarketAsia Pacific: Fastest Growth Driven by Defense Modernization and Growing Robotics Innovations

The Asia Pacific inertial navigation system market is expected to grow at a CAGR of 9.76% during the forecast period, showcasing the fastest regional growth due to rapid expansion of domestic aerospace production, increasing defense self-reliance programs, and strong investments in autonomous mobility technologies. Countries such as China, India, Japan, and South Korea are actively developing UAV ecosystems, advanced missile guidance systems, and next-generation satellite navigation infrastructure, which significantly increases demand for inertial navigation systems. Growth is also supported by large-scale industrial automation and robotics deployment across manufacturing and logistics sectors.

India Inertial Navigation System MarketThe India inertial navigation system market size was estimated at USD 1.05 billion in 2025 due to a strong focus on indigenous navigation capability, defense modernization, and expansion of satellite-based positioning systems. Demand is increasing across missile systems, UAVs, launch vehicles, and maritime platforms as the country pushes for self-reliant navigation technologies. For instance, the setback in the NavIC system after the failure of the IRNSS-1F satellite atomic clock, which reduced operational satellites below the required threshold for full PNT services, highlighted the need for advanced inertial backup systems in aerospace and defense applications.

Japan Inertial Navigation System MarketThe Japan inertial navigation system market size was estimated at USD 1.22 billion in 2025. The market is driven by advanced aerospace engineering capability, robotics innovation, and strong national investment in resilient satellite navigation systems. The country emphasizes high-precision navigation solutions for aviation, autonomous mobility, and space applications where accuracy and stability are critical. The completion of Japan's Quasi-Zenith Satellite System (QZSS), where the final“Michibiki” satellite launch scheduled for 2026 will complete a 7-satellite sovereign navigation constellation, improving positioning reliability and reducing dependency on external systems. This strengthens demand for INS integration in hybrid navigation architectures across aerospace and autonomous platforms.

China Inertial Navigation System MarketThe China inertial navigation system market size was estimated at USD 3.25 billion in 2025. The market is expanding due to strong domestic navigation ecosystem development, large-scale defense modernization, and rapid deployment of autonomous systems across multiple industries. Growing emphasis on self-reliant positioning technologies is accelerating integration of inertial navigation systems with satellite-based navigation frameworks to ensure continuous performance in signal-degraded environments. Expanding UAV manufacturing capacity and high adoption of intelligent transportation systems further strengthen demand for compact and high-precision INS solutions.

Inertial Navigation System Market Segmentation Analysis By Material TypeBy material type, composite materials accounted for the largest share of 34.28% in 2025 due to their superior strength-to-weight ratio, thermal stability, and resistance to vibration and harsh operating conditions. These materials support the structural integrity of high-precision navigation components used in aerospace, defense, and space applications. Their ability to reduce overall system weight while maintaining durability makes them highly suitable for advanced inertial sensors and housings.

The plastic segment is projected to grow at a CAGR of approximately 9.82% during the forecast period due to its increasing use in lightweight and cost-efficient inertial navigation system components. Advances in high-performance engineering plastics are enabling better thermal resistance and mechanical stability, making them suitable for non-critical and commercial navigation applications.

By Technology TypeBased on technology type, the ring laser gyroscope (RLG) segment accounted for the largest share of 36.74% in 2025 due to its exceptional accuracy, stability, and reliability in high-performance navigation environments. It is widely used in aerospace, defense, and space systems where long-duration precision and resistance to external interference are critical.

The micro-electro-mechanical system s (MEMS) segment is projected to grow at a CAGR of 10.64% during the forecast period because of its compact size, low power consumption, and scalability for mass production. MEMS-based inertial navigation systems are increasingly used in drones, autonomous vehicles, and portable robotics where lightweight and cost-efficient solutions are essential.

By ComponentBy component, inertial measurement units (IMUs) accounted for a share of 33.62% in 2025, as they serve as the core sensing module combining accelerometers and gyroscopes into a single integrated unit. IMUs provide essential motion data required for navigation, stabilization, and guidance across aerospace, defense, and autonomous systems. Their ability to deliver real-time orientation and velocity information makes them indispensable in modern INS architectures.

The software & algorithms segment is projected to grow at a CAGR of 11.22% during the forecast period due to increasing reliance on advanced computational models for improving navigation accuracy and reducing sensor drift. Modern INS solutions depend heavily on real-time data processing, sensor fusion, and adaptive correction techniques to enhance performance.

By PlatformBy platform, airborne platforms accounted for a share of 41.86% in 2025 due to extensive use in commercial aviation, military aircraft, UAVs, and space launch systems. Airborne applications require highly reliable and precise navigation solutions to ensure stability, guidance, and safety during complex flight operations. INS plays a critical role in maintaining accurate positioning in environments where external signals may be unreliable or unavailable.

The space platform segment is expected to grow at a CAGR of 10.95% during the forecast period due to rising deployment of satellites, deep-space missions, and reusable launch systems. Inertial navigation systems are essential for maintaining orientation, trajectory control, and stability in space environments where external navigation signals are unavailable. Increasing focus on satellite constellations and space exploration programs is driving rapid adoption of advanced inertial technologies.

By GradeBy grade, the navigation grade segment accounted for a share of 38.27% in 2025 due to its widespread use in commercial aviation, marine systems, and industrial navigation applications. It provides a balance between high accuracy and operational cost, making it suitable for large-scale deployment across multiple industries. Navigation-grade systems ensure stable performance over extended periods and are widely integrated into modern transportation and mobility platforms.

The space-grade segment is expected to grow at a CAGR of 10.48% during the forecast period due to increasing demand for high-precision inertial navigation in satellite systems, orbital missions, and deep-space exploration. These systems are designed to operate in extreme conditions with minimal drift and maximum reliability. Rising investments in space infrastructure and exploration programs are accelerating the adoption of advanced space-grade INS technologies.

By End UserBy end user, aerospace & defense accounted for a share of 47.92% in 2025 due to extensive use of high-precision navigation systems in aircraft, missiles, spacecraft, and military vehicles. These applications require continuous, reliable, and highly accurate positioning in environments where external navigation signals may be unavailable or compromised. INS is a core component in guidance, control, and mission-critical operations. Strong integration across defense modernization programs and aviation platforms reinforces its dominant position.

The industrial and robotics segment is expected to grow at a CAGR of 11.08% during the forecast period due to increasing adoption of automation in manufacturing, logistics, warehousing, and autonomous systems. INS enables precise motion tracking and positioning in environments where GPS signals are weak or unavailable. The rise of intelligent robots and automated industrial systems is driving strong demand for compact and cost-efficient navigation solutions.

Competitive LandscapeThe inertial navigation system market landscape is moderately consolidated, with a combination of established aerospace and defense electronics companies, specialized navigation system manufacturers, and emerging sensor and MEMS technology firms. Large players such as global aerospace corporations and advanced defense contractors compete alongside niche technology developers and component-level suppliers focusing on MEMS sensors and software-based navigation solutions. Emerging players in the inertial navigation system market ecosystem focus on miniaturized designs, cost-efficient MEMS-based solutions, rapid prototyping, and software-driven navigation improvements to address commercial and autonomous system demand.

List of Key and Emerging Players in Inertial Navigation System Market-

Honeywell International Inc. (US)

Northrop Grumman Corporation (US)

Lockheed Martin Corporation (US)

Raytheon Technologies Corporation (US)

Collins Aerospace (US)

Safran Electronics & Defense (France)

Thales Group (France)

BAE Systems plc (UK)

Leonardo S.p.A. (Italy)

L3Harris Technologies Inc. (US)

Analog Devices Inc. (US)

Bosch Sensortec GmbH (Germany)

KVH Industries Inc. (US)

Teledyne Technologies Incorporated (US)

VectorNav Technologies LLC (US)

March 2026: Honeywell introduced the HGuide i700, a compact inertial measurement unit designed for unmanned aerial, land, and marine systems operating in GNSS-denied environments.

January 2026: VIAVI Solutions' Inertial Labs introduced IRINS, a Low Earth Orbit (LEO)-aided inertial navigation system designed for operation across land, air, and sea in denied, degraded, and disrupted space environments.

December 2025: Safran Federal Systems' Skynaute inertial navigation system was selected by Moog Inc. for integration into the Hercules avionics suite. The system enhances navigation performance in contested and GPS-denied environments, reinforcing demand for high-precision fiber-optic gyro-based INS solutions in defense aviation.

Report Scope| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13.48 Billion |

| Market Size in 2026 | USD 14.42 Billion |

| Market Size in 2034 | USD 26.31 Billion |

| CAGR | 7.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Material Type, By Technology Type, By Component, By Platform, By Grade, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Inertial Navigation System Market Segments By Material Type-

Plastic

Copper

Stainless Steel

Brass

Cast Iron

Composite Materials

-

Mechanical Inertial Navigation

Ring Laser Gyroscope (RLG)

Fiber Optic Gyroscope (FOG)

Micro-Electro-Mechanical Systems (MEMS)

-

Accelerometers

Gyroscopes

Inertial Measurement Units (IMUs)

Processing Units (Navigation Computers)

Software & Algorithms

-

Airborne

Land

Naval

Space

-

Marine Grade

Tactical Grade

Navigation Grade

Space Grade

-

Aerospace & Defense

Automotive

Marine & Shipping

Industrial & Robotics

Oil & Gas

Consumer Electronics

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment