403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Soybean Meal Market Size, Share, Growth, Analysis, Report, 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

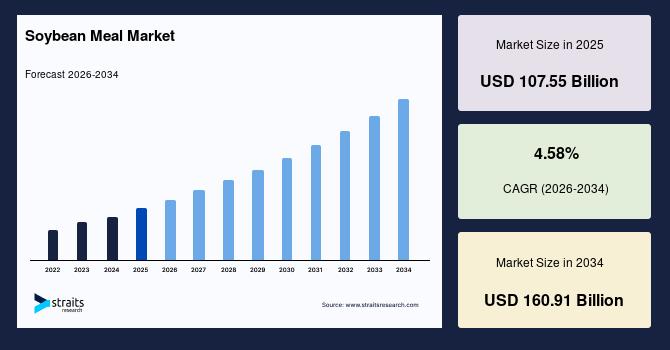

| 2025 Market Valuation | USD 107.55 Billion |

| Estimated 2026 Value | USD 112.47 Billion |

| Projected 2034 Value | USD 160.91 Billion |

| CAGR (2026-2034) | 4.58% |

| Study Period | 2022-2034 |

| Dominant Region | Asia-Pacific |

| Fastest Growing Region | North America |

| Key Market Players | Bunge Limited, Archer Daniels Midland Company (ADM), Cargill Incorporated, Louis Dreyfus Company B.V., COFCO International |

Download Free Sample Report to Get Detailed Insights.

Soybean Meal Market Growth Factor Rising Demand for High-Protein Animal FeedSoybean meal is a rich protein and essential amino acid source, making it an ideal feed ingredient for livestock, poultry, and aquaculture. As populations expand and incomes rise, particularly in Asia-Pacific and Latin America, animal farming intensifies to meet dietary shifts toward protein-rich foods.

-

For instance, the USDA's January 2025 outlook highlighted that U.S. soybean meal exports are projected at 15.8 million tons in 2024/25, representing about 20.9% of global trade. This export surge reflects expanding domestic crush capacity and increasing usage of soybean meal in U.S. livestock feed, where lower meal prices have boosted inclusion rates in diets for dairy, beef, swine, and poultry.

Additionally, its digestibility and affordability make it a preferred alternative to fishmeal in aquaculture. Feed manufacturers increasingly blend soybean meal in compound feed to ensure rapid growth, efficient conversion, and animal health.

Market Restraint Volatility in Soybean Prices and Supply Chain DisruptionsThe ongoing volatility in global soybean prices, compounded by geopolitical risks, climate uncertainties, and logistical disruptions, restricts market growth. Soybean meal is derived from crushed soybeans; its pricing is directly tied to raw soybean futures, making it highly susceptible to shifts in commodity markets. In 2025, extreme weather conditions, including severe droughts in Brazil and flooding in parts of the U.S. Midwest, have disrupted crop yields and export schedules, leading to inconsistent supply and price spikes.

Simultaneously, growing geopolitical tensions involving major exporters like Argentina and Brazil have further stressed trade flows. These fluctuations have created cost unpredictability for feed manufacturers, who often operate on thin margins and require stable input pricing for long-term feed contracts.

Market Opportunity Strategic Sourcing of Eudr-Compliant Soy in Aquaculture FeedAn opportunity in the soybean meal market lies in strategically sourcing soy that meets the European Union's new anti-deforestation requirements (EUDR), particularly for aquaculture feed suppliers serving the Western Mediterranean. This approach supports regulatory alignment and operational efficiency while catering to sustainability-conscious buyers.

-

In April 2025, BioMar, a global aquafeed producer in the Western Mediterranean, announced it had successfully shifted soybean sourcing to European suppliers whose production meets the EU Deforestation Regulation and BioMar's internal 2030 sustainability agenda. This transition involved formula adjustments and supply-chain adaptations to integrate compliant soy without compromising nutritional quality or performance standards.

As aquaculture grows, relying increasingly on plant-based proteins, the ability to blend sustainability compliance with feed efficiency positions soybean meal suppliers at the forefront of industry transformation.

Regional AnalysisAsia-Pacific stands out as the leading region in the global market for soybean meal, primarily fueled by growing demand for animal nutrition across rapidly expanding poultry, aquaculture, and livestock industries. The area benefits from rising per capita meat consumption, increasing investment in feed manufacturing, and efforts to modernise agricultural supply chains. Widespread feed sector modernisation, growing regional trade networks, and public-private partnerships accelerate market development. Countries across the region are increasingly adopting high-efficiency feed formulations, driving consistent demand for soybean meal.

-

China continues to be the world's largest consumer and importer of soybean meal, driven by its massive feed demand across the poultry, swine, and aquaculture industries. In response to U.S. trade tensions, China has diversified its import portfolio by securing long-term contracts with Brazil and Argentina. State-owned COFCO and other crushers also invest in refining soybean meal quality with lower fiber content to meet updated feed standards. Government efforts to curb livestock farming emissions have encouraged using precision-formulated meals to optimise feed efficiency. China is also piloting import substitution models in provinces like Heilongjiang to stimulate domestic soybean production.

India's market for soybean meal is expanding rapidly, fueled by a growing demand for affordable animal protein and evolving livestock farming practices. According to a July 2025 update from the Solvent Extractors' Association (SEA), soybean meal exports have rebounded due to higher global demand and improved crushing margins. Domestically, demand from the poultry sector, particularly in southern and western states, continues to rise, supported by government incentives for feed modernisation. Indian feed manufacturers are gradually shifting toward standardised formulations, integrating soybean meal with performance-enhancing micronutrients.

North America maintains a significant position in the soybean meal market due to its highly integrated production-to-distribution ecosystem. The region's advanced oilseed processing infrastructure and a well-established animal farming sector ensure stable and consistent demand for soybean meal across the poultry, swine, and cattle industries. Additionally, the region's strategic role in international trade, especially during global supply chain disruptions, reinforces its influence as a supplier and stabilising force in the global soybean meal value chain. North America's commitment to feed quality, compliance with global safety standards, and transparent trading practices further bolsters its reputation in international markets.

-

The U.S. remains a cornerstone of the global soybean meal industry, backed by high-capacity crushing plants, extensive soybean cultivation, and a mature feed manufacturing industry. Companies such as ADM and Bunge have continued to optimise feed formulations with enhanced amino acid profiles, increasing value-added product exports. Additionally, the U.S. reinforces trade links with Mexico and Southeast Asia, helping stabilise supply amid global logistics volatility. The rise of speciality non-GMO and organic soybean meal segments is gaining traction, particularly in premium feed markets. Technological investments in precision crushing and protein standardisation further enhance product consistency for export-focused suppliers.

Canada is gradually expanding its role in the soybean meal value chain, supported by rising investments in oilseed processing and livestock exports. The Canadian livestock sector, especially in Quebec and Manitoba, drives steady soybean meal consumption due to shifts toward high-protein poultry diets. Moreover, Canada's alignment with U.S. biosecurity and trade protocols ensures minimal disruption in cross-border meal shipments. Provincial initiatives support feed research partnerships between academia and industry, encouraging trials of enriched soybean meal blends. Increased rail connectivity to port terminals enables better access to Asian export destinations.

Latin America is a key production and export engine for the global market for soybean meal. The region benefits from favourable agroclimatic conditions, expansive arable land, and a high concentration of commercial-scale oilseed processors. Its competitive edge lies in large-scale export-oriented supply chains directly linking to major global markets. Infrastructure investments and supportive government measures have strengthened the region's ability to maintain high-volume output while navigating external economic or logistical challenges. Latin America's focus on meeting international sustainability standards and offering traceable, non-GMO alternatives also positions it favorably among health- and environment-conscious importers.

-

Brazil is a top producer of soybeans and a key global exporter of soybean meal, supported by advanced crushing operations and strong trade relations with Asia and Europe. In May 2025, Abiove reported a significant uptick in soybean meal exports, particularly to Southeast Asia, amid rising demand from feed mills in Vietnam and Indonesia. Domestically, Brazil's poultry and pork industries are also scaling up, keeping internal meal demand robust. Infrastructure improvements in port logistics and railway networks further strengthen Brazil's role as a reliable global supplier. Regional crushing hubs like Mato Grosso and Paraná are seeing expanded capacity with the help of foreign agri-investments.

Mexico is emerging as a high-growth market for soybean meal imports, driven by expanding poultry, swine, and aquaculture sectors. While the country relies heavily on U.S. soybean meal imports, it has begun exploring secondary trade routes through South American suppliers. Rising domestic demand is prompting new feed mill investments in central and western Mexico, enhancing the overall absorption capacity for high-protein meal formulations. Feed associations are pushing for improved nutritional labelling and ingredient traceability, which is reshaping procurement strategies. Growing urban meat demand further intensifies the need for higher-quality meal blends across regional distribution centres.

Conventional soybean meal continues to lead the product category due to its high protein concentration and widespread availability from large-scale oilseed crushers. This meal type is typically produced using solvent extraction methods, which yield higher output volumes suitable for commercial-scale feed formulations. Its consistent amino acid profile and digestibility make it the standard choice for feed manufacturers catering to poultry, aquaculture, and livestock segments. The versatility of conventional soybean meal lies in its adaptability to different feed blends and nutritional enhancement processes. Its availability in bulk packaging further simplifies logistics for industrial-scale users.

Application InsightsAnimal feed remains the most prominent application segment in the soybean meal industry, accounting for most global consumption. Soybean meal is foundational in the livestock industry as a cost-effective, protein-rich feed component supporting muscle development, growth rate, and reproductive efficiency across species. Its inclusion is especially dominant in poultry and pig farming, where performance metrics such as feed conversion ratio are tightly monitored. With rising meat consumption in emerging economies, feed demand is expected to grow steadily, particularly in Asia and Africa. Additionally, government-backed livestock development programs often rely on soybean meal as a dependable protein base.

Nature InsightsGenetically modified (GM) soybean meal holds the largest share under this category, owing to the dominance of GM soybean cultivation in key producing countries like the U.S., Brazil, and Argentina. GM soybean meal offers several logistical and agronomic advantages, including higher crop yields, pest resistance, and reduced herbicide use during cultivation. These factors lower production costs and improve global supply stability. From a feed manufacturing standpoint, GM meals exhibit no significant nutritional difference from their non-GM counterparts, but their pricing is typically more competitive due to efficiency gains across the value chain. GM soybean meal remains the default protein base for many commercial feed brands, especially in cost-sensitive markets due to availability, scalability, and pricing predictability.

Distribution Channel InsightsDirect procurement dominates the distribution model for soybean meal, especially among large-scale feed manufacturers and integrated poultry or livestock operations. These buyers typically source bulk quantities directly from oilseed crushers or commodity traders to ensure volume consistency and pricing leverage. This tiered channel structure helps bridge the gap between producers and end-users in fragmented markets. Increasingly, digital procurement platforms and online agri-marketplaces are gaining traction in some countries, offering price transparency and streamlined logistics, particularly for mid-sized buyers seeking contract flexibility and traceable sourcing.

End-User InsightsPoultry farming emerges as the dominant end-use segment, driven by the growing global demand for broiler meat and eggs. Soybean meal is a key input in poultry feed formulations because of its digestibility, palatability, and strong lysine content, an amino acid crucial for muscle formation. In broiler and layer operations, soybean meal helps maintain high growth rates and egg production cycles. The poultry sector's reliance on soybean meal is reinforced by the need for predictable nutritional performance, which this ingredient consistently delivers, making it a staple in feed mill formulations worldwide. Large integrators and vertically integrated poultry producers are increasingly standardising feed formulations to include soybean meal as the core protein base.

Company Market ShareThe soybean meal market share is moderately consolidated, with global agribusiness giants controlling a substantial share of processing and international trade, especially across North and South America. Integrated crushing capacity, long-term trade agreements, and robust infrastructure across export corridors drive the growth. These companies serve livestock feed manufacturers, commercial poultry producers, aquaculture farms, and international commodity buyers across Asia-Pacific, Latin America, and the EU.

Bunge Global SA is a leading agribusiness and food company with global operations spanning over 40 countries. Headquartered in Switzerland with U.S. operations based in Missouri, Bunge specialises in oilseed processing, grain trading, and producing plant-based oils, protein meals, and bioenergy. The company is actively expanding its renewable feedstock capabilities through a joint venture with Chevron and recently completed a $34 billion merger with Viterra in July 2025.

-

In March 2024, Bunge Chevron Ag Renewables LLC, a 50/50 joint venture, broke ground on a new oilseed processing plant in Destrehan, Louisiana. The facility is expected to begin operations in 2026 and will handle soybeans and other oilseeds for renewable diesel feedstock and high-protein soybean meal used in animal nutrition. This investment supports Bunge's crushing network in the U.S. and Brazil, reinforcing its strategy to align sustainable fuel supply with feed market growth.

-

Bunge Limited

Archer Daniels Midland Company (ADM)

Cargill Incorporated

Louis Dreyfus Company B.V.

COFCO International

AG Processing Inc (AGP)

Olam Agri Holdings Pte Ltd

Wilmar International Limited

Sodrugestvo Group S.A.

Vicentin S.A.I.C.

Groupe Avril

GrainCorp Limited

Noble Agri (now part of COFCO)

Seara Alimentos (part of JBS S.A.)

Tianjin Bohai Seed Group Co., Ltd.

-

July 2025- ARISE Integrated Industrial Platforms, through its subsidiary Benin Agri Business, became the first African company to receive ProTerra Level III certification for soybean production, covering both soybean meal and related products. This globally recognised certification denotes deforestation-free sourcing, climate-smart agriculture, fair labour practices, and full supply chain traceability from farm to terminal delivery.

July 2025- China's General Administration of Customs officially approved soybean meal imports from Ethiopia, effective July 3, 2025. This groundbreaking decision, China's first inclusion of a non-traditional supplier under strict phytosanitary standards, forms part of a strategic drive to diversify its feed protein sources amid mounting trade tensions, aiming to reduce dependence on traditional exporters like the U.S. and Brazil.

April 2025- French engineering firm Morillon Systems completed the commissioning of a state-of-the-art soybean meal storage and unloading system at CPF Group's feed facility in Bangkok, Thailand. The installation includes a 10-meter-diameter silo fitted with Morillon's advanced Hydrascrew reclaimer, designed to improve unloading efficiency and ensure a consistent flow of meal used in livestock and aquaculture feed production.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 107.55 Billion |

| Market Size in 2026 | USD 112.47 Billion |

| Market Size in 2034 | USD 160.91 Billion |

| CAGR | 4.58% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Product Type, By Application, By Nature, By Distribution Channel, By End-User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Soybean Meal Market Segments By Product Type-

High-Protein Soybean Meal

Conventional Soybean Meal

Dehulled Soybean Meal

Organic Soybean Meal

Low-Oligosaccharide Soybean Meal (LO-SBM)

-

Poultry Feed Formulation

Cattle and Dairy Nutrition

Aquaculture Feed

Pet Food Ingredient

Industrial Fermentation & Enzyme Production

Bio-Based Adhesives and Bioplastics

-

Genetically Modified (GM) Soybean Meal

Non-GMO Soybean Meal

Organic Certified Soybean Meal

-

Bulk Commodity Traders

Feed Ingredient Distributors

Direct Sales to Feed Manufacturers

Online Feed Marketplaces

Agri-Cooperatives & Grower Associations

-

Commercial Livestock Producers

Integrated Poultry & Dairy Operations

Aquafeed Manufacturers

Pet Food Processing Companies

Agro-Industrial Biofactories

Export-Oriented Feed Suppliers

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment