403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Butter Packaging Market Size, Share, Growth, Forecast, 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

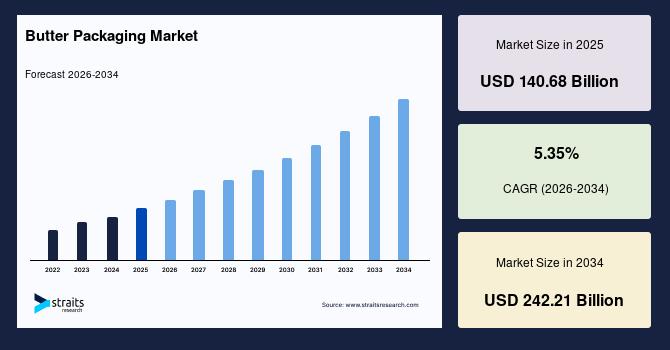

| 2025 Market Valuation | USD 140.68 Billion |

| Estimated 2026 Value | USD 160.15 Billion |

| Projected 2034 Value | USD 242.21 Billion |

| CAGR (2026-2034) | 5.35% |

| Study Period | 2022-2034 |

| Dominant Region | Europe |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Arla Foods, Fonterra Co-operative Group, Lactalis Group, Land O'Lakes, Amul (GCMMF) |

Download Free Sample Report to Get Detailed Insights.

Market Driver Rising Global Consumption of ButterThe global butter packaging market is driven by increasing butter consumption across households, foodservice, and industrial sectors. Changing dietary habits, growing bakery and confectionery industries, and the rising popularity of butter in processed foods are contributing to sustained demand.

-

For instance, in July 2025, butter production in the United States reached 180.1 million pounds, marking a 9.8% increase compared to July 2024. Although this represents a slight 4.4% decrease from June 2025 levels, international demand remains robust across regions, reflecting a steady global appetite.

This growing consumption drives the need for innovative, convenient, and protective butter packaging solutions to maintain freshness and meet consumer expectations worldwide.

Market Restraint Environmental Concerns and Regulatory ComplianceThe global market faces restraints due to rising environmental concerns and strict regulatory requirements on food-grade packaging. Conventional plastic-based wraps and containers contribute to waste, prompting pressure for sustainable alternatives. However, shifting to eco-friendly solutions often raises production costs and demands technological upgrades.

Moreover, compliance with global food safety standards and labeling regulations adds complexity for manufacturers, particularly in emerging markets. These challenges hinder the rapid adoption of innovative packaging solutions, slowing overall market growth despite strong consumer and industry demand for sustainable practices.

Market Opportunity Demand for Biodegradable and Eco-Friendly Packaging MaterialsThe global butter packaging market is witnessing growing opportunities due to rising consumer awareness about environmental sustainability. Increasing concerns over plastic waste and stringent regulations on single-use plastics are encouraging manufacturers to adopt biodegradable and eco-friendly packaging solutions.

-

For instance, in March 2025, Novolex's compostable butter wraps, TerreGlossTM and TerrecoteTM, received the Flexible Packaging Association's Gold Award for Sustainability and earned certification from the Biodegradable Products Institute (BPI) for commercial composability. This highlights the industry's shift toward environmentally responsible materials.

Such innovations enable brands to cater to eco-conscious consumers while complying with regulatory standards, driving long-term growth, and opening avenues for sustainable packaging adoption globally.

Regional AnalysisEurope dominates the butter packaging market with a share of over 35%, due to strong dairy production, established processing facilities, and high consumer demand for premium packaged dairy products. The region emphasizes eco-friendly and recyclable packaging, aligning with strict sustainability regulations and consumer preferences. Innovation in flexible packs, paper wraps, and portion-controlled units is widely adopted to reduce waste and extend shelf life. Leading packaging manufacturers collaborate with dairy cooperatives and retail chains to introduce advanced barrier films and biodegradable solutions, ensuring longer freshness while supporting Europe's circular economy goals.

The UK butter packaging market is shaped by rising consumer preference for sustainable and recyclable options, driving demand for paper-based wraps and compostable films. With butter consumption remaining steady, manufacturers focus on attractive, portion-sized packs to meet modern lifestyle needs. Major players like DS Smith and Amcor are investing in lightweight, eco-conscious solutions to cater to retail and foodservice channels.

Germany's butter packaging industry is characterized by advanced technological integration and a strong push toward sustainable solutions. With dairy being a central segment of the food industry, packaging companies are investing in biodegradable films, aluminum alternatives, and recyclable laminates. Firms like Huhtamaki and Mondi play a significant role, offering innovative packaging formats tailored to both retail and bulk distribution.

Asia-Pacific Market TrendsAsia-Pacific is witnessing rapid growth in the butter packaging market, fueled by rising dairy consumption, urbanization, and the expansion of modern retail formats. Increasing adoption of Western-style diets boosts butter sales, encouraging investments in advanced packaging to preserve quality in hot and humid climates. Flexible pouches, foil wraps, and resealable tubs are gaining traction, while sustainable materials are gradually entering the market. Moreover, regional players collaborate with global packaging firms to bring cost-effective and innovative designs, ensuring affordability and convenience for diverse consumer bases.

China's butter packaging market is expanding as consumer demand for bakery products and Western-style dairy items rises. Packaging companies like Greatview and international players such as Tetra Pak are introducing innovative formats, including portion packs and resealable tubs, to cater to growing urban households. Sustainability initiatives are slowly gaining ground, with biodegradable films and recyclable wraps entering premium product lines.

India's market for butter packaging is growing steadily, driven by the popularity of brands like Amul and Mother Dairy, which rely on durable, cost-effective packaging to serve a vast consumer base. Foil wraps and laminated paper remain dominant, but rising awareness of sustainability is pushing interest in recyclable options. Packaging firms are also focusing on portion-controlled packs for urban markets and bulk formats for hotels and food services.

Packaging Type InsightsFoil/paper-wrapped butter blocks lead the market with the highest share of more than 30% by packaging type, due to their ability to preserve freshness, maintain shape, and protect against air and light exposure. This traditional format is preferred by both consumers and foodservice providers for its convenience, portioning flexibility, and compatibility with labeling and branding. The packaging also supports sustainability trends when made from recyclable or responsibly sourced materials, making it a reliable choice for both household use and large-scale commercial applications.

Product Type InsightsThe organic butter segment holds the dominant position, while the organic & plant-based butter segment is projected to record the fastest CAGR of 5.23%, as consumers increasingly prefer natural, chemical-free, and sustainably produced dairy products. Growing health awareness, coupled with demand for premium and traceable food items, drives the popularity of organic butter. Packaging for this segment often emphasizes eco-friendliness, premium aesthetics, and freshness preservation, ensuring both quality and brand appeal. Organic butter's dominance reflects a shift toward healthier and environmentally conscious consumer choices globally.

Distribution Channel InsightsSupermarkets and hypermarkets lead the butter packaging market, accounting for over 50% share, offering widespread accessibility and convenient shopping for consumers. These large-format stores provide a wide variety of butter types, sizes, and packaging options, catering to both regular households and premium buyers. Attractive packaging, promotions, and bulk options enhance visibility and sales. Their dominance is supported by organized retail growth in emerging markets and the ability to efficiently handle high-volume distribution while maintaining product quality and safety.

End Use InsightsThe bakery and confectionery sector dominates butter consumption due to high demand for consistent quality, precise portioning, and specialized packaging solutions. Butter is a critical ingredient in pastries, cakes, cookies, and chocolates, where freshness and performance directly impact product quality. Innovative packaging formats like blocks, tubs, and resealable packs help maintain functionality in industrial settings. The segment's growth is driven by increasing bakery production globally and rising demand for premium and artisanal baked goods.

Company Market ShareCompanies are actively focusing on expanding product portfolios with sustainable and recyclable solutions, catering to rising consumer demand for eco-friendly options. Many are investing in advanced barrier films, lightweight materials, and portion-controlled formats to enhance convenience and reduce waste. Collaborations with dairy producers and retailers are common, helping firms introduce innovative designs that improve shelf life, brand appeal, and compliance with regional sustainability regulations.

Arla Foods was established in 2000 through the merger of Arla, a Swedish dairy cooperative, and MD Foods, a Danish cooperative, with headquarters in Viby, Denmark. It is one of the world's largest dairy companies, owned by over 8,000 farmers. Arla specializes in milk, cheese, butter, and cream production, with a strong focus on sustainability. The company actively develops eco-friendly packaging and invests in innovation to meet global dairy demand while reducing environmental impact.

-

In April 2025, Arla Foods and Germany's DMK Group plan to merge, forming Europe's largest dairy cooperative with over 12,000 member-farmers. The combined annual revenue is expected to reach about €19 billion. The new company will use the Arla name, be headquartered in Denmark, and is subject to regulatory and board approvals by the end of 2025.

-

Arla Foods

Fonterra Co-operative Group

Lactalis Group

Land O'Lakes

Amul (GCMMF)

Dairy Farmers of America

Ornua (Kerrygold)

Saputo Inc.

Kerry Group

Organic Valley

Danone

Unilever (Flora, Becel)

Nestlé S.A.

President (under Lactalis)

Anchor (under Fonterra)

Horizon Organic

Vermont Creamery

-

In April 2025, ProAmpac introduced its Butter Fresh Parchment and foil-paper-based packaging solutions, specifically designed to protect butter, margarine, and other oil-based solid products. These innovative options preserve freshness, maintain dead-fold properties, and minimize air exposure, effectively extending shelf life.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 140.68 Billion |

| Market Size in 2026 | USD 160.15 Billion |

| Market Size in 2034 | USD 242.21 Billion |

| CAGR | 5.35% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Packaging Type, By Product Type, By Distribution Channel, By End Use |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Butter Packaging Market Segments By Packaging Type-

Foil/Paper-Wrapped Blocks

Butter Sticks (wrapped or unwrapped)

Tubs (plastic, compostable, biodegradable)

Resealable Pouches

Cartons/Boxes

Jars (glass/plastic)

Squeeze Tubes

Others (e.g., Bag-in-box systems, single-serve pods)

-

Salted Butter

Unsalted Butter

Cultured Butter

Clarified Butter (Ghee)

Flavored/Herb Butter

Organic Butter

Plant-Based Butter

Reduced-Fat/Lite Butter

Others (e.g., Whey Butter, Spreadable Blends)

-

Supermarkets/Hypermarkets

Convenience Stores

Online Retail/E-commerce

Foodservice Distributors

Specialty/Deli Stores

Others (e.g., Institutional/Bulk Purchase Programs, Direct-to-Consumer Subscriptions)

-

Household/Retail

Foodservice (Restaurants, Cafés, Hotels)

Bakery & Confectionery Industry

Dairy Processing Facilities

Meal Kit Services

Others (e.g., Airline Catering, Institutional Kitchens)

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment