403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Hemostats Market Size, Share, Growth, Analysis, Report, 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

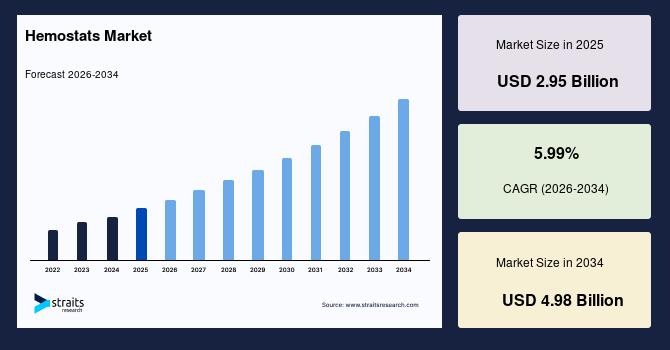

| 2025 Market Valuation | USD 2.95 Billion |

| Estimated 2026 Value | USD 3.13 Billion |

| Projected 2034 Value | USD 4.98 Billion |

| CAGR (2026-2034) | 5.99% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Johnson & Johnson (Ethicon), Baxter International Inc., Braun Melsungen AG, Medtronic plc, Pfizer Inc. |

Download Free Sample Report to Get Detailed Insights.

Hemostats Market Growth Factors Rising Surgical Procedures GloballyOne of the primary drivers of the global market is the surging number of surgical procedures worldwide. The increase in surgeries is driven by the surging prevalence of chronic conditions like cardiovascular diseases, cancer, and orthopedic disorders.

-

According to the World Health Organization (WHO), over 310 million major surgeries are performed each year globally. In addition, the rising geriatric population, more prone to requiring surgical interventions, further contributes to this trend. For instance, the American Heart Association reported that in 2023, over 1.2 million coronary artery bypass grafting procedures were performed in the U.S. alone.

These surgeries require effective bleeding control, boosting demand for hemostatic agents. Moreover, with the expansion of surgical care in developing regions, the need for efficient, fast-acting hemostatic products is growing steadily across diverse medical settings.

Market Restraining Factors High Cost of Advanced Hemostatic ProductsThe high cost of advanced hemostatic products poses a significant restraint to market growth, especially in low- and middle-income countries. Innovative solutions such as fibrin sealants, collagen-based agents, and flowable hemostats are priced higher due to their complex manufacturing processes and stringent regulatory approvals.

These elevated costs can burden healthcare facilities with limited budgets, making them rely on traditional and less effective methods. Additionally, the lack of reimbursement policies for advanced surgical adjuncts in several regions further discourages widespread adoption. This cost barrier particularly impacts smaller hospitals and clinics, hindering equitable access to optimal surgical care and limiting market penetration.

Market Opportunity Expansion in Emerging MarketsThe rising healthcare expenditure and infrastructural improvements in emerging economies provide substantial growth opportunities for the global market. As developing nations invest more in modernizing their surgical capabilities and hospital facilities, the demand for surgical consumables, including hemostatic agents, is expected to rise.

-

For instance, the UAE Cabinet allocated AED 5.745 billion (≈ 8% of the federal budget) to healthcare and community prevention for fiscal year 2025. Similarly, India's Union Budget 2023 allocated over ₹89,000 crore (approx. USD 11 billion) to healthcare, focusing on tertiary care expansion.

These investments are increasing the number of public and private surgeries and trauma centers, thereby creating demand for efficient bleeding control solutions. Global manufacturers are also increasingly localizing their operations and launching cost-effective hemostats to cater to price-sensitive, high-volume markets across Asia, the Middle East, and Latin America.

Regional InsightsThe market in North America is driven by advanced surgical infrastructure, high healthcare spending, and early adoption of innovative surgical products. A strong presence of leading medical device companies and robust clinical research facilitates continuous product innovation. The region also sees high procedural volumes in cardiovascular, orthopedic, and trauma surgeries, further boosting demand. Favorable reimbursement policies and a well-structured regulatory framework support market growth. Moreover, growing awareness among healthcare professionals regarding blood management during surgeries has led to the increased adoption of topical hemostatic agents across hospitals and surgical centers.

U.s Hemostats Market Trends-

The United States hemostats industry is driven by the high volume of surgical procedures, advanced healthcare infrastructure, and growing use of innovative hemostatic agents. For example, Baxter International's Floseal and Ethicon's Surgicel are widely used across major U.S. hospitals. Additionally, the country's aging population and rising prevalence of chronic diseases are fueling surgical interventions, further supporting the demand for reliable and fast-acting hemostats.

The Canadian hemostats marketis experiencing steady growth due to increasing investments in hospital upgrades and surgical care. The adoption of advanced hemostatic products like fibrin sealants and flowable hemostats is expanding, especially in cardiac and orthopedic surgeries. Initiatives by organizations like Health Canada to approve innovative products and improve surgical outcomes are promoting market expansion. For instance, hospitals in provinces like Ontario are adopting advanced bleeding control solutions for trauma and elective surgeries.

The global market in Asia Pacific is witnessing rapid growth due to expanding healthcare infrastructure and rising surgical procedures driven by an increasing patient base. Governments are investing in modernizing hospitals, which facilitates the adoption of advanced surgical tools, including hemostats. There is growing demand for affordable and easy-to-use products, especially in mid-sized healthcare settings. Additionally, rising medical tourism and improvements in surgical training and awareness are further supporting market penetration. Domestic manufacturers are entering the space with cost-effective alternatives, creating competitive dynamics and enhancing accessibility across both urban and rural areas.

-

China's hemostats market is expanding rapidly due to a surge in surgical procedures and increased government investment in healthcare infrastructure. For instance, China's "Healthy China 2030" initiative is boosting the demand for advanced surgical products, including hemostats. Local manufacturers like Yuwell and international players such as Johnson & Johnson are strengthening their footprint through partnerships and product launches, especially in tier-2 and tier-3 hospitals.

The Indian hemostats market is witnessing growth driven by rising healthcare awareness, increasing surgeries, and expanding private hospital networks. With over 60,000 surgeries performed daily in India, demand for effective bleeding control solutions is rising. Companies like B. Braun and Baxter are expanding their distribution and training programs in India, while Indian manufacturers like Hemarus are scaling up production of cost-effective hemostatic products to meet domestic and export demand.

Europe's market benefits from a mature healthcare system and increasing preference for minimally invasive surgical techniques. High demand for cost-effective, efficient surgical tools, along with widespread adoption of advanced hemostatic technologies in public and private hospitals, is contributing to market expansion. Emphasis on reducing surgical complications, such as excessive bleeding, fuels innovation in bio-compatible and absorbable agents. Regulatory support for clinical testing and CE approvals further accelerates the commercialization of new products. The growing elderly population also increases surgical volumes, particularly in orthopedic and general surgeries, driving market demand.

-

Germany's hemostats market is driven by its advanced healthcare infrastructure and high volume of surgical procedures. According to OECD, Germany performs over 2.4 million inpatient surgeries annually. Institutions like Charité – Universitätsmedizin Berlin and University Hospital Heidelberg increasingly adopt advanced hemostats like fibrin sealants for precision bleeding control. The presence of leading manufacturers such as B. Braun and significant investments in surgical innovations support steady market growth.

The UK hemostats market is witnessing growth due to increasing NHS surgical procedures and the adoption of minimally invasive techniques. According to NHS Digital, nearly 5 million surgical admissions occur annually, boosting demand for effective bleeding control. Leading hospitals such as Guy's and St Thomas' are integrating topical hemostatic agents into routine practice. Additionally, collaborations with global players like Baxter and Johnson & Johnson are enhancing product availability and innovation.

Oxidized regenerated cellulose (ORC)-based hemostats hold a dominant position due to their superior absorbability, antimicrobial properties, and ease of use during surgical procedures. This product effectively control bleeding and is particularly favored in minimally invasive and laparoscopic surgeries. Their compatibility with a wide range of procedures and minimal adverse reactions make them a preferred choice among surgeons. Moreover, their cost-effectiveness and regulatory approvals across various regions further contribute to their widespread adoption in the global market.

Formulation InsightsMatrix and gel hemostats dominate the formulation segment owing to their rapid hemostatic action and ease of application, especially in complex or irregular wound surfaces. These formulations are increasingly used in trauma and cardiovascular surgeries where immediate bleeding control is critical. Their enhanced biocompatibility and ability to conform to the surgical site provide a clinical advantage. Additionally, ongoing innovations and product launches featuring enhanced flowability and efficacy further strengthen the dominance of this segment.

Application InsightsOrthopedic surgery leads the application segment due to the high incidence of bone fractures, sports injuries, and age-related orthopedic disorders globally. These surgeries often involve significant blood loss, making effective hemostatic management crucial. Hemostats are widely used in joint replacements, spinal surgeries, and fracture fixations to minimize bleeding and improve visibility. The rising aging population and growing volume of orthopedic procedures across developed and emerging markets fuel the demand for hemostats in this surgical category.

End-User InsightsHospitals and clinics represent the largest end-user segment due to their comprehensive surgical infrastructure, higher patient inflow, and ability to adopt advanced hemostatic products. These facilities perform an extensive range of procedures requiring reliable bleeding control solutions. Their procurement capacity and adherence to strict surgical safety protocols ensure consistent use of approved and high-quality hemostats. Furthermore, the presence of skilled surgical staff and government investments in hospital infrastructure support the continued dominance of this segment.

Company Market ShareCompanies in the hemostats market are focusing on expanding their product portfolios through research and development of advanced hemostatic agents, including bioactive and flowable formulations. They are investing in clinical trials to demonstrate product efficacy and safety, while also enhancing global distribution networks. Additionally, strategic partnerships with hospitals, acquisitions of smaller firms, and regulatory approvals are key growth strategies being adopted to strengthen market presence and gain a competitive edge.

Baxter International Inc.: Baxter International Inc. is a leading global healthcare company renowned for its advanced surgical products, including a strong portfolio of hemostatic agents. The company offers widely used products such as Floseal and Tisseel, which are employed in various surgical procedures to control bleeding effectively. Baxter's strategic focus on innovation, R&D, and acquisitions has strengthened its position in the hemostats market. Its global distribution network and collaborations with hospitals and surgical centers further enhance its market reach and product adoption.

-

In April 2025, Baxter launched a new room-temperature version of its Hemopatch Sealing Hemostat in Europe. This ready-to-use collagen pad eliminates the need for refrigeration, enhancing surgical efficiency. Designed for rapid bleeding control and tissue sealing, it supports both open and minimally invasive procedures, offering improved convenience and performance in diverse clinical settings.

-

Johnson & Johnson (Ethicon)

Baxter International Inc.

Braun Melsungen AG

Medtronic plc

Pfizer Inc.

Integra LifeSciences Corporation

Teleflex Incorporated

CSL Behring

BD (Becton, Dickinson and Company)

Z-Medica LLC (a Stryker company)

Hemostasis LLC

Arch Therapeutics Inc.

-

June 2025- Johnson & Johnson MedTech launched the ETHICONTM 4000 Stapler, featuring proprietary 3D Staple Technology and enhanced Gripping Surface Technology (GST). This advanced stapler is designed to manage tissue complexities and deliver exceptional staple line integrity, minimizing risks of surgical leaks and bleeding complications across specialties. The ETHICON 4000 Stapler is approved for use in open and laparoscopic surgeries and is planned for future use exclusively on the OTTAVATM Robotic Surgical System.

April 2025- A joint team from IIT‐BHU and Banaras Hindu University secured a patent in India for an innovative hemostatic patch combining homogeneous polymer and Ayurvedic nanotechnology. Developed for managing conditions such as uterine bleeding, pregnancy‐related hemorrhage, and open wounds, this novel solution represents a significant advancement in biopolymer‐Ayurvedic integrated bleeding control.

January 2025- Cresilon Inc. launched TRAUMAGEL, a plant-based hemostatic gel in the U.S. Designed for rapid bleeding control, it is fully non-animal derived and ideal for trauma care. TRAUMAGEL offers fast, effective clotting at the point of care, aligning with the growing demand for bio-based, efficient surgical solutions in emergency and critical settings.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.95 Billion |

| Market Size in 2026 | USD 3.13 Billion |

| Market Size in 2034 | USD 4.98 Billion |

| CAGR | 5.99% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Type, By Formulation, By Application, By End-user |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Hemostats Market Segments By Type-

Thrombin Based Hemostats

Oxidized Regenerated Cellulose Based Hemostats

Combination Hemostats

Others

-

Matrix & Gel Hemostats

Sheet & Pad Hemostats

Sponge Hemostats

Powder Hemostats

Others

-

Orthopedic Surgery

General Surgery

Neurological Surgery

Cardiovascular Surgery

Reconstructive Surgery

Gynecological Surgery

Others

-

Hospitals & Clinics

Ambulatory Surgical Centers

Casualty Care Centers

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment