403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

ESG Omnibus: Three Proposals But A Common Path Towards Major Scope Reductions

(MENAFN- ING)

Source: ING, European Commission, Council of the EU, European Parliament Proposed scope's impact on the European banking sector

Source: ING

Source: ING, European Commission, Council of the EU, European Parliament

Source: ING, European Commission, Council of the EU, European Parliament What does that mean for banks?

Following the European Parliament's agreement on the sustainability Omnibus last week, interinstitutional talks (Trilogue negotiations) have now begun. As the Commission, Council of the EU, and Parliament work towards a final Omnibus I draft, we believe this is the right moment to step back and review what's on the table. Focusing on the European banking sector, we estimate the impact of each proposal.

Although final changes to the sustainability reporting directives are still under discussion, one thing is clear: the significant scope reductions proposed will negatively affect banks that remain subject to these reporting requirements.

Legislative updateEarlier this year, the Commission shared its proposal for a sustainability Omnibus (Omnibus I). The EU's executive arm leveraged the Union's legal mechanism for merging and streamlining multiple policies in order to simplify the European Sustainability Reporting Directives. This covers the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD) and the European Taxonomy.

However, by doing so, the proposal suggests significant changes that somewhat alter the essence of these policies. Read more in our first piece on the Commission's Omnibus I proposal here.

Like any Omnibus package, the sustainability Omnibus is subject to the Ordinary Legislative Procedure. Therefore, following the Commission's initial proposal, both the Council of the EU and the Parliament were required to come up with their own proposal based on the Commission's work. The Council suggests more significant changes to the Directives than initially proposed by the Commission. Read more on the Council's proposal here. The last missing piece of the puzzle was therefore the Parliament's proposal, which was agreed upon last week.

Now that all three institutions have published their final position, they need to come together to design one final proposal. This will then have to be approved by the Parliament before entering into force.

The Parliament's proposalBefore examining the potential impact of Omnibus I on the European banking sector, we considered it important to review the final piece of the puzzle ahead of the Trilogue negotiations: the Parliament's proposal.

After heated negotiations and an initial rejected vote in October, the European Parliament approved its final sustainability Omnibus position on 13 November. The piece includes multiple significant amendments to the Commission's initial proposal. The four key variations are the following.

1) Enforcement scope

The enforcement scope was an extremely contentious point during the Parliament's negotiations. After multiple delays and plot twists, the Parliament passed the following proposal:

-

CSRD: Applies to entities with more than 1,750 employees and a net turnover above €450 million. This represents the greatest proposed scope reduction, as the Council suggests an employee threshold of 1,000 headcounts.

European Taxonomy: Aligned with the CSRD threshold - entities with over 1,750 employees and €450 million turnover. Below this, companies may opt in to the disclosures. While broader than the Commission's proposal, it is less restrictive than the Council's.

CSDDD: Applies only to entities with more than 5,000 employees and €1.5 billion turnover, matching the Council's position and going beyond the Commission's proposal.

To ensure a level playing field, the Parliament proposes harmonising enforcement for third-country entities. Any subsidiary or branch in the EU generating more than €450 million in turnover would be subject to sustainability disclosures.

Despite the variations between each institution's position, both the Council and Parliament introduce more significant reductions than initially planned by the Commission. While the final thresholds will be decided in Trilogue negotiations, one thing is clear: European Sustainability Reporting Directives will apply to far fewer entities - an outcome that will significantly impact the banking sector.

2) ESRS simplification

In line with what was proposed in the Commission's document, the Parliament plans to simplify the European Sustainability Reporting Standards (ESRS) through the amendment of the Delegated Act. However, the Parliament lays out five specific conditions for the simplification, including prioritising quantitative indicators. The European Financial Reporting Advisory Group (EFRAG) was tasked with developing the update of the ESRS and has already submitted a draft proposal earlier this year.

Beyond simplifying the ESRS, the Parliament proposes making sector-specific standards voluntary through guidelines. This contrasts with the Commission and Council's approach, which seeks to eliminate these sector-specific standards entirely.

3) Climate transition plan

The third major element in the Parliament's position is the removal of the sustainability transition plan requirement under the CSDDD. The co-legislator argued that transition plans are already mandated by other EU legislation, justifying this more radical stance. This goes beyond the two existing proposals, which only sought to simplify or eliminate the planning obligation as well as introduce regulators' guidance.

4) Maximum fine caps

The Parliament proposes introducing a maximum fine cap for entities breaching CSDDD requirements, set at 5% of the undertaking's net worldwide turnover. This contrasts with the Commission's plan to remove the current minimum fine cap and the Council's preference for issuing guidelines to Member States.

However, the Parliament aligns with earlier positions by recommending the removal of the civil liability clause for entities violating the CSDDD. This means undertakings would not face civil liability at the EU level, though Member States could choose to apply it.

The table below summarises and highlights the main changes proposed by each institution that will take part in the negotiations as of this week.

Summary of each institution's Omnibus positionSource: ING, European Commission, Council of the EU, European Parliament Proposed scope's impact on the European banking sector

In our first publication on the sustainability Omnibus, we estimated the impact that the Commission's proposal could have on the European banking sector. We identified three channels through which these changes would affect the financial sector, namely:

-

Smaller banks falling out of scope

Lower data availability

Legislative uncertainty

While this holds true for each proposal, differences in scope mean the degree of impact varies. With Trilogue negotiations kicking off this week, we felt it was the right time to revisit and expand on our earlier analysis of Omnibus I's impact on the banking sector.

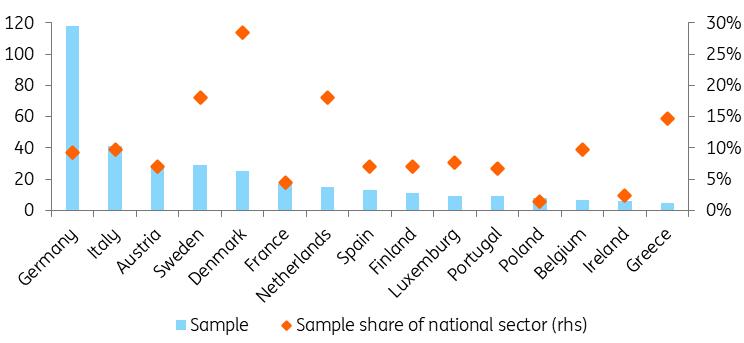

To do so, we increased our bank sample to include 342 banks from 15 Member States. The sample includes both globally significant institutions (under the direct supervision of the European Central Bank) and less significant banks (supervised by their national regulator).

German banks represent the largest portion of our sample, with nearly 120 institutions included. However, this accounts for just under 10% of all German credit institutions.

On average, our sample captures just above 10% of all financial institutions nationally. The graph below depicts the number of banks included per country as well as the share of the national sector it represents.

Number of banks included in our sample per countrySource: ING

For each financial institution in our sample, we collected data on the number of employees, balance sheet size, and net turnover. Based on the thresholds proposed by each institution prior to the Trilogue negotiations, we estimated the proportion of banks that would be exempt from sustainability disclosure requirements.

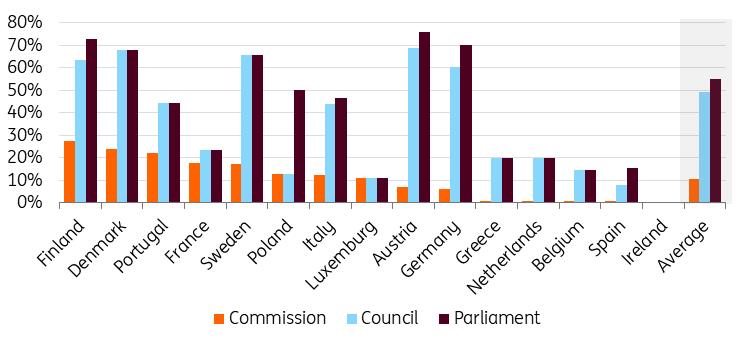

Major differences in CSRD impacts

Looking at the changes to the CSRD, we note a substantial difference in the proportion of financial institutions falling out of scope depending on whether the Commission's proposal or those from the Council and Parliament are applied.

Under the Commission's thresholds, the average share of banks excluded from the Directive is just over 10%, and no Member State exceeds 30% of its sector being exempt from sustainability disclosures.

In contrast, the average proportion of banks out of scope rises sharply to 49% under the Council's proposal and 55% under the Parliament's. This increase is driven primarily by the change in the net turnover threshold, which jumps from €50 million to €450 million.

The Parliament's proposal, which limits inclusion to entities with more than 1,750 employees and a net turnover above €450 million, results in up to 75% of the sector falling out of scope in Austria. This reflects the country's large number of smaller financial institutions. Other countries, such as Finland, Denmark, Sweden, and Germany, would also see the majority of their banks excluded, with figures exceeding 60%.

The graph below illustrates the impact of each institution's proposed CSRD scope on the share of banks excluded, by country. Beyond the overall effect on the banking sector, it highlights significant variations between Member States. Countries like Ireland, Luxembourg, and Belgium show relatively lower exclusion rates, reflecting financial sectors dominated by larger entities.

Share of banks falling out of the CSRD's scope per proposalSource: ING, European Commission, Council of the EU, European Parliament

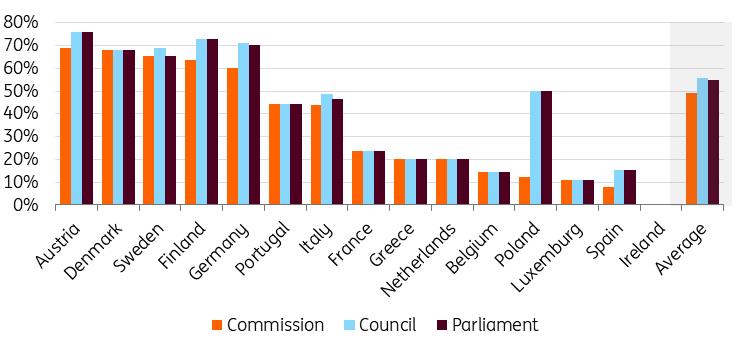

Significant but similar impact of Taxonomy's scope

Replicating the exercise using the different scopes proposed for the European Taxonomy reveals fewer differences between the three institutions' positions. Since the monetary threshold remains consistent across all proposals (net turnover above €450 million), only the employee criterion drives variations in the results.

Unsurprisingly, the Council's proposal would exclude the largest share of institutions, with nearly 60% on average falling out of scope. The Commission's proposal has a comparable impact, with around 50% of banks exempt from Taxonomy disclosures, while 55% are exempt when applying the Parliament's threshold.

Here again, the most pronounced effects appear in Austria and Denmark, where up to 76% and 68% of the banking sector, respectively, would fall outside the Taxonomy's scope. These figures reflect the relatively high proportion of smaller entities in these countries. The graph below illustrates the share of banks excluded under each Taxonomy proposal, by country.

Share of banks falling out of the European Taxonomy's scope per proposalSource: ING, European Commission, Council of the EU, European Parliament What does that mean for banks?

Naturally, for banks that fall out of scope of the sustainability reporting requirements, these changes will significantly reduce their disclosure burden. However, for those remaining in scope, the reduction in the number of corporates subject to sustainability reporting will negatively impact their own disclosures.

As highlighted in our previous publication, narrowing the scope implies that only the largest corporates will be required to collect and share sustainability data. Since banks rely heavily on client data for their own reporting, this change will directly reduce both the quality and quantity of available information, while increasing disclosure costs.

To address this, banks will have two solutions:

-

Firstly, they can develop bilateral agreements with their clients to gather and share the necessary data points. However, considering both the one-off cost of implementing the required systems and the longer-term maintenance costs, it is difficult to see the benefit for corporates outside the scope. Moreover, corporates falling under the value chain cap are under no obligation to provide such data to their credit institutions.

Secondly, financial institutions could make use of more proxies to compensate for the lack of data from their clients. While this solution would offer the benefit of limiting costs, the current state of the Directive limits the use of such proxies. For this to be a viable solution, regulators would need to relax these limits. Additionally, relying on proxies could raise questions about the reliability of the data, as it would not accurately reflect the true state of banks' portfolios.

The sustainability Omnibus also introduces legislative uncertainty. With Trilogue negotiations starting this week, the cost of disclosure uncertainty for European banks should not be underestimated. Many banks in our sample could either fall within or outside the CSRD's scope depending on the outcome of these interinstitutional discussions.

Considering the costs of designing and implementing both the CSRD and the European Taxonomy, decisions on data collection and disclosure are not to be taken lightly.

Three proposals but a common path towards major scope reductionsAs Trilogue negotiations begin this week, the final shape of the European sustainability Directives remains uncertain. However, the publication of both the Council's and Parliament's official positions ahead of the interinstitutional talks points to one clear trend: a further significant narrowing of the Directives' scope.

In the aftermath of the Commission's Omnibus I proposal, several stakeholders in the European legislative process, such as the Parliament's Left parties, strongly opposed the initial scope reduction. The European Central Bank also weighed in, expressing concerns about the repercussions it could have on the regulation of the European banking sector and the assessment of climate-related risks.

Despite these objections to weakening sustainability reporting requirements, both the Council and Parliament have gone beyond the Commission's initial proposal. While each approach may have different implications for the European banking sector and negotiations are still ongoing, one point is clear: only the very largest entities, both corporate and financial institutions, will remain subject to sustainability disclosure obligations.

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment