Bank Of Japan Hits Pause Dissenting Votes Hint At Incoming Rate Hikes

| 0.5% | Target rate |

| As expected |

As widely expected, the Bank of Japan maintained its policy rate at 0.5%. However, the surprise came from the fact that two board members dissented, favouring a 25bp hike, which indicates that more hawkish voices are growing within the board. The dissenting voters expressed the view that recent price trends indicated the BoJ's price stability target had been largely met and noted an increase in potential upside risks to prices.

In its statement, the BoJ noted that inflation expectations have risen moderately, and underlying CPI inflation is generally consistent with the price stability target. We agree with the BoJ's assessment. Recently, headline inflation eased – though mostly due to the energy subsidy program – while core inflation remained above 3%. Firm wage growth is expected to continue, and this is likely to keep inflation floating above 2%.

At the press conference, Governor Kazuo Ueda showed some confidence in the growth outlook. He continues to highlight high uncertainty, but sees little sign of tariffs having an impact on Japan's economy, and noted that the US-Japan trade deal reduced uncertainty quite meaningfully. Regarding inflation, the price trend is still below the goal, but is progressing towards 2%. Ueda also emphasised data-dependent decisions, and we believe he aims to maintain a balanced approach to future policy actions.

With reduced uncertainty and expected rate cuts from the Federal Reserve supporting US growth, the BoJ can proceed more confidently with policy normalisation. Core inflation has remained above 3% for an extended period. Even after a 25bp increase, the policy rate of 0.75% remains below the estimated neutral rate, which means that monetary conditions continue to be accommodative. We therefore expect the BoJ to deliver a 25bp hike in October.

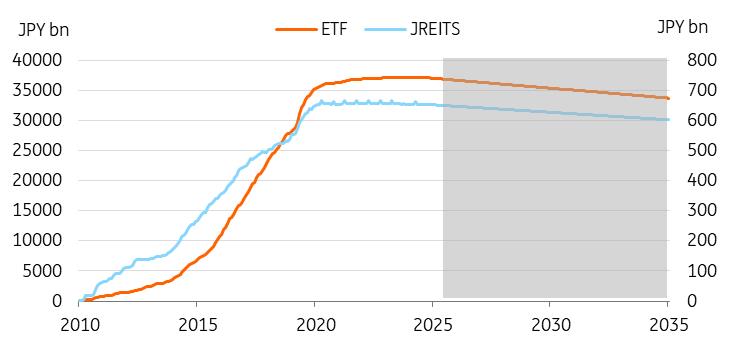

The BoJ will unload its holdings of ETFs and J-REITsToday, the BoJ announced its plan to reduce its holdings of ETFs and J-REITs. Although recent media reports had hinted at this development, the timing of the announcement was earlier than most market participants had anticipated. The unwinding process is expected to proceed at a measured and gradual pace. To reduce market impact, 0.05% of trading values will be sold in the markets. The annual sales amount, based on book value, will be 330bn yen for ETFs and 5bn yen for J-REITs. The BoJ also allowed sales amounts to be adjusted if key price indexes drop significantly.

ETF/J-REIT sells at a glacial pace

Source: CEIC Political uncertainty remains a key risk for postponing BoJ rate hike

While we continue to believe an October hike is possible, political factors may influence future policy decisions.

On 4 October, a Liberal Democratic Party (LDP) leadership election will take place; the outcome could affect the timing of monetary policy moves if a candidate with dovish views is selected.

Among the two leading candidates, Sanae Takaichi has publicly expressed her opposition to the BoJ rate hikes. Her policy stance closely aligns with that of former prime minister Shinzo Abe, indicating a preference for maintaining both monetary and fiscal policy easing measures. During her press conference held this afternoon, Takaichi pledged to raise the limit for untaxed income and eliminate gasoline taxes. She did not make any explicit comments regarding BoJ policy today. However, her fiscal spending plan suggests a preference for maintaining monetary policy in an easing position.

Rapid JPY appreciation is not desirable for the BoJAnother consideration for the BoJ is the Fed's policy. If the Fed cuts rates again in October, the yen could appreciate rapidly, which may influence the BoJ's decision-making process. Japanese exports have suffered from US tariffs, but the impact has been partially offset by a weaker JPY. As a result, the central bank may exercise caution when it comes to rate hikes, as they could lead to a sharp rise in the currency.

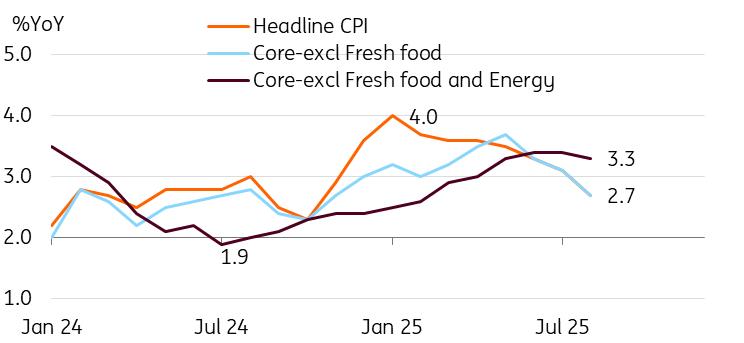

| 2.7% |

Consumer price inflation (%YoY)

Core inflation excluding fresh food and energy: 3.3% |

| Lower than expected |

CPI inflation eased to 2.7% year-on-year in August (compared to 3.1% in July and the market consensus of 2.8%), thanks to government subsidies. The energy subsidy programme reduced utility prices by 4%, while the free tuition programme lowered education prices by 5.6%. Meanwhile, food prices moderated, though they remained high at 7.2%.

Today's headline inflation growth was the slowest since November 2024, though it remains well above the Bank of Japan's target range of 2%. Core inflation excluding fresh food and energy – a better gauge of underlying inflation – rose to 3.3%, down slightly from 3.4% the previous month. It increased by 0.1% month-on-month seasonally adjusted, with goods and services prices rising by 0.1% and 0.2%, respectively. Despite the slowdown in headline inflation, we believe that sticky core inflation represents a steady rise driven by demand-side pressure.

Going forward, we expect inflation to pick up in the coming months, with noise created by the government subsidy programme.

Core inflation stays above 3%

Source: CEIC Yen thinks about rallying

USD/JPY briefly sold off around 0.5% on the news today that two of the nine BoJ voters favoured a 25bp rate hike. However, it subsequently recovered during Ueda's press conference as he provided few clues about the timing of the first hike.

As above, we think the risks of a 25bp BoJ rate hike on 30 October are underpriced at a 52% probability. That will be bullish for the yen if we're right with our BoJ call. If seen, that will further lower the hedging costs that Japanese investors pay to FX hedge their US asset portfolios. Back in late 2023, FX hedge ratios would have been low when it cost nearly 6% per annum (using the three-month forward) to hedge US exposure. Those hedging costs have dropped to 3.60% today and should move close to 3.00% later this year, largely driven by two further 25bp rate cuts from the Fed. A BoJ hike would be a bonus here.

We think USD/JPY is staying bid at the moment on a mixture of low volatility favouring the carry trade, political uncertainty around the new LDP leader and perhaps some corporate flows as well. But behind the scenes, the Japanese Balance of Payments (BoP) picture is actually quite yen-supportive. Fed cuts and a potential BoJ hike should be enough to see USD/JPY press 145 towards the end of October and drift down to 140 by year-end as the seasonal dollar weakness in November and December kicks in.

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

- Ozak AI Partners With Pyth Network To Deliver Real-Time Market Data Across 100+ Blockchains

- Blockchainfx Raises $7.24M In Presale As First Multi-Asset Super App Connecting Crypto, Stocks, And Forex Goes Live In Beta

- B2PRIME Secures DFSA Licence To Operate From The DIFC, Setting A New Institutional Benchmark For MENA & Gulf Region

- BTCC Summer Festival 2025 Unites Japan's Web3 Community

- From Zero To Crypto Hero In 25 Minutes: Changelly Introduces A Free Gamified Crash Course

- BILLY 'The Mascot Of BASE' Is Now Trading Live On BASE Chain

More Story

Comments

No comment