Tariffs Weigh On India's Growth Outlook Despite Tax Relief

(MENAFN- ING)

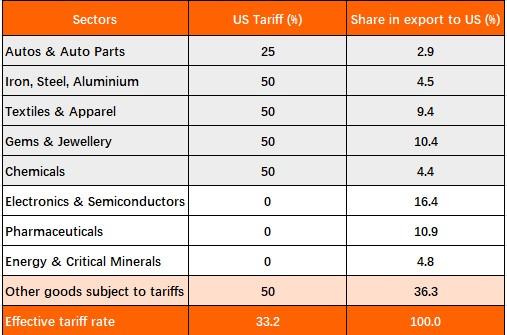

Tariff shock: a sudden escalation in US-India trade tensions

Source: ING research, White House GDP impact: manageable on paper, but larger indirect risks

Source: CEIC The Russian oil dilemma – strategic vs economic trade-offs

Source: Department of Commerce, India Some moderation in oil imports from Russia in recent months

Source: Bloomberg Why India Is holding back on US dairy imports

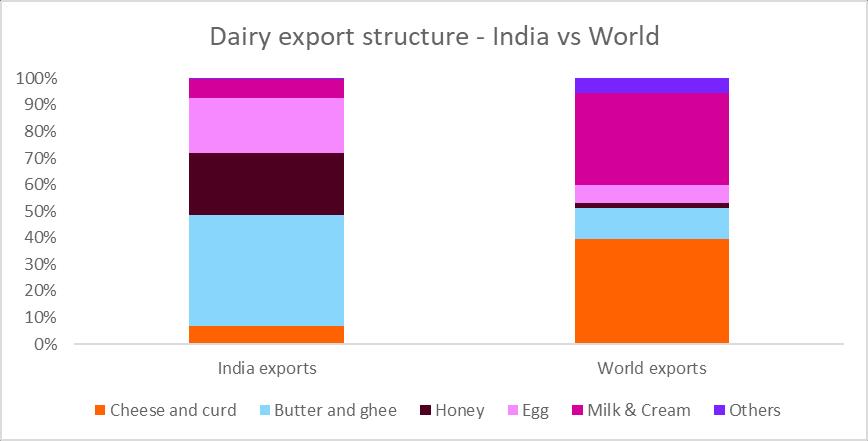

Source: International trade center India's dairy export structure is very different from the rest of the world

Source: International trade center GST reform, a huge win for the Modi government, could partially offset the tariff drag

Source: India government Impact on financial markets: tariff shock opens room for policy easing

Source: Bloomberg

President Trump's steep 50% tariffs on Indian imports officially took effect ten days ago – a move that includes a 25% penalty on India for its continued oil imports from Russia. The combined tariffs mark a sharp escalation in trade tensions between India and the US against market expectations of a for a swift deal between the two countries.

India cannot afford to overlook its trade relationship with the US, which accounts for 21% of its total exports. While electronics and pharmaceuticals – nearly one-third of this trade – remain largely unaffected, other sectors face substantial headwinds. Auto parts (3% of total exports) will be taxed at 25%, while the remaining 65%, including iron, steel, and aluminum, will be hit with the full 50% tariff.

Effective tariff rate at 33%Source: ING research, White House GDP impact: manageable on paper, but larger indirect risks

At a broad level, the macro impact looks relatively manageable. India exported about US$87 billion worth of goods to the US in FY2025 – less than 2% of its GDP. Once you factor in tariff-free categories like pharma and electronics, and adjust for domestic value added, the actual GDP exposure to these tariffs drops to around 1.2–1.3%. IMF estimates suggest that over the long run, a 1% increase in India's international export prices could lead to a drop in export volume growth – around 0.9% across all industries, and about 1.1% for manufacturing. Assuming a full tariff pass-through and no trade diversion, the direct hit to output would be 0.6-0.7% of GDP.

However, the impact would be much larger given the second-round impact on employment and consumption. Labour-intensive sectors like textiles, leather, and jewellery face the highest downside risk – not just in terms of exports, but also employment. These industries operate on thin margins and are highly price-sensitive, making them especially vulnerable to tariff shocks. Plus, since they rely more on low-skilled labour, they're easily substitutable by countries like Vietnam and Bangladesh, which offer similar products at competitive prices.

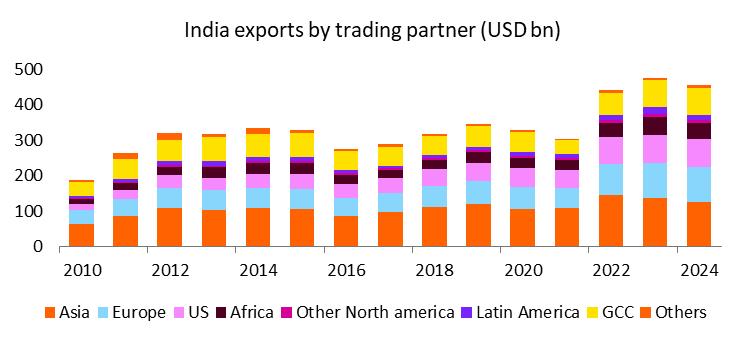

Can Asia fill the export gap? India's shrinking regional trade tells a different storyWe doubt Asia can fill the export gap. What's most striking about India's trade direction is that trade with the rest of Asia is shrinking -- and steadily so. If you look at India's export trends over the last five years, a clear shift is afoot. Back in 2018, more than one-third of exports were going to Asia. Fast forward to 2024, and that number has dropped to 28%. The decline really started during the Covid period and hasn't bounced back since.

Interestingly, what Asia lost, the US and Europe seem to have gained. Their share of India's exports has together gone up by around 7 percentage points over the same time. So, while Asia's role is shrinking, the West is stepping in to fill the gap.

This is the opposite to what we are seeing for the rest of Asia which is seeing a surge in intra-Asia trade. Part of the reason is that the India-ASEAN FTA on goods that was signed in 2010 never took off. From the perspective of Indian exporters, the India FTAs involved high user costs, largely due to complex rules of origin and burdensome documentation. These challenges, common to many of India's older FTAs, have led exporters to avoid utilising the agreement, given the high opportunity costs of claiming preferential access.

India has been actively negotiating trade deals with Europe and other countries to diversify its exports, but it's unlikely to be a quick remedy.

Exports to Asia have been fallingSource: CEIC The Russian oil dilemma – strategic vs economic trade-offs

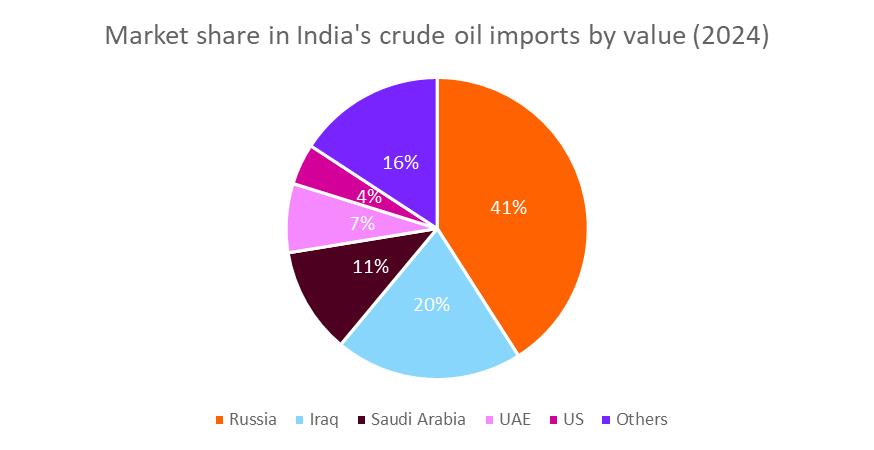

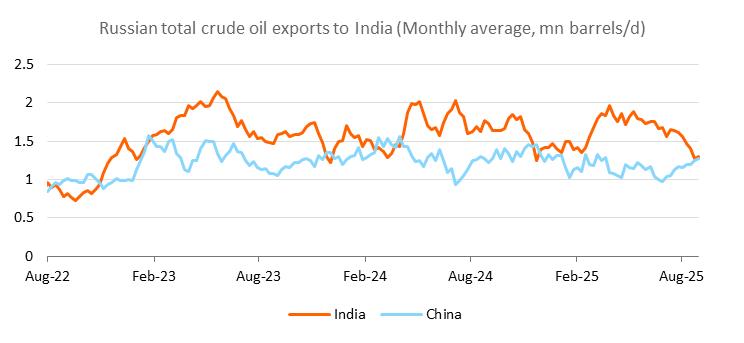

Russia remains the largest source of oil imports for India. While there has been some moderation in oil imports from Russia in recent months, it's too early to read it as a trend. On the face of it, cost savings from buying from Russia look small at about US$2/bbl. Hence, there is a strong view in the market that India should align with Trump's demands on Russian oil. However, our estimates suggest that if India were to stop buying oil from Russia, essentially removing Russian supply of crude, the surge in global Brent oil prices will be large. Our commodity strategy team estimates that the Brent oil price could increase from our base case of US$57/bbl to US$71/bbl in 2026 if India were to stop buying from Russia, which would cost India a large 0.7% of GDP. In addition, this 25% oil price increase would have a significant impact on India's inflation by potentially adding 0.7 percentage points to headline CPI.

While eventually successful trade negotiations could mean weaning India off Russian oil imports, it's not an easy economic choice. As such, India is treading carefully, exploring other options to reduce the 50% tariff blow.

Russia is the biggest supplier of oil imports for IndiaSource: Department of Commerce, India Some moderation in oil imports from Russia in recent months

Source: Bloomberg Why India Is holding back on US dairy imports

Another major point of contention in US-India trade negotiations is agricultural market access. While India has shown a willingness to ease restrictions on imports of US dry fruits and apples, it continues to hold back on allowing corn, soybeans, wheat, and – most notably – dairy products.

India is the world's largest milk producer, with an annual output of around 240 million tonnes. Yet, it contributes less than 0.7% to global dairy exports. This paradox highlights a critical gap: while India has scale, it lacks global competitiveness in high-demand dairy categories like cheese and curd. Instead, its export profile is skewed toward butter and milk fats, which face relatively lower global demand.

Opening up to US dairy imports could risk undermining India's vast domestic dairy ecosystem – largely composed of small-scale farmers and cooperatives – without a clear upside in export gains. Therefore, India's cautious stance is not just defensive; it's strategic.

India is a very small player in world dairy exportsSource: International trade center India's dairy export structure is very different from the rest of the world

Source: International trade center GST reform, a huge win for the Modi government, could partially offset the tariff drag

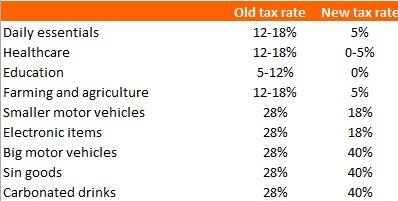

One of the recent measures that could partially offset the tariff impact has been cuts in GST (Goods and Services Tax) rates for some commodity groups.

In a bold move to stimulate domestic demand and make taxation more equitable, the Modi government overhauled the GST rate structure. Taxes on essential items – including food products, basic household goods, consumer electronics, and small motor vehicles – have been significantly reduced, while life-saving drugs and health and life insurance have been made entirely tax-free. These reforms are designed to directly boost consumption, especially among middle- and lower-income households.

To ensure fiscal prudence, the government is simultaneously introducing a new 40% GST rate for luxury goods, replacing the previous 28% rate. This rebalancing of the tax structure is expected to have only a marginal impact on the fiscal deficit – an increase of just 0.16% of GDP. The estimated revenue loss of c.0.3% of GDP from lower rates on basic goods and services is likely to be partially offset by gains of c.0.13% of GDP from the higher luxury tax.

Importantly, with revenue expenditure having a fiscal multiplier of 1, these changes are projected to lift consumption by 0.1-0.2% of GDP – providing a timely boost to economic growth.

GST rate cuts should partly offset negative impact from tariffsSource: India government Impact on financial markets: tariff shock opens room for policy easing

The downside risks to growth from steep US tariffs create more room for the Reserve Bank of India (RBI) to ease monetary policy. The export losses from high US tariffs are likely to be deflationary, and recent GST rate cuts could reinforce this disinflationary trend. We estimate that a full pass-through of GST rate cuts to the consumer could lower CPI inflation by 1 percentage point. Even under a more conservative scenario, we could see inflation declining by around 50 basis points over the next six months, bringing our current forecast of 3.4% to below 3%. This strengthens our case for another 50bp Repo rate cut by the RBI over the next six months with rising risks of the RBI front-loading cuts in the fourth quarter.

Encouragingly, the revenue impact from GST cuts appears smaller than expected, suggesting that government borrowing may remain contained this fiscal year – a positive signal for bond markets. Against this backdrop, we expect a relief rally in government securities, supported by stable fiscal dynamics and anticipated Fed rate cuts starting in September. The 10-year benchmark yield is likely to trade in the 6.45–6.50% range in the near term.

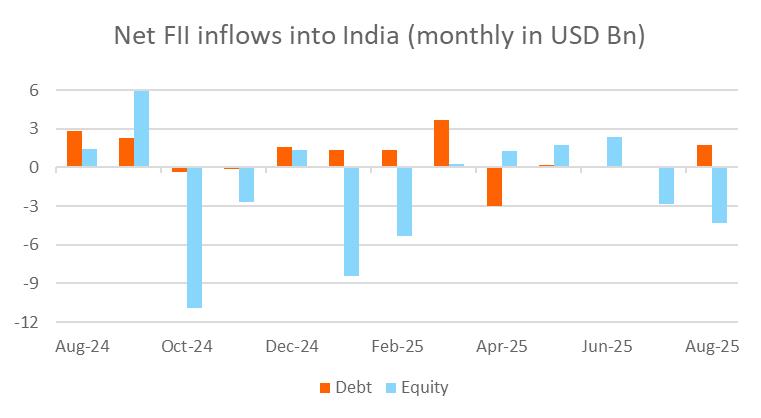

Ongoing tariff uncertainty continues to weigh on the Indian rupee, which has already depreciated by over 3% in the third quarter. Foreign investor sentiment remains cautious – FII equity inflows were weak this past week, following sharp outflows of US$4.3 billion in August. In contrast, debt inflows stayed resilient, with US$1.7 billion in net purchases last month, supported by easing concerns over fiscal slippage.

Looking ahead, active RBI intervention is expected to cap USD/INR around 89.0 in the near term, helping to stabilise currency markets amid external headwinds. However, the risk of further weakness persists if India fails to negotiate tariff levels lower. A prolonged export slowdown could structurally weaken India's current account balance, adding sustained pressure on the currency.

Ongoing tariff uncertainty continues to weigh on the Indian RupeeSource: Bloomberg

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Market Research

- Gas Engine Market Analysis: Strong Growth Projected At 3.9% CAGR Through 2033

- Daytrading Publishes New Study On The Dangers Of AI Tools Used By Traders

- Excellion Finance Launches MAX Yield: A Multi-Chain, Actively Managed Defi Strategy

- United States Lubricants Market Growth Opportunities & Share Dynamics 20252033

- ROVR Releases Open Dataset To Power The Future Of Spatial AI, Robotics, And Autonomous Systems

- Blackrock Becomes The Second-Largest Shareholder Of Freedom Holding Corp.

Comments

No comment