403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

The Worst Is Over For Europe's Building Materials Industry

(MENAFN- ING)

Further recovery expected in the building material industry

![- Source: Eurostat, ING Research]() Source: Eurostat, ING Research

Source: Eurostat, ING Research

![- Source: European commission, ING Research]() Source: European commission, ING Research

Prices of concrete, cement and bricks stable

Source: European commission, ING Research

Prices of concrete, cement and bricks stable

Source: Eurostat, ING Research

We anticipate a further revival of the building material industry in 2025, encompassing concrete, cement, and bricks. The sector faced significant challenges in 2022 and 2023 due to a decline in demand for new houses, the primary market for building material companies producing these products.

However, house prices of existing homes have started to increase in many European countries. This is a positive indicator for new developments, as the prices of newly built and existing homes typically follow each other closely; they cannot diverge too much since new and existing houses are substitutes for consumers. Therefore, new building developments will lead to increased demand for building materials.

In most European countries, building material suppliers' production levels plummeted in 2022 and 2023. Volumes were down by almost 15% in Spain and by around 25% in Belgium and Germany at the beginning of last year. Yet, we also observed the first signs of a recovery in 2024. Poland and the Netherlands are experiencing the largest comebacks. These countries have seen the biggest uptick, at 16% and 12%, respectively. In Germany, production is still at a very low level but has started to increase slowly as well.

It is only in France and Austria where volumes have decreased further. In a European Commission business survey, building material companies in these two countries are the most pessimistic about the development of further production in February 2025.

We believe that volumes in the building material sector will slowly further improve in 2025. In many urban European areas, there is a structural high demand for new houses. As mentioned earlier, house prices are improving and this makes the business case for new house developments and consequently the demand for building materials stronger. Nevertheless, higher interest rates could slow down the pace of this process.

Sharp recovery in building material production in Poland and the NetherlandsVolume production building material industry (eg. concrete, cement & bricks), Index January 2022=100 SA

The confidence indicator for the building materials sector has reached its lowest point

There are other signs indicating that the worst is over for building material producers. For instance, the confidence indicator for the EU construction sector is still negative but has improved slightly.

The confidence indicator for the building materials sector has reached its lowest point in the last three years, and although it has improved a bit, it remains negative.

Producer confidence in the building material sector is improving but still negativeEU producer confidence indicator, SA

Building material prices, such as concrete, are very stable and have almost not moved during the last two years. You might expect a price decline here as demand has significantly slowed, but the prices of concrete, cement and brick remain sticky.

Building materials such as concrete and cement are heavy and voluminous. This is why they're often traded on relatively small local markets, resulting in less competition. This gives the suppliers of these products a bit of market power, which usually results in both higher prices and lower price volatility. They do not have to pass on price reductions of raw materials or energy costs directly because of the relatively limited competition. As a result, the output prices of these products rise – and fall – at a slower rate compared to building materials such as steel, which are traded in more competitive markets.

The graph above also shows that the steel price follows a bumpier road. US tariffs on metals could also result in trade diversion from other origins, which could directly affect local EU metal prices.

Timber more expensive, plastics cheaper

The prices of many building materials are relatively steady. The cost of timber has slowly increased and prices were 7% higher in January 2025 compared to the same month a year earlier, following a decline of 4% in 2023. Plastic prices have remained more or less the same compared to two years ago.

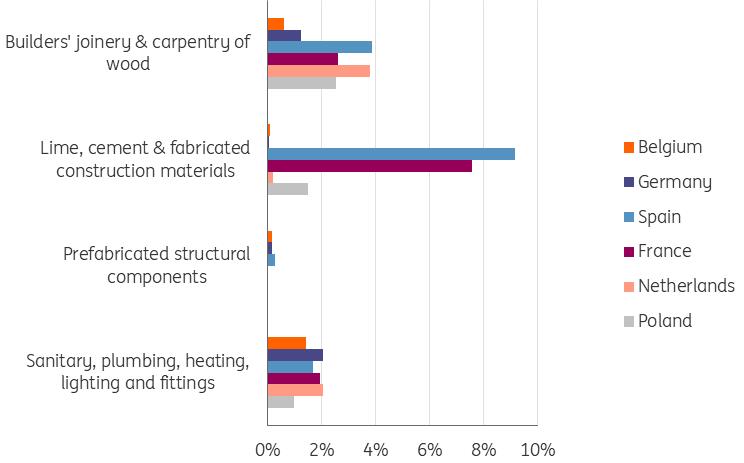

Many building materials, such as concrete, bricks, and cement, are heavy and thus costly to transport, resulting in limited exports from the EU to the US. For most building material categories from EU countries, less than 3-4% is exported to the US. Only France and Spain have a higher share of their exports to the US for lime, cement, and fabricated construction materials. However, the exported volumes remain low. For example, French building material suppliers exported only €55m worth to the US in 2024.

EU building material companies export little to USShare of total product category exports to US, 2024

Source: Eurostat, ING Research

The US imports the most Gypsum from Spain (US$85m), even more than from Mexico and Canada. Yet, relatively speaking, this is still a small amount compared to the total EU building material output that has a value of more than €260bn for the concrete, cement and brick subsegment alone per year. Therefore, US import tariffs will hardly affect the EU building material industry of these products. However, of course, for some specific individual companies it could be a real burden, and prices of other building materials such as metals could be affected due to changes in trade patterns.

Price increases only expected for timberBalance of manufactures in European Union which expects to increase/decrease output prices (over the next three months)

Source: Eurostat, ING Research Few producers expect price changesIt looks like there are no strong price movements of building materials expected. Only a very small number of the EU concrete, cement and brick suppliers said in February that they were expecting to increase their sales prices over the next three months. They probably don't see much room for this as demand is still relatively low from the construction industry, although it is slowly improving. In addition, input prices of raw materials such as sand have remained stable over the last year.

Author:Maurice van Sante

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment