403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Australia: Labour Data Remains Strong In July

| 58,200 |

Total employment gain in July

Follows 52,300 gain in June |

| Better than expected |

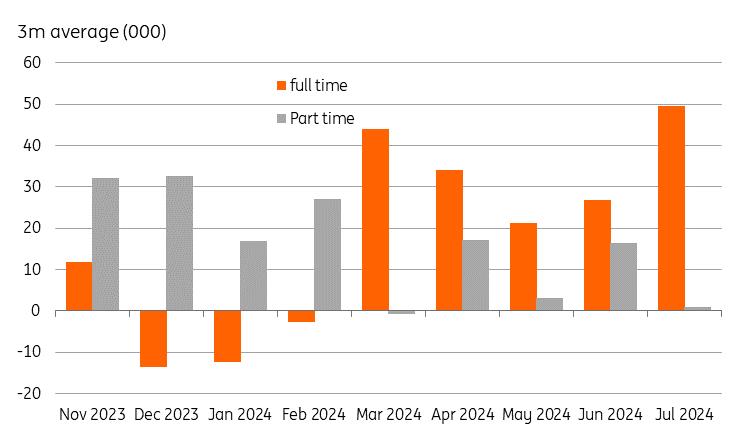

58,200 jobs were created in Australia in July, all of which were full-time (60,500), and there was a small decline in part-time employment (-2,300). Australian labour data is choppy, but this is the second month in a row in which total employment has risen by more than 50,000, and the June figure was also dominated by full-time employment.

There may be some concern that the unemployment rate has risen from 4.1% to 4.2%. However, the blame for this can be levelled firmly at the door of the rise in the labour force, where another strong monthly increase will have left some new entrants still without work, contributing to a roughly 24,000 increase in the unemployment total. We expect most of these new jobless will be swallowed up in next month's employment gains, with some initially getting part-time work before converting to full-time jobs.

In other words, this might be considered a "good" increase in the unemployment rate, which is both likely to be relatively short-lived, and reflects optimism about labour opportunities, not job shedding.

Part time vs full time jobs monthly change (000s, 3-month moving average)

Source: CEIC, ING Yes, but what about the RBA?

The RBA held rates unchanged at 4.35% in July, but this was a hawkish hold, and today's labour data suggest that the decision not to hike may have been a close one, and will remain a talking point in the months ahead. Recent wage price data held at 4.1% YoY instead of beginning to fall as had been expected. This stickiness in wages adds a further element of uncertainty about the inflation outlook, at a time when progress on inflation has been extremely slow.

The market's views on the outlook for the RBA's cash rate target have whipped around a lot this year. They are currently fully pricing in a rate cut by the end of this year. We would have to say that this looks like an extremely ambitious forecast to us, and we would be more comfortable with pricing that showed flat rates for the rest of this year, with even a small possibility of a final 25bp hike somewhere, to indicate lingering demand strength and price pressures. Until it does so, the AUD is likely to be whipped around by G-10 moves against the USD and by macro developments in China. This suggests a tendency to appreciate over the back end of the year, though with substantial volatility as the China story remains disappointing as evidenced by today's activity data dump.

Author:Robert Carnell

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment