403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Anti-Biofilm Wound Dressing Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

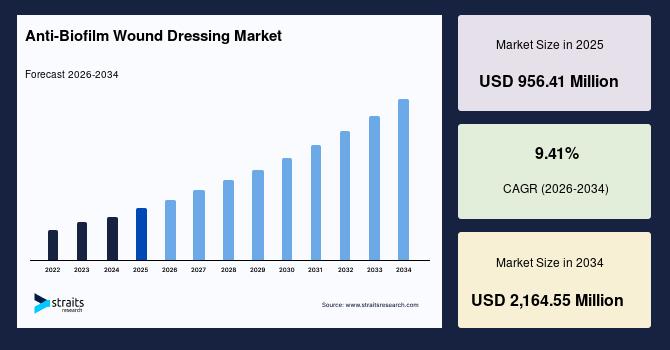

| 2025 Market Valuation | USD 956.41 Million |

| Estimated 2026 Value | USD 1,054.52 Million |

| Projected 2034 Value | USD 2,164.55 Million |

| CAGR (2026-2034) | 9.41% |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Smith & Nephew plc, 3M, Mölnlycke Health Care AB, ConvaTec Group PLC, Coloplast A/S |

Download Free Sample Report to Get Detailed Insights.

Emerging Trends in Anti-biofilm Wound Dressing Market Incorporation of Bacteriophage-embedded Anti-biofilm DressingsThe use of bacteriophage-embedded dressings, where viruses selectively kill bacteria within biofilms, is a key trend supporting the anti-biofilm wound dressing market growth. These dressings target resistant pathogens like Pseudomonas aeruginosa and Staphylococcus aureus, improving treatment effectiveness. Companies develop customizable phage libraries based on patient infection profiles, supporting precision medicine. For example, PhagoMed Biopharma develops phage-based therapies for chronic wounds. Clinical studies show improved biofilm disruption and healing rates. This gains adoption in diabetic foot ulcers, where conventional antimicrobial dressings fail against persistent biofilm infections.

Development of Smart Anti-biofilm Dressings with Real-time Sensing and ResponseSmart anti-biofilm dressings with real-time sensing and response are an emerging trend in wound care. These dressings use biosensors to detect pH changes, oxygen levels, and bacterial metabolites linked to biofilm formation. They release antimicrobial agents like silver nanoparticles or enzymes when infection is detected, improving treatment precision. For example, in clinical studies, dressings embedded with pH-sensitive hydrogels successfully signaled early biofilm growth and released anti-biofilm compounds automatically, accelerating healing. This approach supports remote monitoring and is especially useful for chronic wounds in elderly or home-care patients.

Market Drivers Increased Emphasis on Antibiotic Stewardship and Rising Demand for Chronic Wound Management in Aging Population Drives Anti-biofilm Wound Dressing MarketThe global push to reduce antibiotic overuse and combat antimicrobial resistance is driving market expansion. Anti-biofilm wound dressings that deliver targeted, non-antibiotic antimicrobial agents, such as silver nanoparticles, enzymes, or phage-based components, align with stewardship initiatives. Hospitals and clinics adopt these dressings to minimize systemic antibiotic exposure while effectively controlling biofilm infections. Regulatory support and clinical guidelines increasingly encourage alternatives to conventional antibiotics, boosting the adoption of innovative anti-biofilm products. This trend strengthens market growth, particularly in chronic and hard-to-heal wound segments.

The rising need for chronic wound care due to aging populations is a key driver for the anti-biofilm wound dressing market. Older adults have higher rates of diabetes, venous insufficiency, and immobility, all of which increase chronic wound prevalence and persistent biofilm infections. For example, by 2025, over 1 in 6 people worldwide will be aged 65 or older, a demographic strongly correlated with higher rates of pressure ulcers and diabetic foot ulcers that resist healing due to biofilms. This growing patient segment drives demand for advanced dressings that prevent biofilm formation, improve healing outcomes, and reduce costly hospital stays, especially in long-term care and home-health environments.

Market Restraints High Production Costs and Lack of Standardized Evaluation Protocols Restrain Anti-biofilm Wound Dressing Market GrowthThe high cost of producing multifunctional anti-biofilm dressings that combine sensors, nanoparticles, or enzymatic agents restrains their adoption in the market. Manufacturing these advanced materials involves specialized polymers, microfabrication, and sterilization processes, making them expensive compared to conventional dressings. For example, smart dressings with integrated pH and moisture sensors can cost 2 times more than standard antimicrobial dressings in premium markets. Small and mid-sized healthcare providers may struggle with adoption due to budget constraints, especially in homecare or developing regions, limiting widespread use despite clear clinical benefits.

A key restraint in the anti-biofilm wound dressing market is the lack of standardized evaluation protocols for innovative dressings like phage-embedded or smart responsive materials. Regulatory agencies require extensive safety and efficacy data, but biofilm-targeted technologies often face complex approval pathways due to their novel mechanisms. This slows product launch and clinical adoption. Hospitals and care centers hesitate to invest in unvalidated or variably tested products, particularly for chronic wounds, limiting market growth despite the high clinical need for advanced anti-biofilm solutions.

Market Opportunities Expanding Applications into Surgical Site Infection and Development of Multi-Functional Solutions Offer Growth Opportunities for Anti-Biofilm Wound Dressing Market PlayersThe development of anti‐biofilm wound dressings designed to prevent surgical site infections offer opportunities for market players. SSIs frequently involve biofilm‐forming bacteria that evade standard prophylactic treatments, leading to complications and longer recoveries. Advanced anti‐biofilm dressings applied immediately post‐surgery can reduce infection rates, shorten hospital stays, and cut readmission costs. For example, dressings incorporating antimicrobial polymers have shown reduced SSI rates in orthopedic joint replacement studies. By targeting surgical care pathways, companies can secure high‐value supply agreements and stand out in a competitive wound care market.

Use of anti-biofilm wound dressings specifically for patients with surgical implants, such as orthopedic rods, joint replacements, or pacemakers. Biofilm formation on implant-adjacent tissues often leads to severe infections that are costly and difficult to treat. Dressings that release targeted antimicrobials or biofilm-disrupting enzymes in the immediate post-operative period can prevent implant-related infections. Market players can partner with hospitals and surgical device manufacturers to supply high-value, specialized dressings, creating a differentiated product line and recurring demand in implant-heavy surgical segments.

Regional Insights North America: Market Leadership Driven by Favorable Reimbursement Structure and Telehealth ProgramsThe North America anti-biofilm wound dressing market accounted for a revenue share of 38.51% in 2025. The region benefits from a high prevalence of diabetes-related chronic wounds, especially in the US, where more than 6 million people live with chronic wounds, such as foot ulcers prone to biofilm infections. Hospitals and outpatient clinics increasingly use advanced dressings to prevent infections and improve healing. The growing home health and telemedicine infrastructure supports the adoption of smart anti-biofilm dressings, allowing remote monitoring of pressure injuries and non-healing ulcers, reducing clinic visits and improving patient outcomes.

The US anti-biofilm wound dressing market is leading the North America region because Medicare and Medicaid increasingly reimburse advanced dressings for chronic wounds, encouraging adoption in home health and long‐term care. For example, Medicare now covers specialized dressings for diabetic ulcers, lowering costs for elderly patients. The higher regional rates of obesity and diabetes in states like Texas and Florida lead to more chronic wound cases that require biofilm‐targeting products, boosting demand among wound care clinics and home health agencies.

Canada's anti‐biofilm wound dressing market is driven by very high chronic wound prevalence in acute and long‐term care settings. In Canadian hospitals, about 40 % of inpatients have at least one wound, with pressure ulcers and surgical wounds comprising most cases and infection rates up to 8%, indicating a strong clinical need for biofilm‐targeted dressings. Indigenous and remote communities face limited access to specialized care, creating demand for durable, easy-to-apply biofilm-targeting dressings. For example, healthcare programs in Nunavut implement advanced antimicrobial dressings in community clinics to manage chronic wounds in isolated populations, reducing the need for frequent hospital transfers and improving local patient outcomes through telehealth services.

Asia Pacific: Fastest Growth Driven by Rising Medical Tourism and Post-surgical Cases in Urban AreasThe Asia Pacific anti-biofilm wound dressing market is expected to register the fastest growth with a CAGR of 11.80% during the forecast period due to rising medical tourism and specialized surgical care in countries like Thailand and Singapore, where patients demand advanced post-operative wound management to prevent biofilm infections after cosmetic or orthopedic surgeries. The high prevalence of coastal flooding and tropical injuries in Southeast Asia increases chronic wound risk, creating demand for durable, moisture-resistant anti-biofilm dressings. For example, hospitals in Bangkok increasingly use such dressings for burn and trauma wounds in flood-affected patients.

The China anti-biofilm wound dressing market grows due to unique healthcare infrastructure priorities and local clinical practices. Wound care training programs by provincial health authorities emphasize biofilm awareness and modern dressing techniques in community hospitals, improving early adoption of advanced products at the grassroots level. For example, training initiatives in Sichuan and Guangdong routinely demonstrate biofilm‐targeting dressings for chronic wounds in outpatient settings, expanding clinician demand. Higher chronic wound burden in southern China leads to more persistent leg and foot ulcers that resist healing, prompting clinicians to use advanced anti‐biofilm solutions. These factors collectively drive market growth in China.

The India anti-biofilm wound dressing market grows due to rising post-surgical and trauma cases in urban hospitals and regional tropical wound risks. In cities like Mumbai and Delhi, high rates of road accidents and orthopedic surgeries create demand for biofilm-targeting dressings to prevent infections in complex wounds. Rising medical tourism in India means more foreign patients travel for procedures such as orthopedic, cardiac, cosmetic, and other surgeries, which increases the number of post-operative wounds requiring advanced care, including anti-biofilm dressings to prevent infection and promote healing. For example, the Ministry of Tourism reported that in 2025 (January–April) India recorded 131,856 Foreign Tourist Arrivals (FTAs) for medical purposes, accounting for about 4.1% of total foreign arrivals, up from 182,945 in 2020 and 644,387 in 2024, showing a substantial and growing international patient base whose surgical care needs contribute to demand for specialised wound care products. In India, community clinics use durable, easy-to-apply dressings to manage diabetic ulcers and pressure wounds, reducing hospital visits and improving infection control in resource-limited areas.

By Mode of MechanismThe chemical segment dominated the anti-biofilm wound dressing market in 2025, with a revenue share of 40.20% in 2025, due to the widespread use of silver, iodine, and honey-based antimicrobial agents in anti-biofilm dressings. For example, silver-impregnated dressings in US hospitals prevent biofilm formation on chronic and surgical wounds. Their proven efficacy, low cost, and easy integration into standard care drive segment growth.

The biological segment is expected to grow at a CAGR of 9.86% during the forecast period due to enzyme- and peptide-loaded dressings effectively degrading biofilms in chronic wounds, improving healing. Bacteriophage integration allows targeted elimination of resistant pathogens without harming healthy tissue. For example, lactoferrin- and dispersin B-based dressings in Japanese wound care centers show faster healing in pressure ulcers, driving adoption and segment growth.

By ApplicationThe chronic wounds segment is expected to grow at a CAGR of 10.17% during the forecast period due to the high prevalence of diabetic foot ulcers, pressure ulcers, and venous leg ulcers, which are prone to persistent biofilm infections. Delayed healing and frequent complications increase demand for advanced anti-biofilm dressings. Rising elderly populations and longer hospital stays drive the need for effective chronic wound management solutions, supporting segment growth.

The acute wounds segment in the anti-biofilm wound dressing market is expected to grow at a CAGR of 10.58% during the forecast period due to increasing surgical procedures, trauma cases, and post-operative care needs. Acute wounds like lacerations, burns, and surgical incisions are highly susceptible to rapid biofilm formation, requiring fast-acting anti-biofilm dressings. Shorter healing timelines and higher patient turnover in hospitals drive demand for advanced dressings that prevent infections and accelerate recovery, supporting segment growth.

By End UserThe hospitals segment dominated the market, accounting for 44.74% revenue share in 2025. This growth is driven by high patient volume, complex wound cases, and post-surgical infection risk. Hospitals manage chronic wounds, pressure ulcers, and surgical incisions that are prone to biofilm formation, requiring advanced anti-biofilm dressings. Hospital protocols favor standardized products to reduce readmissions and complications, driving bulk adoption and supporting segment growth.

The home healthcare segment is projected to grow at a CAGR of 10.57% during the forecast period, driven by rising chronic wound care at home, aging populations, and patient preference for convenience. Patients with diabetic ulcers, pressure sores, or post-surgical wounds increasingly receive treatment at home. Telemedicine and remote monitoring programs support the use of advanced anti-biofilm dressings, enabling clinicians to track healing, reduce hospital visits, and improve patient outcomes, driving segment growth.

Competitive LandscapeThe anti‐biofilm wound dressing market is moderately fragmented, with a mix of large global medical device companies and smaller specialized players. Leading firms like 3M Company, Smith & Nephew, ConvaTec, Mölnlycke Health Care, and Coloplast maintain strong positions through extensive product portfolios, proven clinical performance, and wide distribution networks. Smaller players, including Next Science, Imbed Biosciences, and Integra LifeSciences, focus on innovative biofilm-disrupting technologies, faster product development, and targeted solutions for specialized wounds. Established companies compete mainly on product range, clinical validation, regulatory approvals, and market reach, while emerging players differentiate through unique technologies, rapid innovation, and adaptability to new care settings.

List of Key and Emerging Players in Anti-Biofilm Wound Dressing Market Smith & Nephew plc 3M Mölnlycke Health Care AB ConvaTec Group PLC Coloplast A/S Braun Melsungen AG Medline Industries, LP Integra LifeSciences Holdings Corporation Medtronic plc Urgo Medical Next Science Limited Imbed Biosciences Inc. Covalon Technologies Ltd. SolasCure DermaRite Industries Argentum Medical Recent Developments-

In February 2026, SolasCure announced the successful completion of its Phase II (CLEANVLU2) clinical trial for Aurase Wound Gel, a biofilm-targeting enzymatic hydrogel.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 956.41 Million |

| Market Size in 2026 | USD 1,054.52 Million |

| Market Size in 2034 | USD 2,164.55 Million |

| CAGR | 9.41% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Mode of Mechanism, By Application, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Anti-Biofilm Wound Dressing Market Segments By Mode of Mechanism-

Physical

-

Manual Debridement

Pulse Electrical Field

Ultrasound Debridement

-

Ionic Silver

Iodine

EDTA

Others

-

Dispersin B

Lactoferrin

Bacteriophage

Others

-

Chronic Wounds

-

Diabetic Foot Ulcers

Pressure Ulcers

Venous Leg Ulcers

Others

-

Surgical & Traumatic Wounds

Burn Wounds

-

Hospitals

Specialty Clinics

Home Healthcare

Other End Users

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment