403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Advanced Biofuel Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

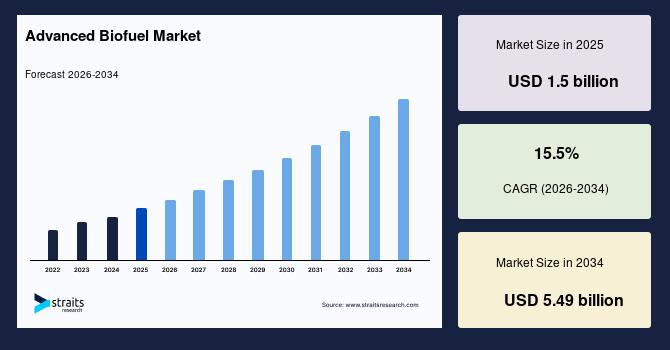

| 2025 Market Valuation | USD 1.5 billion |

| Estimated 2026 Value | USD 1.73 billion |

| Projected 2034 Value | USD 5.49 billion |

| CAGR (2026-2034) | 15.5% |

| Dominant Region | North America |

| Fastest Growing Region | Europe |

| Key Market Players | Abengoa Bioenergy, Eni S.p.A, Q8 Italy, Inbicon A/S, A2BE Carbon Capture LLC |

Download Free Sample Report to Get Detailed Insights.

Emerging Trends in Advanced Biofuel Market Shift toward Second- and Third-Generation BiofuelsShift toward second- and third-generation biofuels, which prioritize sustainability by utilizing non-food biomass, acts as a key market trend. Unlike first-generation biofuels, which rely on food crops, these newer generations use agricultural residues, forestry waste, algae, and industrial by-products, reducing the risk of food competition and supporting a circular economy. This approach addresses both environmental and ethical concerns while providing a consistent, renewable feedstock. Technological advancements in bioconversion, fermentation, and algae cultivation are making these biofuels increasingly viable, efficient, and cost-effective, driving broader adoption in transportation, aviation, and industrial sectors worldwide.

Increasing Corporate Net Zero and Energy Security FocusThe growing emphasis on corporate net-zero commitments and energy security acts as a trend in the market. Companies across aviation, logistics, and heavy transport are increasingly adopting advanced biofuels to reduce carbon emissions in alignment with climate targets and sustainability pledges. Governments and organizations are prioritizing energy diversification to reduce reliance on volatile fossil fuel imports. This has spurred long-term investments, strategic partnerships, and offtake agreements in biofuel production. By integrating advanced biofuels into operations, businesses enhance sustainability credentials and mitigate energy supply risks, supporting a resilient and low-carbon energy transition.

Market Drivers Rising Demand for Renewable Energy and Carbon Reduction Goals Drive MarketThe growing global emphasis on reducing reliance on fossil fuels is a significant driver for the market. Government, industries, and consumers are increasingly prioritizing sustainable energy solutions to mitigate climate change and reduce greenhouse gas emissions. Advanced biofuels, produced from non-food biomass, algae, and waste materials, offer a renewable and environmentally friendly alternative to conventional fuels. Rising energy security concerns and volatile crude oil prices further encourage the adoption of biofuels. Global initiatives and international agreements promoting carbon neutrality are accelerating investments in biofuel production, making them an essential component of the transition toward a sustainable energy future.

Technological innovations in production processes, including cellulosic ethanol, algae-based biofuels, and waste-to-fuel technologies, contribute to the growth of the market. Cellulosic ethanol uses non-food biomass like agricultural residues, increasing feedstock availability and reducing competition with food crops. Algae-based biofuels offer high yields per acre and can grow on non-arable land, making them sustainable and scalable. Waste-to-fuel technologies convert municipal, industrial, and agricultural waste into energy, minimizing environmental impact and lowering raw material costs.

Market Restraints Feedstock Availability, Supply Chain Challenges, and Technological Complexities Restrains Advanced Biofuel Market GrowthThe limited availability of sustainable biomass and the inconsistent supply of feedstocks such as agricultural residues, forestry waste, and algae are hampering market growth. Seasonal variations, competing uses for biomass, and logistical challenges in collection and transportation disrupt continuous production, making large-scale commercialization difficult. Cultivating algae or sourcing residues at sufficient scale requires significant investment in infrastructure, land, and water resources. These supply chain constraints increase production costs and limit the ability of manufacturers to meet growing global demand.

The complexity of production processes, which include biochemical methods like enzymatic hydrolysis and fermentation, as well as thermochemical processes such as gasification and pyrolysis. These technologies require specialized equipment, highly skilled personnel, and continuous research and development to optimize efficiency and yields. High capital and operational expenditures associated with these processes increase the overall cost of advanced biofuels, limiting their competitiveness against conventional fossil fuels. Technological challenges in scaling up from pilot to commercial production create uncertainty for investors and slow widespread adoption in transportation and industrial sectors.

Market Opportunities Aviation Sector and Residue Recycling Offers Growth Opportunities for Advanced Biofuel Market PlayersThe high-margin segments like biojet fuel and renewable diesel are experiencing faster demand growth than conventional ethanol, which acts as an opportunity for the market. Aviation and heavy-duty transport sectors are under increasing pressure to reduce carbon emissions, creating strong demand for sustainable, high-energy fuels. These fuels offer higher revenue per unit due to their specialized applications and regulatory incentives, such as carbon credits and blending mandates. Companies investing in advanced production technologies for biojet and renewable diesel capture premium markets, strengthening strategic partnerships with airlines and fleets, and positioning themselves as leaders in decarbonizing critical transport sectors.

Abundant agricultural residues, municipal solid waste, and non-food biomass enable companies to secure low-cost and locally available feedstock, improving margin stability. Firms invest in waste-to-fuel technologies such as anaerobic digestion, gasification, and cellulosic ethanol to convert low-value waste into high-value fuels. For example, companies in the U.S. and Europe use corn stover and forestry residues to produce cellulosic ethanol at commercial scale. Municipal partnerships allow biofuel producers to utilize urban waste streams, as seen in projects converting city waste into renewable natural gas for transport fleets. Localized biorefineries reduce dependence on long-distance feedstock logistics, lowering operational costs and supply chain risks. This approach also aligns with circular economy goals, helping companies secure government incentives and long-term supply agreements.

Regional Insights North America: Market Dominance by Well-developed Biofuel Production Facilities and Increasing Focus on Environmental SustainabilityNorth America accounted for a market share of 42.1% in 2025 due to well-developed biofuel production facilities and supply chains serving as a critical driver for the advanced biofuel market. The region benefits from established infrastructure, including large-scale biorefineries capable of processing diverse feedstocks such as agricultural residues, forestry waste, and algae. Efficient logistics networks ensure smooth transportation of raw materials and distribution of finished biofuels to end users, including transportation and industrial sectors. This mature ecosystem reduces production costs, enhances reliability, and supports large-volume supply, making advanced biofuels more competitive with conventional fuels. The synergy between production capacity and supply chain efficiency accelerates market adoption and investment in next-generation biofuels.

The increasing focus on environmental sustainability and corporate net-zero commitments is contributing to the growth of advanced biofuels in the US. Airlines are progressively adopting sustainable aviation fuels (SAF), while freight and logistics companies are integrating low-carbon biofuels to reduce greenhouse gas emissions. These measures are particularly critical in hard-to-decarbonize sectors such as aviation, shipping, and long-haul transport, where electrification is challenging. Growing regulatory pressure, carbon reduction targets, and corporate ESG initiatives are boosting demand for advanced biofuels, creating opportunities for market expansion beyond traditional road transport and enhancing long-term growth prospects.

Canada's advanced biofuel market is strongly driven by government regulations and incentives aimed at reducing carbon emissions. The Renewable Fuels Regulations (RFR) mandate that gasoline contain 5% renewable content and diesel contain 2% renewable content, creating stable demand for biofuels. Provincial programs like British Columbia's Low Carbon Fuel Standard (LCFS) provide tradable credits for low-carbon fuels, encouraging producers and distributors to adopt advanced biofuels.

Asia Pacific: Fastest Growth Driven by Focus on Energy Security and Sustainable Aviation Fuel AdoptionAsia Pacific is expected to register a CAGR of 12.5% during the forecast period, driven by rapid industrialization and urbanization. Expanding industries, growing transportation networks, and increasing energy consumption in countries like China and India are creating a pressing need for sustainable, low-carbon fuel alternatives. Advanced biofuels derived from non-food biomass, algae, and waste offer a viable solution to meet this rising energy demand while reducing greenhouse gas emissions. Urban centers, with higher vehicle density and energy-intensive infrastructure, further amplify the requirement for cleaner fuels.

In China substantial investment by domestic companies in facilities converting waste oils and other non-food feedstocks into sustainable aviation fuels (SAF) surges the growth of advanced biofuels in the region. With over USD 1 billion committed, these investments reflect strong industrial confidence in the growth potential of advanced biofuels. The funding supports the development of modern production infrastructure, scaling of bioconversion technologies, and commercialization of SAF for domestic use and export markets. Such initiatives enhance China's energy security and carbon reduction goals and position the country as a competitive player in the global low-carbon aviation fuel sector.

The government's mandatory target for sustainable aviation fuel (SAF) adoption, requiring 10% of aviation fuel for international flights to be SAF by 2030, drives the growth of the advanced biofuel market in Japan. This policy creates a strong regulatory framework in Japan that stimulates industry investment, encourages technology development, and supports the scale-up of domestic SAF production. Airlines and fuel producers are aligning with these targets, investing in infrastructure and supply chains to meet demand. The directive drives market growth in aviation biofuels and reinforces Japan's broader carbon reduction and energy transition goals, boosting long-term sector expansion.

By ProcessThe biochemical process segment dominated the market in 2025 and is expected to grow at a rate of 8.8% during the forecast period. These fuels, produced through fermentation and transesterification of biomass such as sugarcane, corn, and agricultural residues, are extensively adopted in transportation across North America, Europe, and parts of Asia. Their established supply chains and compatibility with existing fuel infrastructure create consistent demand, making the segment highly reliable. Government policies and blending mandates further incentivize production and consumption. Ongoing research to improve yields from cellulosic and non-food biomass strengthens the segment's growth potential, supporting sustainable energy goals worldwide.

The thermochemical process segment is expected to grow at a CAGR of 13.5% during the forecast period, driven by its ability to convert a wide variety of feedstocks such as agricultural residues, municipal solid waste, and algae into high-energy biofuels through gasification, pyrolysis, and hydrothermal liquefaction. These technologies produce versatile fuels, including bio-oil, syngas, and drop-in fuels suitable for aviation, shipping, and heavy transport, where conventional biofuels fall short. The flexibility to use non-food and waste biomass aligns with sustainability and circular economic goals. Along with government incentives for low-carbon fuels and increasing industrial adoption, thermochemical processes are rapidly expanding, making this segment the fastest-growing in the market.

By TypeThe biodiesel segment accounted for a share of 46.5% in 2025, driven by its well-established production from vegetable oils, animal fats, and waste oils, which ensures a reliable supply chain and consistent market availability. Its compatibility with existing diesel engines allows seamless integration into transportation and industrial sectors without requiring significant infrastructure changes. Government mandates, such as the US Renewable Fuel Standard (RFS) and the EU Renewable Energy Directive, provide regulatory support and incentivize production and consumption. Additionally, biodiesel offers substantial environmental benefits by reducing greenhouse gas emissions and particulate matter, making it a preferred choice for countries pursuing decarbonization and sustainability goals.

The cellulosic advanced biofuels segment is expected to register a CAGR of 14% during the forecast period, driven by its use of non-food feedstocks such as agricultural residues, forestry waste, and dedicated energy crops, which minimizes competition with food supply and enhances sustainability. This approach allows for large-scale production without impacting food prices or availability. Cellulosic biofuels offer significant environmental benefits, including up to 90% lower greenhouse gas emissions compared to conventional fossil fuels, aligning with stringent climate policies worldwide. Technological advancements in enzymatic hydrolysis, fermentation, and biomass pretreatment are improving yields and reducing production costs, making cellulosic biofuels increasingly viable for transportation, aviation, and industrial applications.

By Raw MaterialThe lignocellulose segment accounted for a market share of 52.65% in 2025, driven by the widespread availability of biomass, including agricultural residues, forestry waste, and dedicated energy crops. This abundant and renewable feedstock provides a reliable and cost-effective raw material source for producing cellulosic ethanol and other advanced biofuels. Utilizing non-food biomass ensures sustainability and avoids competition with food production, aligning with global environmental and climate policies. Government incentives and blending mandates further support its adoption in North America, Europe, and the Asia-Pacific. Additionally, advancements in pretreatment, enzymatic hydrolysis, and fermentation technologies are improving yields and reducing production costs, strengthening market growth.

The algae segment is expected to grow at a CAGR of 17% during the forecast period, driven by its exceptionally high oil yield per hectare, far surpassing traditional crops like soy or palm, making it an extremely efficient feedstock. Algae cultivation does not compete with arable land or freshwater resources, allowing sustainable production at scale. It can be processed into biodiesel, biojet fuel, and other advanced biofuels, meeting the demand for low-carbon, high-energy-density fuels in transportation and aviation. Technological advancements in bioreactors, strain optimization, and extraction methods are reducing production costs, while government incentives and carbon reduction targets further accelerate algae-based biofuel adoption globally.

Competitive LandscapeThe advanced biofuel market is highly fragmented, with a diverse mix of established multinational energy companies, specialty biofuel producers, and emerging startups focusing on innovative technologies. Established players primarily compete on production capacity, global distribution networks, regulatory compliance, and partnerships with governments or large industries. Emerging companies differentiate themselves through technological innovation, cost-efficient processes, and niche feedstock utilization, such as algae or waste-to-fuel solutions. Collaboration, strategic investments, and intellectual property are also key competitive levers. Advancements in sustainable feedstock sourcing, scalable technologies, and supportive policies will continue to shape market dynamics and growth trajectories.

List of Key and Emerging Players in Advanced Biofuel Market Abengoa Bioenergy Eni S.p.A Q8 Italy Inbicon A/S A2BE Carbon Capture LLC Clariant Bangchak Petroleum Plc DowDuPont Inc Fujian Zhongde Energy Co., Ltd Algenol Biotech GranBio Chemtex Company Recent Developments-

In April 2026, Eni S.p.A. and the European Investment Bank entered into a USD 576.92 million financing agreement to convert the Sannazzaro refinery into a biofuel production facility.

In February 2026, Eni S.p.A. and Q8 Italy partnered to build an advanced biorefinery to process waste, residues, and vegetable oils into advanced biofuels.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.5 billion |

| Market Size in 2026 | USD 1.73 billion |

| Market Size in 2034 | USD 5.49 billion |

| CAGR | 15.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Process, By Type, By Raw Material |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Advanced Biofuel Market Segments By Process-

Biochemical Process

Thermochemical Process

-

Cellulosic Advanced Biofuels

Biodiesels

Biogas

Biobutanol

Others

-

Lignocellulose

Jatropha

Camelina

Algae

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment