403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Iot In Construction Market Size, Scope, Share To 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

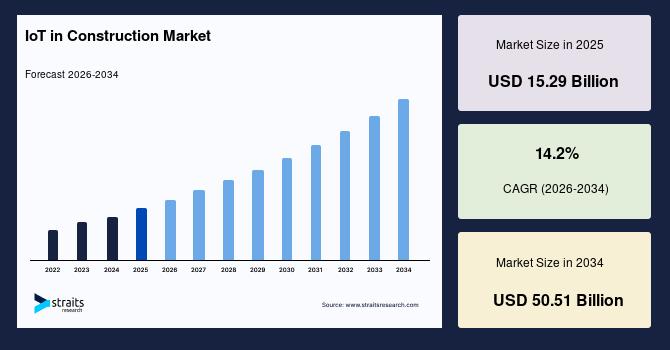

| 2025 Market Valuation | USD 15.29 Billion |

| Estimated 2026 Value | USD 17.46 Billion |

| Projected 2034 Value | USD 50.51 Billion |

| CAGR (2026-2034) | 14.2% |

| Dominant Region | Asia Pacific |

| Fastest Growing Region | North America |

| Key Market Players | Trimble, Inc., Pillar Technologies Inc., Triax Technologies, Inc., AOMS Technologies, Topcon Corporation |

Download Free Sample Report to Get Detailed Insights.

IoT in Construction Market Drivers Proper safety management on construction sites to aid growthThe construction sector employs many people and works in hazardous conditions. OSHA (Occupational Safety and Health Administration), a branch of the U.S. Department of Labor, reports that over 252,000 construction sites employ over 6.5 million people in the United States. Compared to the national average for all other U.S. industries, the construction sector has a much higher risk of fatal injuries. The lack of appropriate protective equipment, trench collapse, falls, scaffold collapse, repetitive motion injuries, and other risks are common at construction sites. IoT integration in the building industry allows for real-time safety monitoring on sites through smart wearables, including smart glasses, wearable sensors, safety vests, exoskeletons, smart helmets, and others.

Additionally, measurements of respiration and heart rates, as well as active monitoring of a worker's physiological response to a particular work environment, are all made possible by such wearable technology. In addition, around 83% of contractors believe that wearable technologies might enhance site safety and reduce fatal injuries on the job site, including fall prevention, which accounts for approximately 30% of construction fatalities. Therefore, benefits like microsleep prevention, fall prevention, smart monitoring of hazardous gases, vital sign tracking, and others may increase demand for IoT-based wearables on construction sites, propelling IoT growth in the construction market.

Growing efficiency and productivity in construction areas to drive marketIoT-based technologies connect construction sites using sensors, drones, CCTV cameras, and Radio-frequency Identification (RFID) tags to gather real-time data on the employees, inventory, and ongoing activities. Among other advantages, sensors and RFID tags on materials allow for efficient workflows, proactive material ordering, equipment servicing, monitoring of equipment usage, and preventative maintenance. Effective time management on construction sites reduces equipment and employee downtime, which saves time and money lost to delays. As a result, using IoT technologies like BIM and others increases productivity and efficiency on building sites, which stimulates the market for IoT in the construction industry.

Market Restraint Growing security threats to hinder market growthMost third-party businesses in business operations maintain networks and information technology systems. Cyberattacks, which may be targeted and organized, are risks while processing and maintaining data gathered by IoT-connected devices. This jeopardizes the data's integrity and confidentiality. Additionally, such cyberattacks harm consumers' reputations in addition to their information, which could result in fines, government enforcement measures, and other consequences. Such flaws pose a severe risk to IoT implementation, particularly in the construction sector. For instance, almost 36% of industrial executives believe that IoT platforms are their organization's top problem, according to the IBM Global C-suite Study published in 2018 by the IBM Institute for Business Value (IBV).

Market Opportunity Robotics in construction to boost market opportunitiesAlthough robotics has been used in the construction sector for some time, very few commercial robots are still being used on construction sites. Robotic technology integration in the construction sector helps to lessen the need for human labor for tasks like bricklaying, plastering, surveying, welding, and other construction-related jobs. Furthermore, robotic devices use technologies like artificial intelligence, the Internet of Things, and others, making it simple to gather real-time data on the spot without requiring specialized equipment. Additionally, the ability of robots to be monitored and controlled remotely helps to increase efficiency while reducing mortality. As demand for robotics in construction grows, the IoT in construction market share is anticipated to grow.

Regional Analysis The Asia Pacific and North America Will Dominate the Regional MarketThe Asia Pacific will command the market while expanding at a CAGR of 13.71% during the forecast period. As wealth and credit have become more widely available in China and India, the two countries with the largest populations in the world, people in this region have started spending more on various things, from necessities like utilities to luxuries. Thus, Asia-Pacific serves as a promising market for the production and development of hardware and software solutions based on the Internet of Things. The world's largest building market is in Asia-Pacific.

The rapid increase in per capita income, the expansion of metropolitan areas, and the widespread acceptance of new technology all contribute to the growth of the construction industry. The infrastructure in emerging countries like Myanmar, Thailand, the Philippines, Vietnam, and others is being improved with a strong commitment. Thailand, for instance, unveiled its infrastructure plan for 2016 to 2020. By 2025, it plans to invest USD 58.5 billion in new infrastructure improvements. The Myanmar government has also announced an investment of USD 26.8 billion in the National Transport Master Plan to create new roads, water, air, and train infrastructure. Additionally, to support the development of smart cities and maximize productivity at construction sites, China and South Korea have been at the forefront of deploying 5G technology and related IoT infrastructure. This fuels the Asia-Pacific construction market's adoption of IoT in construction projects.

North America will likely grow at a CAGR of 13.11% and hold USD 6,768 million. Due to the rapid acceptance of new technologies on construction sites in the U.S. and Canada, North America is the second-largest consumer of IoT in the construction industry. The strong consumer spending on emerging technologies also encourages Americans to use IoT-connected products. Since many businesses, such as Autodesk, Inc., CalAmp Crop, Oracle Corporation, and others, have their corporate headquarters in the U.S., the cost of new revolutionary technology is also comparatively low in the region. These elements encourage the market for IoT technology in North America, which fuels IoT development in the construction industry.

By ApplicationThe asset monitoring section is projected to advance at a CAGR of 14.37% and hold the largest market share. Asset monitoring or asset management in the construction industry involves the organization of drawings, papers, plans, tools, and equipment. Utilizing smart asset monitoring devices and systems helps to consolidate and centralize asset data, which provides adequate control over their use and location and aids in making decisions regarding their rental, purchase, or relocation. In addition, asset monitoring can aid in determining profitability ratios gleaned from monitoring asset utilization data to determine the ideal usage settings.

The fleet management section will hold the second-largest share. Fleet management, often known as telematics, offers a variety of solutions, including fleet management, vehicle tracking, fleet safety, driver behavior, and efficient driving. Fleet management delivers daily information regarding fleet operations, weak links, equipment downtimes, and forthcoming duties, reducing vehicle downtimes and maximizing vehicle productivity with minimal fuel usage.

By End-UseThe non-residential section is projected to advance at a CAGR of 13.5% and hold the largest market share. Non-residential construction encompasses hospitals, hotels, industrial buildings, and infrastructure projects. Large commercial construction projects necessitate sophisticated planning, designing, and management of assets, staff, resources, and equipment. Adopting IoT technology in non-residential construction operations increases project efficiency and reduces operation delays in various construction activities.

The residential section will hold the second-largest share. Residential structures include apartment complexes, condominiums, and single-family homes. Residential projects typically have limited financial resources, which are challenging to sustain on building sites staffed by humans. Integrating IoT technology into residential construction makes it possible to manage each project phase efficiently.

By ComponentsThe hardware section will most likely expand at a CAGR of 13.58% and hold the largest market share. Using hardware instruments such as radio frequency identification (RFID) tags, sensors, and intelligent systems enhances the construction process's safety, security, and productivity. RFID tags enable vehicle monitoring, improved protection, collision avoidance, raw material routing, and asset tracking, which not only assures the safety of the fleet, workers, and materials but also increases the efficiency of mining operations by reducing fleet downtime.

The services section will hold the second-largest market share. Support and maintenance of mining operations, consulting, and system integration are provided. Adopting engineering services such as retrofitting, regular maintenance, and employee training maintains the equipment's efficiency and productivity, reducing unscheduled or unintentional costs. Recognizing these advantages can contribute to expanding maintenance and support services over the anticipated period.

List of Key and Emerging Players in IoT in Construction Market Trimble, Inc. Pillar Technologies Inc. Triax Technologies, Inc. AOMS Technologies Topcon Corporation Hilti Corporation Autodesk, Inc. Oracle Corporation Hexagon AB CalAmp Corporation Recent Developments-

In March 2026, Trimble Inc. launched an advanced IoT-enabled construction monitoring platform integrating real-time site analytics, machine control, and cloud-based data sharing to improve productivity and safety across large infrastructure projects.

In February 2026, Caterpillar Inc. expanded its Cat® Command and VisionLink® IoT ecosystem with enhanced remote equipment monitoring and predictive maintenance features aimed at reducing downtime in construction fleets.

In January 2026, Hexagon AB introduced new IoT-integrated smart construction solutions under its Geosystems division, enabling digital twin-based project tracking and real-time asset monitoring for infrastructure projects.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.29 Billion |

| Market Size in 2026 | USD 17.46 Billion |

| Market Size in 2034 | USD 50.51 Billion |

| CAGR | 14.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Application, By End-User, By Component |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

IoT in Construction Market Segments By Application-

Asset Monitoring

Predictive Maintenance

Fleet management

Wearables

Remote Operations

Others

-

Residential

Non-residential

-

Hardware

Software

Connectivity

Services

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment