403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Oxygen Therapy Devices Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

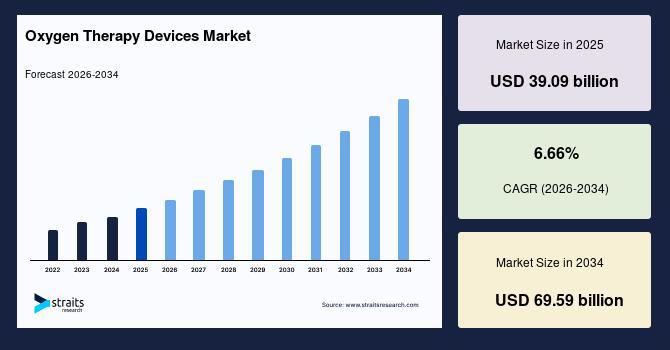

| 2025 Market Valuation | USD 39.09 billion |

| Estimated 2026 Value | USD 41.55 billion |

| Projected 2034 Value | USD 69.59 billion |

| CAGR (2026-2034) | 6.66% |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Ventec Life Systems, Inc., Unitaid, VARON, MedAccess, Inogen, Inc. |

to learn more about this report Download Free Sample Report

Emerging Trends in Oxygen Therapy Devices Market Shift toward Low-noise DevicesDemand for low-noise oxygen therapy devices rises as patients require uninterrupted sleep quality, especially in long-term home care cases such as COPD and sleep apnea. A European Respiratory Review study evaluated randomized trials and found that nocturnal oxygen therapy significantly reduces apnea–hypopnea index (AHI), reinforcing its ongoing clinical relevance in sleep-related breathing disorders. This trend pushes the market toward compact and acoustically optimized concentrators and PAP devices, which enhances patient adherence and therapy continuity. Manufacturers respond by redesigning internal airflow systems and motor structures to reduce sound levels, which increases product differentiation and encourages premium pricing for comfort-focused devices.

Increasing Preference for Connected Therapy SystemsHealthcare providers adopt connected oxygen therapy systems that allow real-time monitoring of oxygen saturation and device performance. For instance, the myCAIRE telehealth system connects concentrators to smartphones or tablets and transmits real-time data such as oxygen usage, flow rates, and device alerts to healthcare providers. This trend strengthens clinical decision-making and reduces emergency interventions, which expands the value of oxygen therapy beyond basic supply. Manufacturers incorporate sensors and connectivity features that align with telehealth ecosystems, which improves product relevance in digital healthcare environments and supports long-term service-based revenue models.

Market Drivers Clinical Emphasis on Early Oxygen Intervention and Need for Post-acute Recovery Plans Drives MarketMedical guidelines increasingly support early oxygen supplementation in moderate respiratory impairment to prevent disease progression and complications, as reflected in recommendations from the World Health Organization, which advises oxygen therapy for patients with hypoxemia in acute and chronic conditions. The Global Initiative for Chronic Obstructive Lung Disease recommends long-term oxygen therapy in COPD patients with persistent low oxygen levels. This clinical shift expands the eligible patient base and increases prescription rates across both hospital and home settings. Manufacturers benefit from higher device utilization across earlier disease stages, which creates demand for a wider range of products, including entry-level and portable systems tailored for non-critical patients.

Healthcare systems focus on reducing hospital stay duration, which places oxygen therapy devices at the center of post-acute recovery plans. Patients discharged after respiratory events require continued oxygen support at home or rehabilitation centers, which drives demand for portable and easy-to-operate devices. Manufacturers align product design with discharge protocols and caregiver usability, which strengthens partnerships with hospitals and increases repeat procurement tied to patient transition programs.

Market Restrains Oxygen Purity Compliance Challenges and Dependence on Stable Power Supply Restrains Oxygen Therapy Devices Market GrowthStrict regulatory requirements for oxygen purity and device performance create barriers in product approval and market entry, including standards such as the World Health Organization requirement for oxygen concentrators to deliver ≥82% oxygen purity, the US Food and Drug Administration classification of oxygen therapy devices under stringent medical device approval pathways (e.g., 510(k) clearance), and the International Organization for Standardization ISO 80601-2-69 standard that specifies safety and performance requirements for oxygen concentrator equipment. Any deviation in concentration levels affects patient safety, which leads to rigorous testing and certification processes. This restraint slows product launches and increases compliance costs for manufacturers, which limits rapid innovation cycles and places pressure on smaller players that lack advanced quality assurance infrastructure.

Oxygen concentrators rely on continuous electricity supply, which creates limitations in regions with unstable power infrastructure. This constraint reduces device reliability in critical care scenarios and restricts adoption in rural or underdeveloped areas. Manufacturers face pressure to develop battery-backed or hybrid solutions, which increases production complexity and cost while requiring additional investment in energy-efficient technologies.

Market Opportunities Need for Specialized Pediatric Care and Investments in Emergency Oxygen Infrastructure Offer Growth Opportunities for Oxygen Therapy Devices Market PlayersRising focus on specialized respiratory care for infants creates demand for oxygen therapy devices designed with precise flow control and enhanced safety features, supported by clinical guidance from the World Health Organization, which recommends oxygen therapy for children with hypoxemia and pneumonia, one of the leading causes of death in children under five globally. This opportunity expands the market into neonatal intensive care units and pediatric home care segments for pediatric hospital admissions in low- and middle-income countries that require oxygen support. Manufacturers develop highly sensitive delivery systems and miniaturized components, aligning with standards from the American Academy of Pediatrics that emphasize precise oxygen dosing in neonates to avoid complications such as oxygen toxicity and retinopathy of prematurity. These requirements drive innovation in low-flow oxygen delivery systems capable of accurate titration and continuous monitoring in fragile patient populations. As a result, this creates new revenue streams and strengthens product portfolios with niche clinical applications while addressing critical unmet needs in neonatal and pediatric respiratory care.

Governments and healthcare institutions invest in emergency oxygen infrastructure to handle sudden respiratory crises and disaster scenarios, supported by regulatory and preparedness frameworks such as the National Fire Protection Association NFPA 99 code, which mandates reliable medical gas systems and backup oxygen supply in healthcare facilities. This creates demand for scalable and rapidly deployable oxygen systems such as modular concentrator units and portable cylinders, as reinforced by the Centers for Medicare & Medicaid Services emergency preparedness rule requiring hospitals to maintain essential equipment and continuity systems for patient care. Manufacturers gain opportunities to supply bulk and emergency-ready solutions, aligning with infrastructure upgrades encouraged by the Health Resources and Services Administration, which supports facility resilience and capacity building in critical care services. These frameworks emphasize redundancy, rapid deployment capability, and system reliability during emergencies and disasters. As a result, this drives innovation in durable, interoperable oxygen delivery systems capable of supporting large-scale healthcare responses.

Regional Insights North America: Market Leadership Driven by Reimbursement-Backed Home OxygenNorth America oxygen therapy devices dominated the market with a share in 2025 due to structured reimbursement frameworks and clinical eligibility pathways that support long-term oxygen use. The US Centers for Medicare & Medicaid Services confirms coverage of home oxygen therapy for patients with hypoxemia, which ensures consistent device demand across chronic and acute care cases. High healthcare expenditure and institutional adoption of respiratory care protocols strengthen procurement of advanced oxygen delivery systems. The region also benefits from strong domestic manufacturing and rapid uptake of portable concentrators aligned with home-based treatment models.

The US market expands due to defined replacement cycles and reimbursement structures that ensure recurring demand for oxygen equipment. CMS policy establishes a five-year reasonable useful lifetime for oxygen devices, which creates predictable replacement demand across patient populations. The bundled payment model that includes accessories and maintenance supports continuous device utilization. Strong clinical emphasis on chronic respiratory disease management and widespread adoption of patient-centered care models reinforce demand for technologically advanced and portable oxygen therapy devices across both institutional and home settings.

The Canada oxygen therapy devices market shows stable growth due to its publicly funded healthcare system that ensures access to essential respiratory therapies across provinces. Provincial health programs support oxygen therapy provision for chronic disease patients, which strengthens adoption in home care environments, including initiatives such as the Assistive Devices Program, Home Oxygen Program, Alberta Aids to Daily Living, and Home Oxygen Therapy Program that provide funding or reimbursement for home oxygen equipment and related services. The country places emphasis on community-based respiratory management, which reduces hospital burden and increases demand for portable oxygen concentrators. National focus on rural healthcare delivery encourages deployment of reliable and low-maintenance oxygen systems, which supports consistent device utilization across geographically dispersed populations.

Asia Pacific: Fastest Growth Driven by Healthcare Infrastructure ExpansionThe Asia Pacific oxygen therapy devices market is expected to register the fastest growth with a CAGR of 8.66% during the forecast period due to large-scale healthcare infrastructure expansion and rising awareness of respiratory care. Governments across the region invest in hospital capacity, emergency preparedness, and oxygen supply systems, which increases demand for both source equipment and delivery devices. The region also benefits from a rising elderly population and improved diagnosis rates of respiratory disorders. Local manufacturing expansion reduces device cost and improves accessibility, which supports adoption across both urban and semi-urban healthcare facilities, positioning the region as the fastest-growing market globally.

China experiences strong growth due to high exposure to air pollution and a large patient base with respiratory conditions. Urbanization and industrial emissions contribute to increased incidence of lung diseases, which drives demand for oxygen therapy devices, as evidenced in China, where air pollution is responsible for around 2 million deaths annually and is a major contributor to conditions such as chronic obstructive pulmonary disease (COPD) and lung cancer. The country also benefits from large-scale domestic manufacturing capabilities that reduce dependence on imports and lower device costs. Government focus on strengthening medical supply chains and hospital infrastructure supports widespread availability of oxygen equipment, which ensures rapid adoption across both public hospitals and home care settings.

The South Korea oxygen therapy devices market demonstrates growth due to the integration of digital health technologies with respiratory care. The country promotes smart hospital systems and remote patient monitoring, which supports connected oxygen therapy devices with real-time tracking features. Strong national insurance coverage enables access to advanced respiratory treatments, supported in South Korea by the National Health Insurance Service and the Health Insurance Review and Assessment Service, which provide broad reimbursement for oxygen therapy, home respiratory care, and related medical devices, thereby improving patient access and treatment adherence. High penetration of home healthcare services and emphasis on early disease diagnosis contribute to increased use of PAP devices and portable oxygen systems. The healthcare system prioritizes technology-driven efficiency, which supports adoption of compact and intelligent oxygen therapy solutions.

Japan shows steady expansion due to its rapidly aging population and structured home healthcare ecosystem. High life expectancy results in a larger population with chronic respiratory conditions, which creates a sustained need for long-term oxygen therapy. The country emphasizes compact, quiet, and energy-efficient devices tailored for elderly patients, which drives innovation in concentrators and PAP systems. Healthcare policies support home-based treatment to reduce hospital dependency, which strengthens demand for portable and user-friendly oxygen therapy devices designed for continuous and safe use.

By ProductThe oxygen delivery devices segment is expected to grow at a CAGR of 7.45% during the forecast period. The growth is driven by its direct role in patient interface and therapeutic efficiency. Rising preference for non-invasive respiratory support and precise oxygen administration supports demand for masks, nasal cannulas, and Venturi systems. Hospitals and home care settings prioritize comfort, disposability, and infection control, which strengthens adoption. Technological improvements in material design and ergonomic fit enhance patient compliance, while expanding emergency and critical care infrastructure increases consistent utilization across diverse clinical conditions.

The oxygen source equipment segment is expected to grow at a CAGR of 7.12% during the forecast period, as healthcare systems shift toward reliable and continuous oxygen supply solutions. Portable oxygen concentrators gain traction due to mobility benefits and suitability for home healthcare. The increasing prevalence of chronic respiratory diseases supports demand for both fixed and portable systems. Cost efficiency over long-term use compared to cylinders strengthens adoption. Technological advancements improve energy efficiency and device lifespan, which encourages healthcare providers and patients to transition toward concentrator-based oxygen generation systems.

By ApplicationChronic obstructive pulmonary disease dominated the application segment with a share of 43.23% in 2025 due to its high global prevalence and long-term oxygen dependency in advanced stages. Patients require continuous oxygen therapy to maintain adequate blood oxygen levels, which drives sustained demand for concentrators and delivery devices. An aging population and exposure to pollutants contribute to disease burden. Clinical guidelines strongly recommend oxygen therapy for severe cases, which ensures consistent utilization across hospital and home care settings, reinforcing its leading market position.

The obstructive sleep apnea segment is expected to have the fastest growth, registering a CAGR of 7.61% during the forecast period, as awareness and diagnosis rates improve across both developed and emerging regions. Rising obesity levels and sedentary lifestyles contribute to higher incidence. PAP devices such as CPAP and BiPAP serve as primary treatment options, which increases demand within this segment. Expansion of sleep clinics and home-based diagnostic solutions supports early intervention. Patients show preference for home treatment, which drives adoption of compact and user-friendly devices with enhanced comfort features.

By End UseHome healthcare emerges as the fastest-growing end-use segment with a CAGR of 7.56% due to a shift toward decentralized care and cost-containment strategies. Patients with chronic respiratory conditions prefer treatment within home settings for convenience and reduced hospital visits. Availability of portable concentrators and easy-to-use delivery devices supports this transition. Healthcare systems encourage home care to reduce burden on hospitals. Reimbursement support in several regions and a rising elderly population further strengthen demand for oxygen therapy devices in home environments.

The non-home healthcare segment is expected to register a CAGR of 7.34% due to sustained demand from hospitals, clinics, and emergency care units that require continuous and high-flow oxygen therapy support. Critical care admissions, surgical procedures, and acute respiratory conditions create consistent utilization of oxygen delivery and source equipment. Healthcare facilities invest in centralized oxygen systems and advanced monitoring integration to ensure reliability and patient safety. Expansion of hospital infrastructure and rising ICU capacity across emerging regions strengthen this segment, while strict clinical protocols maintain steady equipment replacement and upgrades.

Competitive LandscapeThe oxygen therapy devices market exhibits a moderately fragmented structure, with a mix of large multinational medical device companies and numerous regional and niche manufacturers operating across product categories such as concentrators, cylinders, and delivery systems. Established players maintain strong positions through broad product portfolios, global distribution networks, regulatory expertise, and continuous investment in advanced technologies such as portable and IoT-enabled devices. In contrast, emerging and mid-sized players compete on cost efficiency, localized manufacturing, rapid product customization, and targeted penetration in price-sensitive and developing markets, often addressing supply gaps and unmet demand with agile strategies. Competitive intensity also reflects partnerships with healthcare providers and reimbursement alignment as key differentiation factors among leading companies.

List of Key and Emerging Players in Oxygen Therapy Devices Market Ventec Life Systems, Inc. Unitaid VARON MedAccess Inogen, Inc. ICU Medical ResMed HERSILL S.L. OMRON Healthcare GE Healthcare Fisher & Paykel Healthcare Limited Respironics Tecno-Gaz Industries Allied Healthcare Products, Inc. Teleflex Incorporated Chart Industries DeVilbiss Healthcare Drägerwerk AG & Co. KGaA Linde Caire Medical Rhythm Healthcare Laboratory Informatics Market Recent Developments In January 2026, VARON introduced the VP 8 Lite portable oxygen support device, offering a new option in the personal oxygen therapy category aimed at everyday patient use. In December 2025, VARON partnered with FOSSVI (Fundación Obras Sociales de San Vicente, IAP) to donate home oxygen concentrators to elderly and vulnerable community groups in Mexico. In July 2025, MedAccess, Unitaid, and the Clinton Health Access Initiative (CHAI) announced a volume guarantee financing agreement with Synergy Gases Ltd. to boost production and distribution of affordable medical oxygen in sub-Saharan Africa, helping hospitals access lifesaving oxygen under agreed volume targets. Report Scope| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 39.09 billion |

| Market Size in 2026 | USD 41.55 billion |

| Market Size in 2034 | USD 69.59 billion |

| CAGR | 6.66% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Product, By Application, By End Use |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

to learn more about this report Download Free Sample Report

Oxygen Therapy Devices Market Segments By Product-

Oxygen Source Equipment

-

Oxygen Cylinders

-

Fixed

Portable

-

Fixed

Portable

-

CPAP

APAP

Bi-PAP

-

Oxygen Masks

Nasal Cannula

Venturi Masks

Non-rebreather Masks

Bag Valve Masks

CPAP Masks

Others

-

Chronic Obstructive Pulmonary Disease

Asthma

Obstructive Sleep Apnea

Respiratory Distress Syndrome

Cystic Fibrosis

Pneumonia

Others

-

Home Healthcare

Non-home Healthcare

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

Comments

No comment