403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

US Electric Vehicle Transition Delayed But Not Derailed By Subsidy Exit

(MENAFN- ING)

Dropping both carrot and stick slows US electric vehicle trend

last datapoint: September Source: ANL GOV, ING Research EV sales hit record highs before subsidy deadline

*forecast based on current regulations and plans Source: BNEF, S&P, ACEA, ANL Gov, ING Research EV market share to face setback to 8.5% in 2026

Source: GOV Bureau of Economic Analysis Subsidy exit to gradually feed through

US tax credits for electric vehicles – up to $7,500 for a new full electric EV and up to $4,000 for a used EV – ended on 1 October under the One Big Beautiful Bill Act (OBBBA). This changes the economics of driving EVs, and in turn makes them less attractive.

In August, average new EV purchase prices before tax credits stood at $57,245, still some $9,000 more than a new petrol car ($48,100). Subsidies largely filled the price gap, with almost 90% of new EV buyers in 2024 receiving the incentives .

The globally-lagging EV transition in the US will now be delayed even further, as the administration aims to relax vehicle emission reduction obligations for 2032 . Industry players are cutting their production (scaling) plans accordingly, refocusing on hybrids but also continuing to invest in and develop new EV product portfolios in the background.

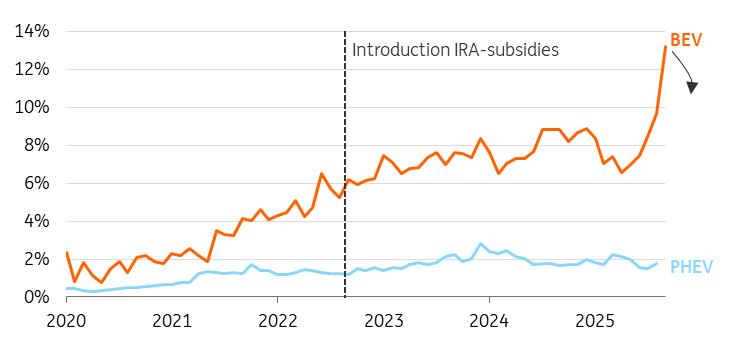

US electric car share in new sales in jumped before tax credit exitShare of battery electric vehicles (BEV) and plug-in hybrid electric vehicle (PHEV) in total new registrations in the US, per month

last datapoint: September Source: ANL GOV, ING Research EV sales hit record highs before subsidy deadline

In the months leading up to the subsidy deadline of 30 September 2025, consumers rushed to secure EV tax credits, resulting in a record influx of new electric vehicles. In September, the share of new EV sales – including battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) – surged to 13% of total new light-duty vehicle sales, lifting the third-quarter average to 10.5% from 7% in the second quarter. Tesla, General Motors, and, to a lesser extent, Ford and Stellantis benefited from this surge.

However, EV sales are expected to decline during the remainder of 2025 – although thanks to front-loading, we anticipate that the full-year EV share will reach 10% (equivalent to 1.6 million units), slightly exceeding the 2024 level. Following a surge ahead of US President Donald Trump's 'Liberation Day' tariffs, it's been a tumultuous year for the US car market.

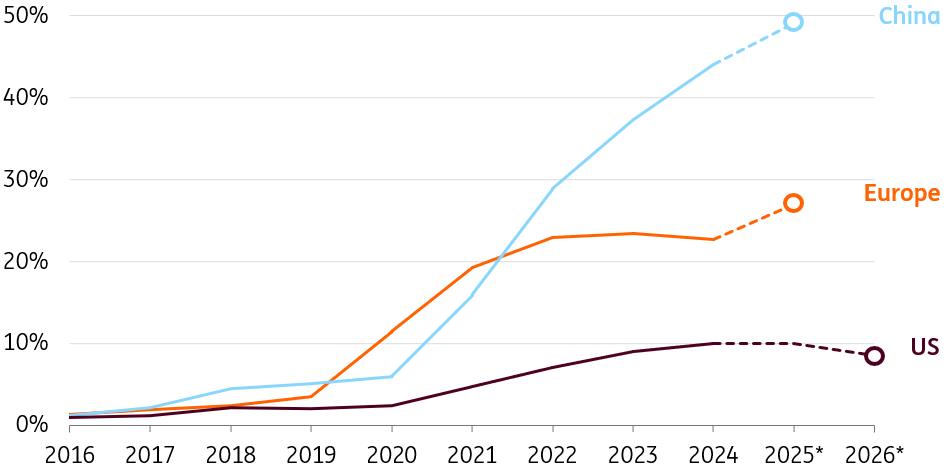

US EV-share to dip in 2026, growing the gap with Europe and ChinaShare of electric vehicles (BEV + PHEV) in total new car registrations per region

*forecast based on current regulations and plans Source: BNEF, S&P, ACEA, ANL Gov, ING Research EV market share to face setback to 8.5% in 2026

Electric vehicle sales have increased from 6.8% in 2022 to 10% in 2025 (around 1.6 million vehicles), supported by federal incentives. However, a correction following front-loading, along with waning consumer interest, is expected to push EV market share back down to around 8% in 2026. At the same time, internal combustion engine (ICE) vehicles and conventional hybrids (HEVs) are likely to gain more traction. We expect EV share to recover in 2027, but this will result in several years of stagnation, delaying the pace of electrification. The setback will widen the gap with China, where electrification is already far ahead, and also with Europe.

Three reasons why the structural EV slowdown won't be as bad as you would thinkIncentives have been terminated and the momentum behind green considerations supporting EV sales has weakened, while carmakers are expected to recalibrate their strategies and shift advertising efforts toward conventional cars and hybrids. However, beyond the possibility of a more EV-friendly future administration, there are a few encouraging signs for the future.

-

EVs can still be financially attractive: A growing number of US drivers already find that electric vehicles offer lower per-mile costs compared to internal combustion engine vehicles, though this varies by state due to differences in excise duties. With the average American driving around 13,500 miles annually, frequent drivers in urban areas may find EVs economically viable even without subsidies. Research shows that the total cost of ownership (TCO) for EVs can still be lower than that of ICE vehicles over ownership periods of five years or more, across all states – even in the absence of tax credits and despite significant variation in excise taxes.

A growing EV market existed before federal incentives: Subsidies in the US were less successful than in other countries, such as those in Europe, suggesting a more gradual adoption curve. Not all EV models were eligible for subsidies, and a market for EVs existed even before the introduction of the incentive scheme.

EV prices are expected to decline further: The relative prices of EVs compared to ICE vehicles are expected to continue falling as battery costs decrease, improving the overall value proposition. A maturing market and increased competition have previously helped drive down EV prices, and this trend is likely to continue.

While the US car market is slowing down for new electric vehicles, the secondhand EV market is gaining momentum. In August, used EV sales rose by 59% year-on-year – far outpacing the growth seen in new EV sales – and this momentum is likely to continue. Several factors are driving this trend:

-

Price convergence : The price gap between used EVs and used internal combustion engine vehicles has narrowed to just $1,000 recently , making used EVs more attractive to buyers.

Lease returns : Many EV leases signed during the first wave of adoption in 2022 (typically lasting three years) are now ending. This will bring a larger supply of used EVs to the market over the next two years, increasing their share in the US used car pool.

Price levelling : The growing flow of returning EVs could further align prices with ICE vehicles.

Admittedly, tax credits for used EVs have also ended. However, given the limited price gap between used EVs and ICE vehicles, the impact on the secondhand EV market is expected to be much milder than on the new EV market.

Auto loan debt pressure could affect used car market

However, a growing risk for the car market in general – and the secondhand EV market in particular – is the increasing stress from auto loans. The 90+ day delinquency rate for auto loans has recently climbed to levels comparable to those seen during the financial crisis and the Covid-19 pandemic. This rise is likely driven by lower-income groups, who tend to purchase secondhand vehicles rather than new ones. While we do not expect this trend to significantly suppress overall sales, smaller lenders may become more cautious and less willing to extend car loans to lower credit score buyers in the secondhand market.

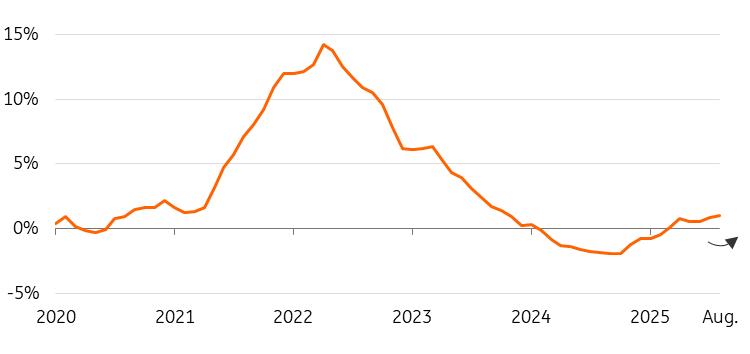

US car prices have barely seen increases so far following Trump's tariffs, but this is unlikely to holdUS consumer price index for new autos YoY

Source: GOV Bureau of Economic Analysis Subsidy exit to gradually feed through

Carmakers absorbed most of the tariff burden during the uncertain period following the implementation and subsequent negotiations. But this approach is unsustainable, despite significant pressure on companies to continue bearing the costs.

In anticipation of the phasing out of tax credits, EV manufacturers also introduced rebates, discounts, and financing deals to reduce inventories. General Motors and Ford pledged to extend EV lease subsidies through the fourth quarter of 2025, while Stellantis and Hyundai offered incentives for both leasing and purchasing. Yet these measures are unlikely to last much longer. After an initial adjustment period, average car prices are expected to rise by 4-8% across the board to offset the tariff burden, excluding the impact of tariffs on steel products, according to Cox Automotive.

Carmakers recalibrate, but the future remains electricThe policy U-turn on EVs ultimately doesn't alter the long-term shift of the automotive industry. While the termination of federal EV incentives and emissions targets gives carmakers more flexibility to optimise their production portfolios and improve short-term profitability, the shift is strategic rather than ideological. For instance, Ford is narrowing its EV lineup to focus on a few models with longer driving ranges and expanding its hybrid offerings. GM is also scaling back EV production in the short term.

At the same time, carmakers continue to invest in electrification, recognising that the future of mobility remains electric. This transitional period presents a critical opportunity to accelerate the development of domestic supply chains – especially for batteries. GM, still reliant on Chinese battery imports , is partnering with LG and Samsung to establish domestic battery production. BMW is planning a battery factory near its Spartanburg site in collaboration with AESC, while Ford is working with CATL and SK to boost US-based battery output. The new reality also challenges manufacturers to innovate and reduce production costs. Ford's announcement of a universal EV platform for pickup trucks is a clear example. Combined with expected declines in battery prices, these developments should help make EVs more accessible to a broader range of consumers in the years ahead.

Crackdown on state-level regulations could slow the frontrunnersEV adoption in the US also varies significantly by state. California, thanks to its unique authority to set stricter-than-federal vehicle standards, leads with a 22% EV registration rate in the first half of 2025. In contrast, the 10 most rural states have seen minimal uptake . Nearly 40 other states and the District of Columbia have implemented policies such as emissions standards and EV rebates to support adoption.

However, states' ability to promote their own EV industries is under pressure. In June, Trump signed three congressional resolutions aimed at revoking California's authority to regulate vehicle emissions under the Clean Air Act. The initiative is now being challenged in court. If upheld, California would need to rely on alternative channels to support EV sales, potentially slowing adoption.

Continuous infrastructure development remains key to EV growthEV charging networks in the US have continued expanding steadily in 2025 despite recent policy changes. According to BloombergNEF, 703 high-speed public charging stations became operational in the second quarter, marking the second-highest quarterly total on record.

However, this momentum may not be sustained. Only pre-contracted funding under the $5 billion NEVI program can be restored, covering just 16% of the total available for FY2022–2025. Additionally, tax credits for alternative fuel vehicle refuelling property are set to expire on 30 June 2026, which could further constrain development. Expanding charging infrastructure remains essential to overcoming range anxiety – a key barrier to EV adoption. The US still has one of the lowest charging densities globally, with just 0.03 charging points per EV, compared to 0.08 in the EU and 0.1 in China.

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment