![SANS Institute, Cloud Security Alliance, [Un]Prompted, And OWASP Genai...](/Updates/index/HTML_Images/NewsEN_MostPopular_img_4.png?1110991251)

403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

The Bank Of Korea Surprised The Market With A 25Bp Cut Today

| 3.0% |

7-day repo rate

Down from 3.25% |

| Lower than expected |

Today's monetary policy meeting had some unusual features that have not been seen often in recent monetary policy meetings. Given the high level of uncertainty in the global economy and financial markets, it is unusual for the Bank of Korea to cut interest rates twice in a row, except in times of crisis. Usually, the Bank of Korea takes a cautious stance for at least two months after a policy change to monitor its effects. Furthermore, among two dissenting votes, one vote was from the Deputy Governor. It is highly unusual for a deputy governor to vote against a decision. We expect to see continued disagreement among board members over the prioritisation of policy between growth support and financial market stability.

Governor Rhee's remarks showed that he was quite confident that the BoK and the government have sufficient tools to mitigate volatile FX market movements. He mentioned the ongoing discussion about swap agreements with the national pension fund and the large size of FX reserves that can be used to stabilise the FX market if necessary. We interpret today's decision as a reflection of the BoK's considerable concern about weak growth. Three of the six committee members indicated that the option of another rate cut in three months is alive as there is considerable uncertainty about the current growth outlook.

We have changed our outlook for policy rates and the KRWWe had expected the Bank of Korea to be cautious about further easing and that the next cut would be in April. While we thought that the BoK sets its policy rate relative to the Fed and would be concerned about exhausting its policy options by cutting rates early, the surprise rate cut signalled that the BoK's policy priority is growth, not short-term financial market stability. The Bank of Korea expects low interest rates to ease the debt repayment burden on households and businesses while the government's macroprudential measures slow the growth of private debt. While we agree that accommodative monetary policy can cushion a sharp decline in growth, we do not fully agree that it will stimulate consumption and investment. Weak exports and trade policy uncertainty make it difficult to expect a cyclical recovery in investment and consumption.

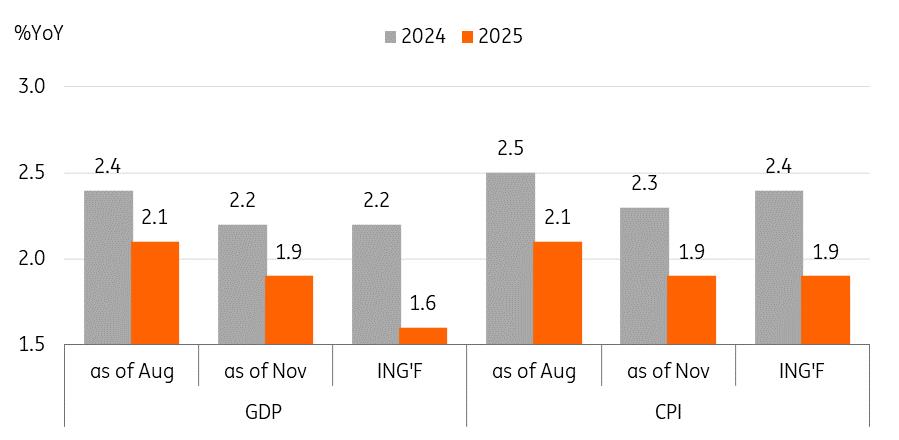

For these reasons, we now expect the BoK to deliver four rate cuts: a 25 bp cut by each quarter in 2025 to a terminal rate of 2.0% but we are keeping our annual GDP forecast of 1.6% (vs 2.2% in 2024). For inflation, we expect it to ease from 2.4% in 2024 to 1.9% in 2025, as a weaker won and sluggish demand-side pressures offset each other. Also, we have changed our KRW forecasts. More rate cuts will probably add more depreciation pressure on the KRW. Widening growth and yield differentials between the US and Korea are a risk factor for KRW-denominated assets. We expect the KRW to trade within a range of KRW1,375-1,475 next year (compared to our previous forecast of KRW1,350-1,400). We expect a weaker KRW in 1H25 with increased volatility. While global dollar movements will be the dominant factor in overall flows, the Korean won is likely to be hit harder than other Asian currencies as the KRW is more sensitive to external shocks given its large trade surplus with the US, high export dependence, and geopolitical sensitivity.

The Bank of Korea lowered its GDP and inflation outlook

Source: Bank of Korea, ING estimates

Author:Min Joo Kang

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment