(MENAFN- ING) Industrial production retreated in May, but Japan's economic outlook remains reasonably optimistic. While Tokyo inflation showed cost-push inflation persisting, tight labour conditions could signal supply-side price pressures

materialising over the coming months

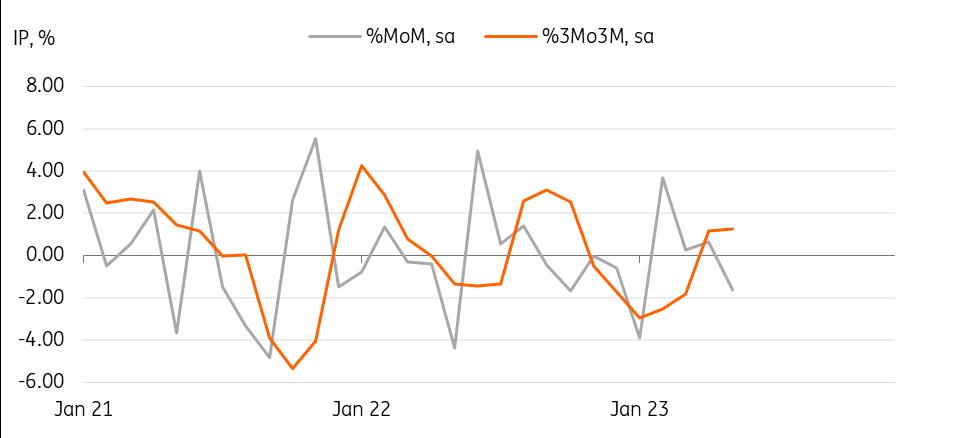

Industrial production came in lower than expected, but we're expecting further rises moving forward Industrial production dropped for the first time in four months Manufacturing output declined -1.6% month-on-month seasonally adjusted, surpassing the market consensus of -1.0% in May – but the sequential quarterly trend rose solidly to 1.3% over three months from the previous quarter's -1.8%. The outlook forecast for manufacturing activity in June rose solidly by 5.6%, and we therefore expect manufacturing output eventually to turn positive in the current quarter. The decline was broadly based, with the most notable drop in vehicles (-8.9%). We believe that the Golden Week holiday effects may have had some negative impact on the overall monthly output.

Sequential trend expands despite the monthly drop in May

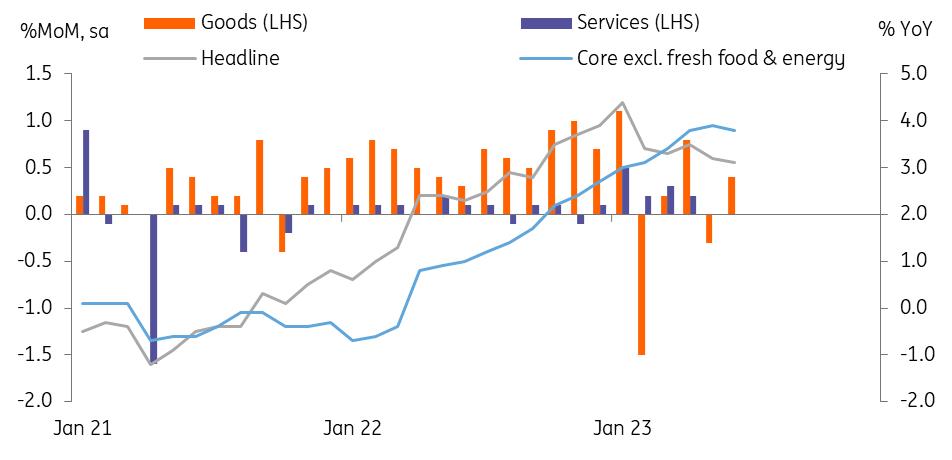

CEIC Tokyo inflation slowed in June Tokyo consumer inflation rose 3.1% year-on-year in June, missing the market consensus of 3.4%. The electricity fee hikes during the month appear to given a smaller boost than expected and spill-over to other service prices has been contained. In a monthly comparison, goods prices rose 0.4% MoM sa but service prices remain unchanged, which shows that Japan is still experiencing more cost-push inflation. However, labour market conditions tightened, with the unemployment rate staying at 2.6% for the second month. As a result, we believe we should be able to see supply-driven inflation in the coming months.

Tokyo inflation suggest cost push inflationary pressures build up

CEIC BoJ watch While industrial production outcome was a bit lower than expected, we believe this is more like a temporary pause and is likely set to rise again. Taking solid retail sales data from yesterday into account, we expect GDP to remain positive in the second quarter. We also foresee cost-push inflation to continue for a while, with the Bank of Japan remaining patient on policy-making and rate hikes.

MENAFN10072023000222011065ID1106575919

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Comments

No comment