(MENAFN- ING) A day before the Bank of England announces its latest decision,

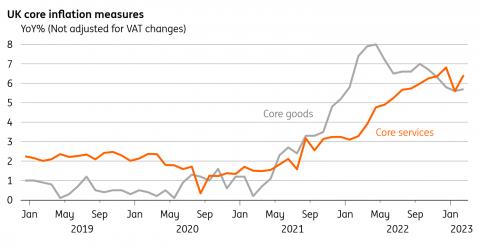

it is faced with an unwelcome resurgence in UK core inflation. Core CPI is back up at 6.2% (from 5.8% in January), and more importantly shows that the surprise dip in services CPI last month was a temporary one.

Policymakers have signalled this is an area they're paying particular attention to, not least because service-sector inflation tends to be more 'persistent' (that is, trends tend to be more long-lasting than for goods) and less volatile. Inflation in hospitality is proving particularly sticky.

The caveat here is that the Bank has indicated it is paying less attention to any one single indicator, and is focused more on a broader definition of“inflation persistence” and price-setting behaviour. And in general, the data has been encouraging over the past month or so. The Bank's own Decision Maker Panel survey of businesses points to less aggressive price and wage rises in the pipeline, and the official wage data finally appears to be gradually easing.

Core services inflation has bounced back after January's dip

Macrobond, ING calculations

Core services inflation excludes air fares, package holidays and education. Core goods excludes food, energy, alcohol and tobacco. Series vary slightly from BoE estimates, partly due to lack of VAT adjustment

We suspect the Bank will want to see more evidence before ending its rate hike cycle entirely, and that's particularly true after these latest inflation numbers. We're still narrowly expecting a 25bp hike on Thursday, and we think the BoE will take a leaf out of the European Central Bank's book and reiterate that it has the tools available if needed to tackle financial stability, thereby allowing monetary policy to focus on inflation-fighting. This was the mantra it adopted last October/November during the mini-budget and LDI pensions fallout in UK markets.

However, assuming the broader inflation data continues to point to an easing in pipeline pressures, then we suspect the committee will be comfortable with pausing by the time of the next meeting in May.

click here to read our full bank of england preview

MENAFN22032023000222011065ID1105834480

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Comments

No comment