403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Czech National Bank Review: The Governor Delivered What He Promised

(MENAFN- ING) CNB confirmed its dovish shift

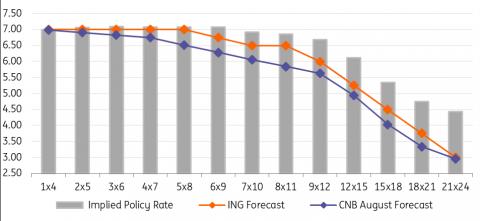

CNB, ING

Rate hike possible only if global risks materialise

Refinitiv, ING

What to expect in rates and FX markets

The CNB left interest rates unchanged today, in line with our expectations . Five members voted in favour of the decision, with two voting for a 100bp rate hike. The details of the vote will be released next week; however, from previous statements it is almost certain that Marek Mora and Tomas Holub voted for the rate hike.

During the press conference, for the first time led by new governor Ales Michl, the CNB's summer forecast was presented. It brought an extension of the monetary policy horizon from 12-18 months to 18-24 months in its baseline scenario as we could only see in May an alternative scenario. With no surprises, inflation moved up in the CNB forecast and is expected to peak in September at 20.4% year-on-year. However, the main shift was in inflation for next year, moving from 4.1% to 9.5% on average. GDP growth was improved from 0.8% to 2.3% this year and downgraded from 3.6% to 1.1% next year. However, under these conditions, the CNB sees the key rate lower than previously forecast, with the peak at the current 7.0% and the first cut implied by the forecast in the fourth quarter of this year. For the koruna, this scenario should imply a depreciation above the 25.00 EUR/CZK level in 4Q and remain around the 25.60 EUR/CZK level throughout the forecast horizon.

In addition to the stability of rates, this time the Board's statement also included a sentence on the CNB's continued intention to 'prevent excessive fluctuations of the koruna exchange rate'. The Governor did not want to comment more on FX interventions during the press conference, but it is clear that the exchange rate has become the main tool of monetary policy.

CNB summer forecastCNB, ING

Rate hike possible only if global risks materialise

Today's CNB meeting confirmed the transformation from hawk to dove and, in our view, showed that the new board is not willing to hike rates now or in the future. Thus, we see no change in our forecast and continue to expect the CNB to no longer raise rates. Although the governor mentioned during the press conference that further rate hikes are not out of the question and will depend on incoming data from the economy, we believe that global developments and pressure on the koruna are key at the moment.

The CNB expects inflation to reach 20% YoY and we believe the pain threshold is high enough to accommodate any upside surprises. Therefore, in our view, only the excessive cost of FX intervention may push the CNB to hike rates again. So the right question is where is the pain threshold of the new board for spent FX reserves. We think it is above 30% of all FX reserves, which is far from current levels (according to our calculation 12% of FX reserves since mid-May).

We can expect pressure on the koruna to increase in the coming days, however, we think sufficient pressure would be sparked by an EM-wide sell-off triggered by global events. Otherwise, we think the CNB can weather the period of record inflation and short koruna speculation in peace and start talking about rate cuts next year, motivated by the weak performance of the economy.

Czech FRA curve expectationsRefinitiv, ING

What to expect in rates and FX markets

Short-term expectations within a year dropped by about 20-30bp in response to the decision and the long end of the curve to a lesser extent, resulting in a strong bull steepening. We expect this trend to continue and therefore continue to like the 2s10s steepener. After the CNB revealed the new cards it wants to play, we see that the risk of a rate hike is lower. At the same time, inflation rising to 20% is becoming a market view. Thus, an outright receiving position at the short end of curve also make sense.

Czech government bonds will get a boost from the ongoing rally in our view, but given the recent buying momentum across the Central and Eastern European region and the all-time record August supply, we see limited space for improvement. Asset spreads of the belly and long end of the curve indicate extremely tight market conditions, which may not allow a significant move lower in yields.

The koruna briefly looked towards 24.550 EUR/CZK just after the decision, likely due to closing short positions as hopes of a near end to the CNB intervention regime faded. However, after the press conference the koruna returned to just below 24.600 and we expect it to remain in this area. Later next week, we will have the first estimate of CNB FX reserves costs for this week, which could reveal how realistic it is that the central bank's new main policy tool becomes too painful.

Author:Frantisek Taborsky

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment