403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Semiconductor Foundry Market Size, Share, Growth, Analysis, 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

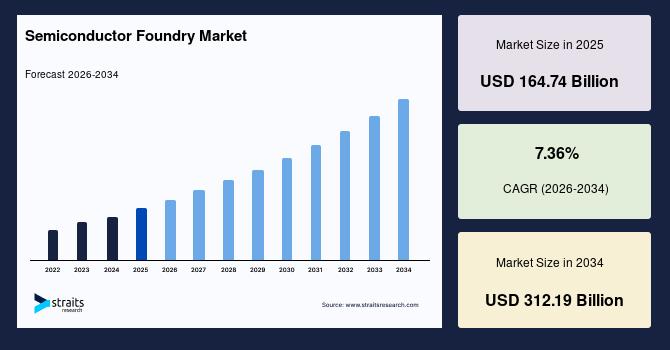

| 2025 Market Valuation | USD 164.74 Billion |

| Estimated 2026 Value | USD 176.87 Billion |

| Projected 2034 Value | USD 312.19 Billion |

| CAGR (2026-2034) | 7.36% |

| Study Period | 2022-2034 |

| Dominant Region | Asia Pacific |

| Fastest Growing Region | North America |

| Key Market Players | TSMC, Samsung Foundry, Intel Foundry Services, GlobalFoundries, UMC (United Microelectronics Corporation) |

Download Free Sample Report to Get Detailed Insights.

Market Driver Rising integration of advanced technologies across sectorsThe global semiconductor foundry market is being propelled by the rising integration of advanced technologies across multiple sectors, from automotive and consumer electronics to cloud computing and artificial intelligence. As industries pursue smarter, faster, and more energy-efficient solutions, the demand for next-generation chips is accelerating.

-

For instance, in June 2025, Chinese EV manufacturer Xpeng introduced its in-house AI chip named Turing, delivering up to 2,200 TOPS to power ADAS and autonomous driving, with plans to integrate it into Volkswagen models in China.

Similarly, in April 2025, Intel Foundry partnered with Synopsys to enable production-ready design flows for its advanced 18A and 18A-P nodes, incorporating innovations such as RibbonFET, PowerVia, and EMIB-T packaging to enhance chip performance for AI and HPC applications.

These developments highlight how foundries are becoming critical enablers of technological transformation, ensuring industries can meet escalating computational and efficiency demands in a rapidly evolving digital ecosystem.

Market Restraint Extremely high capital intensity and long lead times for fab setupThe global semiconductor foundry market faces significant restraints due to its extremely high capital intensity and long lead times for fab setup. Establishing advanced fabrication facilities requires multi-billion-dollar investments in equipment, technology, and infrastructure, creating a major entry barrier for new players.

Moreover, setting up and operationalizing a fab often takes several years, delaying capacity expansion and limiting flexibility in responding to sudden demand surges. These factors slow market scalability, making foundries heavily reliant on long-term planning and strategic partnerships to mitigate risks.

Market Opportunity Expansion of 3nm and sub-3nm nodes for next-gen computing and AI workloadsThe global semiconductor foundry market is seeing significant opportunities as the expansion of 3nm and sub-3nm nodes accelerates next-generation computing and AI workloads. As demand for higher-performance, energy-efficient chips grows across data centers, AI infrastructure, and high-performance computing, foundries are investing heavily to scale advanced process technologies.

-

For instance, in March 2025, Intel announced it would shift high-volume production of its 3nm“Intel 3” node to its Fab 34 facility in Ireland, offering an estimated 18% improvement in performance-per-watt over Intel 4 and improving accessibility for foundry customers.

Meanwhile, in May 2025, TSMC revealed plans to invest USD 38 to 42 billion in its 2nm roadmap, including fabs in Kaohsiung and Hsinchu, targeting N2 and post-2nm nodes for future launches.

These developments highlight the market's strong growth potential as cutting-edge nodes enable more powerful, efficient, and scalable computing solutions.

Regional AnalysisNorth America dominates the global semiconductor foundry market due to its advanced technological ecosystem, strong R&D capabilities, and robust presence of leading foundries and fabless companies. The region benefits from extensive investments in high-performance computing, AI, and automotive electronics, driving demand for advanced nodes and specialized packaging technologies. Moreover, government initiatives supporting domestic chip production, along with strong IP protection and a mature supply chain, reinforce North America's leadership in semiconductor manufacturing and innovation, making it a key hub for next-generation semiconductor solutions.

-

The United States semiconductor foundry market is highly developed, driven by both domestic demand and global outsourcing. Companies such as Global Foundries, Intel Foundry Services, and Texas Instruments play a critical role, producing advanced nodes and custom chips for AI, HPC, automotive, and consumer electronics. Investments in 3nm and sub-3nm technologies, along with advanced packaging solutions, position the US as a strategic hub, enabling rapid innovation.

Canada's semiconductor foundry market is growing steadily, supported by advanced research institutions and technology clusters in Ontario and Quebec. Companies like Teledyne DALSA and D-Wave leverage local expertise to manufacture specialized chips for imaging, quantum computing, and AI applications. Strategic partnerships with U.S. and European firms help Canadian foundries adopt advanced nodes and packaging techniques.

Asia-Pacific is witnessing significant growth in the semiconductor foundry market, fueled by rising demand for consumer electronics, AI, automotive, and telecommunications applications. The region benefits from government incentives, large-scale investments in fabs, and a strong manufacturing ecosystem. Moreover, countries across APAC are rapidly expanding advanced process nodes, supporting high-performance computing, AI workloads, and next-generation mobile devices. The combination of cost-efficient manufacturing, skilled workforce, and proximity to major electronics markets makes Asia-Pacific a crucial driver of global semiconductor foundry growth in 2025 and beyond.

-

China's semiconductor foundry market is expanding rapidly, driven by domestic demand for AI, 5G, and automotive electronics. Companies like SMIC and Hua Hong Semiconductor are investing heavily in advanced nodes, including 7nm–5nm processes, while also adopting FinFET and advanced packaging technologies. Strategic government support, along with partnerships with global semiconductor firms, helps China strengthen its local manufacturing capabilities.

India's market is growing steadily, supported by government initiatives such as the India Semiconductor Mission and investments in advanced manufacturing clusters. Companies like IGSS Ventures, Tessolve, and Sankalp Semiconductor are expanding capabilities in custom chip design, testing, and packaging. Collaborations with global foundries help India adopt advanced nodes and FinFET technology for consumer electronics, automotive, and industrial applications.

The global market is segmented into technology node, foundry type, technology, application, and end-user industry.

Technology Node InsightsThe 7nm–9nm technology node remains dominant in the semiconductor foundry market due to its balance of performance, power efficiency, and cost-effectiveness. It supports high-performance computing, AI accelerators, and advanced mobile processors while enabling mass production at a manageable cost. Many leading foundries continue to optimize 7nm–9nm processes, meeting the growing demand from consumer electronics and automotive sectors, where high-speed, energy-efficient chips are essential for modern applications like smartphones, laptops, and ADAS-enabled vehicles.

Foundry Type InsightsPure-play foundries, which focus solely on manufacturing without in-house design capabilities, dominate the market by offering scalable, flexible production for a wide range of customers. Their specialization allows them to adopt advanced process nodes quickly, provide cost-efficient solutions, and serve multiple industries. Companies like TSMC and GlobalFoundries leverage pure-play models to maintain high-volume production, cater to AI, HPC, and consumer electronics demand, and enable fabless semiconductor companies to bring innovative products to market efficiently.

Technology InsightsFinFET technology dominates due to its superior control over leakage current, higher transistor density, and better power efficiency compared with planar CMOS. Widely adopted for high-performance processors, mobile SoCs, and AI accelerators, FinFET allows foundries to deliver chips capable of handling demanding workloads. Its prevalence across leading process nodes (7nm–5nm) ensures reliability, scalability, and energy efficiency, making it the preferred choice for advanced consumer electronics, automotive electronics, and data center applications worldwide.

Application InsightsConsumer electronics lead the application segment due to the continuous demand for high-performance, energy-efficient chips in smartphones, laptops, tablets, and wearable devices. The proliferation of AI-enabled features, 5G connectivity, and high-resolution displays requires advanced semiconductors, driving foundries to prioritize this sector. Dominant process nodes like 7nm–9nm and FinFET technology are extensively used to meet performance and power-efficiency requirements, ensuring devices deliver faster processing, longer battery life, and enhanced user experiences.

Company Market ShareThe market is highly competitive, with leading players focusing on expanding advanced process nodes, including 3nm and sub-3nm technologies, to meet rising demand from AI, HPC, and automotive applications. Companies are investing heavily in advanced packaging, FinFET, and GAA/Nanosheet technologies to enhance chip performance and energy efficiency. Moreover, efforts are directed toward scaling production capacity, optimizing design-to-manufacturing workflows, and supporting specialized applications like 5G, consumer electronics, and data centers, ensuring market leadership through innovation.

TSMCTSMC (Taiwan Semiconductor Manufacturing Company) was established in 1987 in Hsinchu, Taiwan, pioneering the pure-play foundry model. As the world's largest contract semiconductor manufacturer, it specializes in producing advanced process nodes, including 3nm and sub-3nm technologies, for high-performance computing, AI, and mobile applications. TSMC's continuous investment in FinFET, advanced packaging, and next-generation nodes positions it as a key enabler of global semiconductor innovation.

List of Key and Emerging Players in Semiconductor Foundry Market-

TSMC

Samsung Foundry

Intel Foundry Services

GlobalFoundries

UMC (United Microelectronics Corporation)

SMIC (Semiconductor Manufacturing International Corporation)

Powerchip Semiconductor Manufacturing Corp (PSMC)

Vanguard International Semiconductor Corporation

Tower Semiconductor

DB HiTek

Hua Hong Semiconductor

X-FAB Silicon Foundries

VIS

HHGrace

Dongbu HiTek

MagnaChip Semiconductor

Silterra Malaysia

Fujitsu Semiconductor

Texas Instruments

Infineon Technologies

-

June 2025 – GlobalFoundries unveiled a $16 billion investment to expand its semiconductor manufacturing and advanced packaging operations at its facilities in New York and Vermont. The move addresses surging demand from artificial intelligence, which is driving the need for next-generation semiconductors optimized for power efficiency and high-bandwidth performance in data centers, communications infrastructure, and AI-powered devices.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 164.74 Billion |

| Market Size in 2026 | USD 176.87 Billion |

| Market Size in 2034 | USD 312.19 Billion |

| CAGR | 7.36% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Technology Node, By Foundry Type, By Technology, By Application |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Semiconductor Foundry Market Segments By Technology Node-

<5nm

5nm – 6nm

7nm – 9nm

10nm – 13nm

14nm – 19nm

20nm – 27nm

28nm – 44nm

45nm – 64nm

65nm – 89nm

≥ 90nm

-

Pure-Play Foundries

Integrated Device Manufacturers (IDMs) with Foundry Services

-

CMOS

FinFET

FDSOI (Fully Depleted Silicon on Insulator)

Gate-All-Around (GAA) / Nanosheet

Silicon Photonics

MEMS (Micro-Electro-Mechanical Systems)

Compound Semiconductors (GaN, GaAs, SiC)

-

Consumer Electronics

Automotive

Industrial

Telecommunication

Data Centres & HPC

Medical Devices

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment