403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Vital Signs Monitoring Market Size, Global Trends, Demand, Forecast To 2033

| Market Metric | Details & Data (2025-2034) |

|---|---|

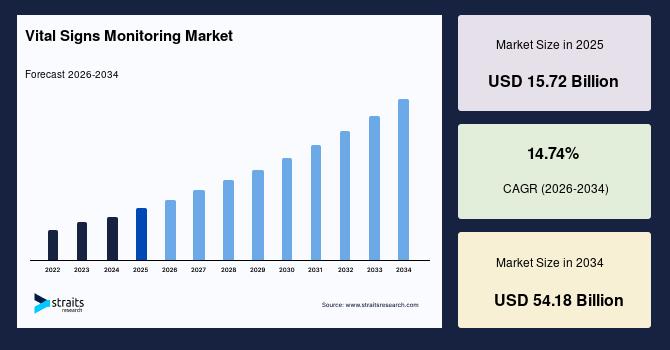

| 2025 Market Valuation | USD 15.72 Billion |

| Estimated 2026 Value | USD 18.04 Billion |

| Projected 2034 Value | USD 54.18 Billion |

| CAGR (2026-2034) | 14.74% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Europe |

| Key Market Players | Koninklijke Philips N.V., Medtronic Plc, Nihon Kohden Corporation, GE Healthcare, OMRON Healthcare, Inc. |

Download Free Sample Report to Get Detailed Insights.

Vital Signs Monitoring Market Growth Factors Increasing Usage of Vital Signs Monitoring DevicesThe vital signs monitoring market encompasses products and services that help monitor general body functioning by continuously measuring various parameters. In 2023, approximately 65% of hospitals worldwide were estimated to use some electronic vital signs monitoring system. By 2024, this percentage is projected to increase to around 70-75%. These devices are powered by modern technologies that make these devices compact, portable, and a point of care. Increased availability of these products in the market has raised awareness regarding the convenience and cost-effectiveness offered. This has positively influenced the market growth and is expected to drive the market.

Furthermore, there has been a recent trend in shifting preferences among patients, who are increasingly opting for treatment at home instead of prolonged hospital stays. This is due to significant cost advantage and reduced hospital expenditure, making treatment more affordable. This shift has opened new opportunities for home monitoring devices that facilitate proactive monitoring of patients.

Innovation in ProductsNew and improved vital sign monitoring devices are constantly being developed, enhancing their usability and functionality. In 2023, about 25% of vital signs monitoring systems incorporated AI for data analysis and predictive diagnostics. This is expected to increase to 30-35% by 2024. Innovation in the healthcare sector is booming, especially regarding creating tools for monitoring vital signs. These developments are improving the gadgets' usability and functionality, making them essential parts of medical care.

Furthermore, the wireless connectivity of modern technologies makes it possible to monitor patients' vital signs remotely. This is especially advantageous for home healthcare services and telemedicine. The emergence of wearable technology has wholly changed patient monitoring by enabling non-intrusive, continuous, real-time data collecting. Innovation in vital sign monitoring devices goes beyond feature additions; it also involves raising patient outcomes, improving treatment quality, and streamlining and improving accessibility to healthcare.

Market Restraining Factors Unresponsiveness of Devices under Certain CircumstancesA significant barrier to the market for vital sign monitoring. Numerous things, such as the devices' technological shortcomings, incorrect use, or highly severe patient circumstances that the devices need to be designed to handle, might cause this problem. Inaccurate readings or a failure to offer crucial monitoring crucial for patient care can result from such unresponsiveness.

-

For example, some devices cannot perform as intended when individuals have specific skin problems or insufficient perfusion. Furthermore, the devices' functioning may be impacted by electromagnetic interference in the surrounding area. The unresponsiveness of devices continues to be a barrier that may affect the accuracy of vital sign monitoring and, as a result, patient outcomes unless these advancements are broadly adopted.

New applications for vital sign monitoring devices are being made possible by the quick development of wearable health technology. The field of vital sign monitoring has seen a significant transformation thanks to the advancement of wearable health technology. The number of wearable vital signs monitoring devices shipped globally in 2023 was estimated at 250 million units. Projections for 2024 suggest this could reach 300 million units. These developments mark a paradigm shift in healthcare provision and the management of individual well-being; they go beyond simple miniaturization or cosmetic enhancements.

Over time, wearable health devices (WHDs) have evolved from basic fitness trackers to complex systems tracking vital signs, including blood pressure, heart rate, and blood sugar levels. Integrating sensors, wireless connection, and processing capacity has facilitated ongoing, instantaneous health monitoring in routine environments. For example, heart rate and oxygen saturation can be tracked wirelessly without using bulky wires or attachments thanks to Remote Photoplethysmography (rPPG) technology. Due to it's frequently integrated into smartphones and smartwatches, a larger audience can utilize this technology. Wearable health devices will experience more integration with machine learning and artificial intelligence in the future, improving the precision and prognostication of health assessments.

Regional Insights North America : Dominant Region Witha Cagr of 5.4%North America is the most significant market shareholder and is estimated to grow at a CAGR of 5.4% over the forecast period. North America, notably the United States, has dominated the Vital Signs Monitoring market. In 2023, roughly 70% of hospitals in the United States had deployed advanced vital signs monitoring systems, which is predicted to rise to 75% by 2024. The region's leadership is fueled by high healthcare spending, solid technical infrastructure, and supporting government policies. In 2023, approximately 15 million patients in North America were using remote vital sign monitoring devices, with forecasts indicating that this figure could rise to 18 million by 2024.

-

According to the United States Centers for Disease Control and Prevention, 65% of persons over 65 will use a digital health monitoring gadget by 2023. In 2023, Canada and the United States accounted for nearly 40% of global wearable vital signs monitoring device shipments, a share that is predicted to stay constant through 2024. Large market participants and a strong emphasis on healthcare technology R&D support the region's dominance.

Europe is estimated to grow at a CAGR of 6% over the forecast period. Europe is the sub-dominant area in the Vital Signs Monitoring industry, with nations like Germany, the United Kingdom, and France driving adoption. In 2023, around 60% of European hospitals had integrated vital sign monitoring systems, with the percentage expected to rise to 65% by 2024. According to the European Commission, over 25% of EU citizens used linked health devices to monitor vital signs in 2023, and this figure is predicted to climb to 30% by 2024.

Furthermore, the region's market is strengthened by an aging population and a greater emphasis on preventative healthcare. The European home healthcare market saw approximately 8 million patients use vital signs monitoring devices in 2023, with forecasts indicating that this figure will rise to 10 million by 2024. The National Health Service in the United Kingdom estimated that 55% of its telemedicine consultations included some remote vital sign monitoring in 2023, with this figure predicted to rise to 60% by 2024. While European adoption rates are slightly lower than in North America, the region's robust healthcare systems and growing government support for digital health projects drive market growth.

Product InsightsThe market is further segmented into blood pressure monitors, pulse oximeters, temperature monitoring devices, and glucose monitoring devices. Pulse oximeters are predicted to increase in the vital signs monitoring devices market, with a CAGR of over 8%. The rising frequency of cardiovascular disorders, increased desire for minimally invasive operations, and newer technology breakthroughs are all driving the growth of the pulse oximeter market. Pulse oximeters are electronic devices that detect oxygen saturation in red blood cells, making them an essential vital sign monitoring tool.

Blood pressure monitoring devices are divided into four categories: aneroid BP monitors, automated BP monitors, digital BP instruments, and ambulatory BP monitors. Blood pressure monitors detect and monitor hypertension and other critical conditions in various medical settings, making them a crucial component of vital sign monitoring. While not increasing as quickly as pulse oximeters, blood pressure monitors are the most popular product in the vital signs monitoring device market.

End-Users InsightsThe market is further segmented into Hospitals, Physician Clinics, Home Healthcare Settings, and Ambulatory Centers. Hospitals are the top end-user category in the Vital Signs Monitoring market. This is explained by their patient base's size and improved ability to finance these gadgets. Hospitals need various monitoring equipment because they use vital sign monitoring devices in many contexts, such as emergency rooms, regular wards, and critical care units. Hospitals need to use a wide variety of vital sign monitors to track multiple physiological indicators. This covers specialist equipment for sophisticated monitoring requirements in addition to standard monitors.

The Home Healthcare segment is anticipated to grow at the quickest rate (CAGR) because of the aging population, the rise in demand for user-friendly devices, technological advancements, remote patient monitoring, and the management of chronic diseases. These establishments use vital sign monitors for first evaluations and routine examinations, which increases their market share. These outpatient clinics also use essential sign monitors for various operations and patient monitoring requirements.

List of Key and Emerging Players in Vital Signs Monitoring Market-

Koninklijke Philips N.V.

Medtronic Plc

Nihon Kohden Corporation

GE Healthcare

OMRON Healthcare, Inc.

Terumo Corporation

Nonin Medical Inc

SunTech Medical Inc

Masimo

Contec Medical Systems Co Ltd

Baxter International Inc

A&D Company

ICU Medical

OSI Systems

Others

-

November 2023 - Low-Noise AFE Sensor for Vital Sign Monitoring was released by Ams Osram. Ams Osram's AS7058 is a prime example of the sophisticated integration found in many contemporary health monitoring systems.

July 2023- Australian researchers created a technology that combines lidar and photonic radar to allow for remote, extremely accurate vital sign monitoring. This hybrid arrangement, which takes advantage of each approach's advantages, might serve as a basis for an affordable, high-resolution noncontact vital-sign detection system, according to a news release that accompanied the research.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.72 Billion |

| Market Size in 2026 | USD 18.04 Billion |

| Market Size in 2034 | USD 54.18 Billion |

| CAGR | 14.74% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Product, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Vital Signs Monitoring Market Segments By Product-

Blood Pressure Monitors

-

Devices

-

Aneroid Blood Pressure Monitors

Digital Blood Pressure Monitor

Ambulatory Blood Pressure Monitors

-

Devices

-

Table-top/Bedside Pulse Oximeters

Fingertip Pulse Oximeter

Hand-held Pulse Oximeters

Wrist-worn Pulse Oximeters

Pediatric Pulse Oximeters

-

Devices

-

Mercury Filled Thermometers

Digital Thermometers

Infrared Thermometers

Liquid Crystal Thermometer

-

Hospitals & Clinics

Ambulatory Surgery Centers

Home Care Settings

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment