403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Zero Trust Security Market Size, Share & Trends Report By 2033

| Market Metric | Details & Data (2025-2034) |

|---|---|

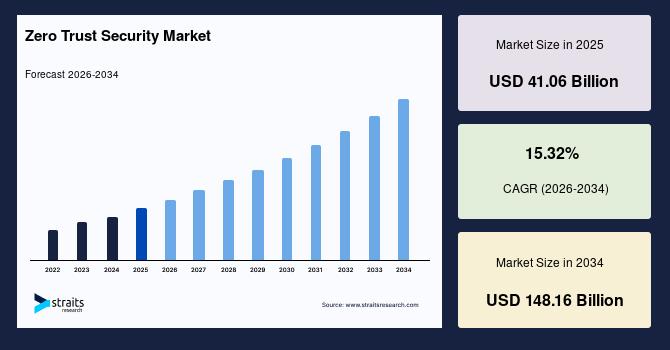

| 2025 Market Valuation | USD 41.06 Billion |

| Estimated 2026 Value | USD 47.35 Billion |

| Projected 2034 Value | USD 148.16 Billion |

| CAGR (2026-2034) | 15.32% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Key Market Players | Cisco, Akamai, Palo Alto Networks, Symantec, OKTa |

Download Free Sample Report to Get Detailed Insights.

Zero Trust Security Market Growth Drivers Increasing Cyber ThreatsThe increasing number of interconnected devices, data, and apps enhances the probability of cyber threats. Check Point Research (CPR) reported a 38% increase in worldwide cyberattacks in 2022 compared to the previous year, 2021. According to Security Magazine, a significant number of over 2,200 attacks happen daily, resulting in a concerning frequency of almost one cyberattack every 39 seconds.

Similarly, as per a survey by Cybersecurity Ventures, the estimated global cost of cybercrime is predicted to rise to USD 10.5 trillion per year by 2025, a substantial increase from USD 3 trillion in 2015. Due to the rising prevalence of cyber threats such as ransomware, data breaches, and insider threats, traditional security methods that focus on protecting the perimeter are no longer enough. Moreover, Zero Trust Security provides a proactive and adaptable approach to cybersecurity, making it more effective in countering contemporary threats. Hence, the rising number of cyber threats on a global scale is projected to propel the growth of the global zero trust security market.

High Adoption of Zero Trust SecurityZero Trust Security is particularly relevant in the current landscape, characterized by the emergence of remote work and cloud-based services, which has weakened the traditional network boundary and diminished the efficacy of existing security frameworks. This has resulted in a global rise in the implementation of zero trust security solutions, which has propelled the expansion of the market.

Okta's most recent annual report, titled "The State of Zero Trust Security," published in October 2023, revealed that nearly all organizations (96%) have either implemented or are preparing to implement a zero-trust security initiative within the next 18 months. Moreover, 61% of organizations have made significant progress in their zero-trust journey in 2023, compared to only about 25% in 2021. Although facing macroeconomic challenges, funds for zero-trust security have been consistently increasing. According to Okta's survey, 80% of the participants stated that their organization's zero trust budgets had grown in the previous year.

Market Restraint Complexity of ImplementationThe complexity involved in implementing zero trust security might provide significant challenges for organizations considering its adoption. Zero Trust Security requires a significant departure from conventional security models relying on perimeters. Organizations must reassess and revamp their entire security framework to embrace Zero Trust concepts. This entails reassessing access rules, network segmentation, authentication systems, and data protection strategies.

Numerous firms own complex and diverse IT infrastructures consisting of outdated systems, cloud services, on-site infrastructure, and other organizations' applications. Integrating Zero Trust Security solutions with these existing systems can be difficult. Due to the growing utilization of cloud services and hybrid IT architectures, enterprises frequently operate on several cloud platforms and environments. Moreover, the implementation of Zero Trust Security in multi-cloud environments introduces an additional level of intricacy, as it is the responsibility of organizations to guarantee uniformity in security policies and controls throughout all cloud instances.

Market Opportunity Launch of Novel Zero Trust Security SolutionsMajor stakeholders in the market are introducing novel and enhanced zero-trust security solutions to enhance their market share. For instance, in February 2024, iboss, a prominent provider of cloud-based cybersecurity, introduced the ChatGPT Risk Module as an innovative component of its Zero Trust Security Service Edge (SSE) solution. This advanced module is specifically engineered to oversee and safeguard user interactions using ChatGPT, a prominent artificial intelligence technology, guaranteeing exceptional data security and adherence to regulations in ever-changing digital environments.

Additionally, in November 2023, Palo Alto Networks recently introduced Strata Cloud Manager, a Zero Trust management and operations solution that utilizes AI. This offering is accompanied by increased security features and five new next-generation firewalls. Palo Alto Networks provides cloud-based security services that safeguard against emerging threats for over 60,000 customers. The Advanced WildFire system incorporates innovative detection capabilities and utilizes AI-powered Advanced Threat Prevention to bolster security measures by promptly identifying and mitigating potential threats. Such launches are anticipated to create opportunities for market expansion.

Regional InsightsNorth America is the most significant global zero trust security market shareholder and is expected to expand substantially during the forecast period. The adoption of zero-trust security is strong in North America due to the region's advanced technological infrastructure and the abundance of cyber threats. The North American zero trust security market is also vast and firmly established, fueled by the region's substantial vulnerability to heightened cyber threats and attacks. As per data from the Identity Theft Resource Center (ITRC), the United States had an increase in the number of data breaches, with the total rising from 1,506 breaches in 2017 to 1,826 breaches in 2021. The rise in cybersecurity threats is expected to drive the market expansion in North America. Moreover, firms in all sectors are allocating resources towards implementing zero trust solutions to strengthen their security measures against advancing cyber threats, as seen by 73% of organizations having a well-outlined strategy.

Furthermore, the region exhibits a robust and comprehensive framework of laws and regulations and an increased consciousness of data security and privacy concerns. This has led to a rise in the demand for efficient security devices. The United States Cybersecurity and Infrastructure Security Agency (CISA) has released version 2 of its Zero Trust Maturity Model (ZTMM), which integrates suggestions from public feedback on the initial version. This updated model introduces a new phase that simplifies the process for organizations to adopt a zero-trust architecture. Moreover, prominent industry participants are launching innovative zero trust security solutions. For instance, in April 2023, Tailscale Inc., a Canadian company that provides corporate virtual private networks, introduced a zero-trust networking solution for enterprise customers. This solution enables users to authenticate each connection and encrypt all communication from end to end. Therefore, all of these factors contribute to the expansion of the regional market.

Asia-Pacific Market TrendsThe Asia-Pacific region is experiencing a rapid and significant digital transformation process. As companies increase their online presence, the demand for comprehensive security solutions grows crucial. Countries such as India, China, and Japan are increasingly adopting zero trust security measures due to the rising cyber dangers they face. Moreover, the prominent participants in the industry are actively undertaking efforts to increase the implementation of zero trust security. For instance, in June 2023, BeyondID, a prominent provider of managed identity services for cybersecurity and cloud services, announced its assistance in facilitating enterprises' adoption of the Okta Identity Engine (OIE) to support their zero trust strategy. BeyondID's services provide customers with a well-defined plan for improvement, including implementing robust security measures such as passwordless protection and Okta FastPass. These factors enhance the expansion of the regional market.

Market Segmentation Type InsightsThe global zero trust security market is divided into network security, data security, endpoint security, security analytics, and others. The endpoint security segment is estimated to hold the most significant market share. Endpoint attacks account for 50% of all organizational data breaches. The 2018 Data Breach Investigation Report issued by Verizon Wireless revealed that cybercriminals specifically target weak endpoint security to carry out their cyber-attacks. Approximately 14.5% of over 2,200 data breaches in 65 countries were mostly caused by remote assaults targeting point-of-sale (POS) terminals and controllers. Ransomware, accounting for 56% of all malware, can also infiltrate web applications when the device lacks adequate endpoint security. The increasing use of BYOD in organizations, where employees have multiple access points to important enterprise data, has led to a significant need for zero-trust security solutions.

Authentication InsightsThe global zero trust security market is bifurcated into single factor authentication and multi-factor authentication. The multi-factor authentication segment dominates the global market. Multi-factor authentication (MFA) is a security protocol that requires users to present various forms of identity to obtain access to a system, application, or service. It provides an additional level of security that goes beyond relying solely on a login and password combination, which can be readily breached. By incorporating zero trust concepts into multi-factor authentication, companies can greatly improve their security stance by decreasing the probability of unwanted access and mitigating the consequences of potential breaches.

Verticals InsightsThe global zero trust security market is segmented into BFSI, IT and telecom, government and defense, healthcare, energy and power, and others. The IT and telecom segment owns the highest market share. Zero Trust security principles are crucial for bolstering cybersecurity in the IT and telecom industries, where safeguarding sensitive data and vital infrastructure is paramount. Companies can enhance the security of their networks, avert data breaches, and uphold consumer trust by adopting zero-trust practices. The Zero Trust approach advocates for ongoing surveillance of network traffic, user conduct, and device operations to promptly identify abnormalities and potential security risks. Through continuous analysis of network traffic and user behavior patterns, IT and telecom enterprises may promptly detect and address security incidents, thereby reducing potential harm.

List of Key and Emerging Players in Zero Trust Security Market-

Cisco

Akamai

Palo Alto Networks

Symantec

OKTa

Forcepoint

Centrify

Cyxtera Technologies

Illumio

Google

Microsoft

-

August 2025: Palo Alto Networks has agreed to acquire identity security powerhouse CyberArk in a deal valued at $25 billion. This acquisition is a significant move to expand Palo Alto Networks' platform strategy by formally entering the identity security space, which is a key component of a Zero Trust architecture.

March 2025: The Cloud Security Alliance (CSA) announced that its Certificate of Competence in Zero Trust (CCZT) has been recognized for excellence. This highlights the growing need for specialized skills and knowledge in Zero Trust as a core component of cybersecurity strategy.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 41.06 Billion |

| Market Size in 2026 | USD 47.35 Billion |

| Market Size in 2034 | USD 148.16 Billion |

| CAGR | 15.32% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Type, By Authentication, By Verticals |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Zero Trust Security Market Segments By Type-

Network Security

Data Security

Endpoint Security

Security Analytics

Others

-

Single Factor Authentication

Multi-Factor Authentication

-

BFSI

IT and Telecom

Government and Defense

Healthcare

Energy and Power

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment