403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Large Volume Parenteral (LVP) Market Size, Share, Global Trends And Regional Analysis By 2033

| Market Metric | Details & Data (2025-2034) |

|---|---|

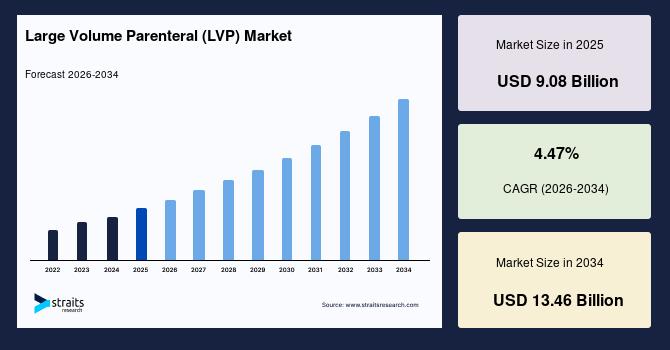

| 2025 Market Valuation | USD 9.08 Billion |

| Estimated 2026 Value | USD 9.49 Billion |

| Projected 2034 Value | USD 13.46 Billion |

| CAGR (2026-2034) | 4.47% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Baxter International Inc., Fresenius Kabi, Braun Melsungen AG, Pfizer Inc., ICU Medical Inc. |

Download Free Sample Report to Get Detailed Insights.

Large Volume Parenteral (lvp) Market Driver Rising Prevalence of Chronic DiseasesChronic diseases such as diabetes, cancer, and cardiovascular disorders are on the rise globally, necessitating long-term and often intravenous treatments. LVPs play a crucial role in managing these conditions by injecting essential fluids, electrolytes, and medications into the bloodstream. The increasing burden of chronic illnesses is thus a significant driver for the LVP market, as healthcare providers seek reliable and efficient drug delivery systems to manage patient care.

-

According to the World Health Organisation, non-communicable diseases account for approximately 74% of all deaths worldwide, highlighting the critical need for effective treatment modalities like LVPs.

Furthermore, the ageing global population contributes to the rising demand for LVPs, as elderly individuals are more susceptible to chronic conditions requiring intravenous therapies. The integration of smart technologies in LVP delivery systems also supports the management of chronic diseases by enabling precise dosing and monitoring, thereby improving patient outcomes.

Market Restraining Factors Stringent Regulatory RequirementsThe LVP industry is subject to rigorous regulatory standards to ensure patient safety and product efficacy. Manufacturers must comply with stringent drug formulation, packaging, and sterility guidelines. These regulations often require substantial investment in quality control systems and can lead to prolonged approval timelines for new products. Additionally, any lapses in compliance can result in product recalls, legal penalties, and damage to brand reputation. Such regulatory challenges can be particularly burdensome for small and medium-sized enterprises, potentially limiting innovation and market entry. For example, in January 2024, Fresenius Kabi received a Class I rating from the FDA for a recall of the Ivenix medication delivery technology due to issues with the large-volume pump component. This incident underscores the critical importance of adhering to regulatory standards and the potential consequences of non-compliance.

Market Opportunity Expansion in Emerging MarketsEmerging economies present significant growth opportunities for the LVP market due to increasing healthcare expenditures, improving infrastructure, and a growing patient population. Governments in countries like India and China are investing heavily in healthcare reforms and hospital expansions, creating a conducive environment for LVP adoption. Moreover, the rising awareness about the benefits of early and effective treatment is leading to higher demand for LVPs. Companies that can navigate these markets' regulatory landscapes and establish strong distribution networks are poised to capitalise on these opportunities.

-

For example, in May 2024, Bristol Myers Squibb (BMS) launched the ASPIRE strategy to increase the affordability and availability of BMS medicines in low- and middle-income countries (LMICs), aiming to reach more than 200,000 patients by 2033.

The development of environmentally friendly packaging materials and the integration of advanced technologies in LVP delivery systems further enhance the appeal of these products in emerging markets, aligning with global sustainability goals and improving patient care.

Regional InsightsNorth America continues to lead the global LVP market, with the United States at the forefront. This dominance is attributed to advanced healthcare infrastructure, substantial healthcare expenditure, and the presence of major pharmaceutical companies. The region's high prevalence of chronic diseases, such as diabetes and cancer, necessitates the extensive use of LVPs for effective treatment. In 2025, the U.S. Food and Drug Administration (FDA) streamlined its regulatory process for injectable manufacturing facilities through the Emerging Technology Program (ETP), encouraging the adoption of advanced production lines and sterile packaging. Moreover, companies like Baxter International and Pfizer are expanding their LVP production capacities.

-

The U.S. remains the largest market for LVPs globally, driven by a well-developed healthcare system, advanced biopharmaceutical manufacturing capabilities, and a high burden of chronic diseases like cancer, diabetes, and renal disorders. The FDA's Emerging Technology Program (ETP) has significantly reduced regulatory bottlenecks for sterile injectable facilities, encouraging companies to invest in cutting-edge production technologies. Furthermore, partnerships between hospitals and drug manufacturers promote the use of customised IV bags for patient-specific therapies, a trend gaining traction in large hospital networks.

Canada's LVP market is steadily expanding, underpinned by its ageing population, high incidence of chronic diseases, and increasing volumes of inpatient care. Leading global firms such as Fresenius Kabi and B. Braun are strengthening their distribution networks in Canada through partnerships with provincial health systems, enabling real-time supply of sterile, ready-to-administer solutions. These efforts are expected to significantly improve clinical outcomes and streamline intravenous therapy workflows across public hospitals.

The Asia-Pacific region is experiencing rapid growth in the market for LVP, driven by increasing healthcare expenditure, rising awareness about advanced medical treatments, and the expansion of healthcare infrastructure. Countries like China, India, and Japan are at the forefront of this growth. The large patient population and the rising incidence of chronic diseases create substantial demand for LVPs. Government initiatives like India's Ayushman Bharat scheme aim to provide affordable healthcare, thereby increasing the accessibility and utilisation of LVPs. Additionally, the growth of medical tourism in the region contributes to market expansion.

-

China is the fastest-growing LVP market globally, thanks to expansive healthcare reforms, rapid hospital network development, and a large ageing population. The“Healthy China 2030” agenda emphasises access to injectable therapies in urban and rural settings. The country's rising cancer and diabetes burden is fueling demand for LVP-based chemotherapy support and parenteral nutrition. Moreover, digital transformation in hospital supply chains enables better tracking, allocation, and usage of IV fluids across China's expanding healthcare infrastructure.

India is rapidly emerging as a global hub for LVP production, leveraging low manufacturing costs and rising domestic demand. The extension of the Production-Linked Incentive (PLI) Scheme for Pharmaceuticals provides fiscal benefits to local firms investing in sterile injectable infrastructure. India's increasing hospitalisation rates, growing medical tourism sector, and emphasis on emergency preparedness have significantly boosted the need for affordable, high-volume intravenous therapies. Additionally, government-led procurement programs for public hospitals are pushing for ready-to-use LVP solutions to improve treatment efficiency and reduce infection risks.

Europe holds a significant share in the global LVP industry, with countries like Germany, France, and the United Kingdom leading. The region's well-established healthcare systems, stringent regulatory frameworks, and high adoption of advanced medical technologies support market growth. The increasing burden of chronic diseases and the ageing population drive the demand for LVPs. European governments' focus on improving healthcare quality, patient safety, and investments in healthcare infrastructure further stimulates market development. Collaborations between the public and private sectors in research and innovation also play a crucial role in advancing the LVP market in Europe.

-

Germany, a leader in Europe's biopharmaceutical industry, boasts a mature market for LVP supported by high healthcare spending and a robust manufacturing ecosystem. The Pharma 2030 strategy, backed by the federal government, incentivises domestic production to reduce reliance on imports and improve supply chain resilience. The rising prevalence of chronic conditions such as heart disease and kidney failure has amplified demand for parenteral therapies in both hospitals and home care. Germany's strong regulatory environment and emphasis on quality assurance continue to attract global pharmaceutical investments in the LVP segment.

France is witnessing robust growth in its LVP industry, driven by national healthcare modernisation programs and increasing surgical admissions. Under the 2024–2027 Health Innovation Plan, the French government provides substantial subsidies to pharmaceutical companies investing in sterile injectables. The country's focus on enhancing post-operative care, cancer management, and nutritional support drives demand for high-quality parenteral solutions. Additionally, integrating digital infusion monitoring systems in public hospitals is expected to enhance patient safety and optimise LVP usage.

Soft Bag LVPs have emerged as the dominant type in the market due to their numerous advantages over traditional glass or plastic bottles. These include superior flexibility, a reduced risk of contamination, and a more environmentally sustainable footprint. Their collapsible design eliminates the need for air exchange, thus maintaining sterility and preventing microbial ingress. The lightweight nature of soft bags also significantly lowers transportation costs and requires less storage space. Additionally, their compatibility with automated aseptic filling lines improves production scalability and operational efficiency. With hospitals increasingly prioritising single-use systems to curb hospital-acquired infections, soft bags are the preferred choice. Recent innovations, such as multi-chamber soft bags that allow mixing components immediately before administration, further drive their adoption.

Volume InsightsThe 500 ML – 1000 ML segment holds a prominent share in the LVP market because it is ideal for various medical applications. This volume suits fluid resuscitation, electrolyte replenishment, parenteral nutrition, and intravenous drug administration. Healthcare professionals often prefer this size because it delivers adequate therapeutic doses while minimising fluid overload risk and waste. It also aligns with global clinical practice standards, making it a convenient option across varied healthcare settings. The growth of this segment is further propelled by the increasing incidence of chronic conditions requiring prolonged intravenous therapy, such as cancer and renal disease. Moreover, many hospitals are standardising this volume in treatment protocols to streamline inventory management and reduce errors.

Application InsightsTherapeutic injections represent the largest and fastest-growing application segment in the market. They are crucial for delivering a wide range of drugs, including antibiotics, analgesics, antipyretics, and chemotherapy agents, directly into the bloodstream for rapid systemic effects. The escalating burden of chronic diseases such as diabetes, cancer, and cardiovascular disorders has significantly increased the reliance on injectable therapies. Furthermore, the global rise in minimally invasive and surgical procedures drives demand for perioperative medication delivery, often administered through LVPs. The evolution of complex biologics and targeted therapies requiring precision dosing has also spurred advancements in LVP-based drug delivery. Pharmaceutical companies increasingly invest in developing LVP-compatible formulations to enhance therapeutic outcomes and patient compliance.

End Users InsightsHospitals are the dominant end users in the LVP market, consuming the largest share due to their extensive infrastructure, high patient turnover, and complex treatment regimens. They rely on LVPs for multiple clinical uses, including hydration therapy, electrolyte correction, medication infusion, and total parenteral nutrition (TPN). The increasing prevalence of inpatient admissions, particularly among ageing populations and patients with chronic or critical illnesses, further amplifies LVP demand. Hospitals also benefit from in-house compounding and centralised pharmacy systems, which facilitate the safe and efficient use of large-volume infusions. Additionally, the growing adoption of value-based care models encourages hospitals to use LVPs in standardised treatment protocols to improve outcomes and reduce readmission rates. Continuous upgrades in hospital infrastructure in emerging economies are expected to expand the footprint of LVPs in these settings.

Company Market ShareThe global large volume parenteral (LVP) market is fragmented, with multinational giants and regional manufacturers competing on innovation, pricing, and distribution. Leading players follow a strategy of regional expansion, capacity building, and product innovation (especially ready-to-administer formulations). Mergers, acquisitions, and government collaboration are key strategic patterns. The market is marked by consistent investment in sterile processing technologies and partnerships with hospitals and diagnostic centres to improve therapy access.

Fresenius Kabi: Fresenius Kabi is a global leader in the LVP market, offering a diverse range of IV fluids, nutrition solutions, and injectable drugs. The company has a strong footprint in Europe and North America and continues expanding in Asia-Pacific. Its strategy emphasises R&D investment, local manufacturing, and partnerships with public health systems. In January 2025, it completed the acquisition of a sterile injectable plant in Malaysia, boosting its supply chain resilience in the Asia-Pacific region.

Latest News:

-

In March 2025, Fresenius Kabi announced the launch of a new line of ready-to-use oncology LVP infusions across European hospitals, addressing the rising demand for time-saving, contamination-free solutions.

-

Baxter International Inc.

Fresenius Kabi

Braun Melsungen AG

Pfizer Inc.

ICU Medical Inc.

Terumo Corporation

Otsuka Pharmaceutical

Vifor Pharma

JW Life Science

Kelun Pharmaceutical

Aculife Healthcare

Amanta Healthcare

Grifols S.A.

Sanofi S.A.

-

October 2024- Following Hurricane Helene's impact on Baxter's North Carolina plant, B. Braun Medical ramped up production of IV fluids by 20% at its facilities in Irvine, California, and Daytona Beach, Florida. This increase in production aims to address the nationwide IV fluid shortage and ensure the continuous supply of critical medical solutions to healthcare providers.

October 2024- Fresenius Medical Care announced plans to increase production of IV fluids and peritoneal dialysis (PD) products to alleviate shortages caused by disruptions in the supply chain. The company is maximising production capacity at its international sites to help add supply amid the industrywide shortage of PD products and IV fluids.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.08 Billion |

| Market Size in 2026 | USD 9.49 Billion |

| Market Size in 2034 | USD 13.46 Billion |

| CAGR | 4.47% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Type, By Volume, By Application, By End Users |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Large Volume Parenteral (LVP) Market Segments By Type-

Soft Bag LVP

Plastic Bottle LVP

Glass Bottle LVP

-

100 ML – 250 ML

250 ML – 500 ML

500 ML – 1000 ML

1000 ML – 2000 ML

2000 ML and More

-

Therapeutic Injections

Fluid Balance Injections

Nutritious Injections

-

Hospitals

Clinics

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment