403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Pharmaceutical Membrane Filtration Market Size, Share & Growth Graph By 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

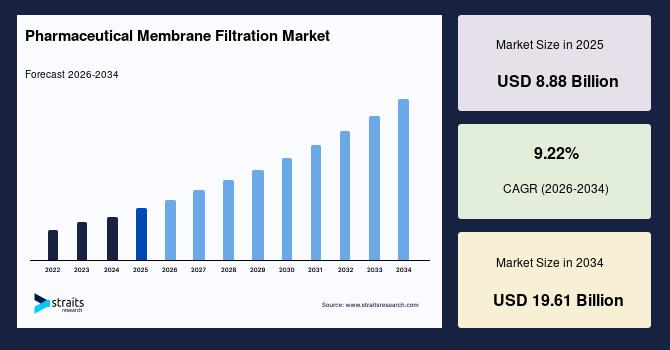

| 2025 Market Valuation | USD 8.88 Billion |

| Estimated 2026 Value | USD 9.68 Billion |

| Projected 2034 Value | USD 19.61 Billion |

| CAGR (2026-2034) | 9.22% |

| Study Period | 2022-2034 |

| Dominant Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Key Market Players | Merck KGaA, Danaher Corporation, Sartorius AG, Thermo Fisher Scientific Inc., 3M |

Download Free Sample Report to Get Detailed Insights.

Emerging Trends in Pharmaceutical Membrane Filtration Market Increasing AI-driven Integrity Monitoring in Membrane Filtration SkidsPharmaceutical manufacturers are increasingly integrating AI-based predictive analytics into membrane filtration skids to detect fouling, pressure deviations, and flux decline in real time. Systems embedded in single-use ultrafiltration units can now analyze transmembrane pressure trends and trigger automated adjustments, reducing batch failure risk. Companies like Sartorius AG and Danaher's Cytiva are deploying digitally connected filtration platforms in bioprocess lines, improving yield consistency in monoclonal antibody production. Early industrial data indicates up to a 20-25% reduction in membrane replacement frequency due to predictive fouling alerts.

Rise of Next-generation Virus Filtration for mRNA and Gene Therapy WorkflowsThe surge in mRNA vaccines and AAV-based gene therapies is driving demand for ultra-high-retention virus filtration membranes capable of handling fragile biomolecules without structural loss. Advanced asymmetric PVDF and nanofiber-enhanced filters are being engineered to achieve >4-log viral clearance while maintaining high protein recovery. Companies like Merck KGaA and Asahi Kasei are introducing low-shear virus filtration capsules optimized for lipid nanoparticle-based mRNA formulations. These systems are now critical in multi-step purification chains, where even minor yield loss directly impacts high-cost biologics manufacturing economics.

Pharmaceutical Membrane Filtration Market Drivers Expansion of Monoclonal Antibody and Growing Integration of Continuous Bioprocessing Platforms Drives MarketThe rapid scale-up of monoclonal antibody and antibody drug conjugate pipelines in 2025 is significantly accelerating demand for membrane filtration systems due to higher bioreactor volumes and multi-stage downstream purification requirements. Companies such as Samsung Biologics have expanded their capacity to approximately 785,000 liters with the new 180,000-liter Plant 5, specifically configured for advanced biologics including mAbs and ADCs. These expansions increase reliance on ultrafiltration, virus filtration, and depth filtration steps per batch, intensifying consumable usage and reinforcing long-term growth for membrane filtration suppliers globally in bioprocessing workflows.

The increasing adoption of continuous bioprocessing in biologics manufacturing is reshaping membrane filtration demand by replacing batch-based purification with nonstop production workflows. For instance, WuXi Biologics expanded perfusion-based upstream systems integrated with continuous downstream clarification trains, while Samsung Biologics implemented similar hybrid continuous platforms to enhance biologics output efficiency. These systems rely heavily on alternating tangential flow ultrafiltration for continuous cell retention. This extended runtime significantly increases membrane loading, fouling frequency, and consumable replacement cycles, driving sustained demand for filtration membranes globally.

Pharmaceutical Membrane Filtration Market Restraints High Rate of Batch Failures and Complexity Integration with Existing Bioprocessing Infrastructure Restrain Pharmaceutical Membrane Filtration Market GrowthA high rate of batch failures and product loss caused by membrane fouling and protein binding in complex biologics in high-value monoclonal antibody and ADC processes restrains market growth. CDMOs reported fouling-related flux decline during ultrafiltration, which can lead to 5–8% yield loss per batch in poorly optimized systems in high-concentration feed streams. This is critical for manufacturers like Lonza and Samsung Biologics, where a single failed batch can exceed multi-million-dollar losses, discourage frequent membrane changeovers, and slow adoption of newer filtration formats.

A key restraint in the pharmaceutical membrane filtration market is the difficulty of integrating advanced filtration skids into existing bioprocessing infrastructure without disrupting validated GMP production workflows. CDMOs transitioning from traditional stainless-steel batch systems to single-use ultrafiltration and virus filtration setups require extensive reconfiguration of pumps, pressure controls, and sterile connections. Manufacturing facilities experience multi-week downtime during retrofitting. Compatibility issues between new ATF-based perfusion systems and legacy downstream equipment further increase validation time, commissioning complexity, and overall implementation cost significantly across biologics manufacturing plants.

Pharmaceutical Membrane Filtration Market Opportunities Advancements in Nanofiltration Technology and Expansion of Biosimilar Production Offer Growth Opportunities for Pharmaceutical Membrane Filtration Market PlayersAdvancements in nanofiltration technologies are creating significant opportunities in the market by enabling higher selectivity and improved removal of small contaminants while preserving complex biologics. Currently, next-generation nanofiltration membranes with tighter pore distribution and surface-modified polymers are adopted for monoclonal antibody polishing and viral clearance steps. Companies like Merck KGaA and Asahi Kasei are developing low-protein-binding nanofilters that enhance yield efficiency in ADC and mRNA workflows. These innovations improve process efficiency, reduce purification cycles, and support high-purity biologics manufacturing at commercial scale globally.

Expansion of biosimilar production in emerging markets is creating a strong opportunity for pharmaceutical membrane filtration systems due to the need for cost-efficient, high-throughput downstream purification. Countries such as India, South Korea, and China are scaling biosimilar monoclonal antibody production to reduce dependency on originator biologics, increasing global supply contracts. These facilities rely heavily on ultrafiltration and virus filtration membranes to ensure regulatory compliance with EMA and FDA standards. This expansion increases demand for scalable, reusable, and cost-optimized membrane filtration technologies across large-volume biosimilar manufacturing lines.

Regional Analysis North America: Market Leadership through Increasing Membrane Consumption Intensity and Increasing Biosimilar Manufacturing BaseNorth America accounted for the largest share of 32.15% in the pharmaceutical membrane filtration market in 2025. This growth is propelled by FDA-mandated multi-stage viral clearance requirements that enforce redundant ultrafiltration and nanofiltration steps per biologics batch, increasing membrane consumption intensity. Rapid expansion of US mRNA and gene therapy manufacturing is further driving high-volume sterile filtration in fill-finish operations. FDA-aligned modernization of CDMO facilities toward continuous bioprocessing under regulatory facilitation programs is boosting real-time membrane utilization and reducing downtime, strengthening regional demand.

Growing regulatory requirements for extractables and leachables requalification for each single-use membrane change, increasing testing frequency, and validated product turnover in GMP environments are driving growth in the US pharmaceutical membrane filtration market. Growth in biosimilar manufacturing under the Purple Book pathway is also intensifying downstream purification needs in monoclonal antibody production using ultrafiltration and virus filtration. In addition, NIH and BARDA-funded biomanufacturing initiatives for pandemic preparedness are accelerating continuous production systems, raising membrane consumption intensity across US facilities.

Health Canada's strict biologics manufacturing compliance framework mandates enhanced virus filtration validation for biologics imported from US and EU facilities. This increases local testing and re-filtration demand, which boosts the pharmaceutical membrane filtration market in Canada. Furthermore, Canada's government-backed biomanufacturing resilience strategy is accelerating investments in modular, single-use filtration systems for rapid vaccine and biologics surge-capacity production nationwide.

Asia Pacific: Fastest Growth Driven by Regional Vaccine Self-sufficiency Mandates and Strict Regulatory GuidelinesThe Asia Pacific pharmaceutical membrane filtration market is expected to register the fastest regional growth with a CAGR of 11.83% during the forecast period due to the rapid establishment of regional vaccine self-sufficiency mandates, where countries like Indonesia, Vietnam, and Thailand are building national biologics fill-finish hubs that require sterile filtration capacity to reduce import dependency. China's centralized biopharma cluster model in zones like Zhangjiang and Suzhou is enforcing shared GMP filtration utilities across multiple CDMOs, raising membrane utilization intensity per production line. Furthermore, South Korea's K-Bio strategy is accelerating plug-and-play modular bioreactors requiring integrated single-use filtration skids, boosting advanced membrane adoption.

The pharmaceutical membrane filtration market in China is expanding due to the government's centralized biopharma cluster strategy in regions like Shanghai and Jiangsu, where shared GMP-certified downstream filtration utilities are reducing production redundancy and increasing membrane turnover intensity. Additionally, China's rapid scale-up of domestic CDMOs under the“Made in China 2025” biopharma push is accelerating high-volume ultrafiltration demand for biosimilars. Furthermore, strict NMPA alignment with ICH guidelines is forcing multi-stage virus filtration adoption in biologics export batches.

Hospital-linked biologics manufacturing is closely tied to national procurement cycles in Japan. This requires highly consistent filtration quality for oncology and autoimmune therapies, which boosts the Japan pharmaceutical membrane filtration market. Strict PMDA inspection standards mandate integrity testing of every single-use membrane system before batch release, significantly increasing validation intensity. Decentralized small-scale GMP facilities in regional prefectures, supported by aging-focused healthcare models, are adopting high-efficiency filtration skids for ultra-pure biologics production. All these factors are expected to pace the growth of the pharmaceutical membrane filtration market in Japan.

By MaterialThe polyethersulfone segment accounted for the largest share of the pharmaceutical membrane filtration market, by material, accounting for a share of 31.24% in 2025. This dominance can be attributed to its exceptional protein-binding resistance, making it ideal for high-yield monoclonal antibody purification in ultrafiltration steps. The thermal and oxidative stability of polyethersulfone under repeated gamma sterilization cycles supports widespread use in single-use bioprocessing systems.

The polyvinylidene difluoride segment is expected to grow at a CAGR of 9.76% during the forecast period, driven by strong chemical resistance against harsh biologics buffers and cleaning agents, making it ideal for virus filtration in mAb and ADC production. The high mechanical strength of polyvinylidene difluoride supports high-pressure filtration systems, while low protein binding ensures superior biologics recovery in GMP workflows.

By TechnologyThe microfiltration segment led the technology segment with a share of 42.62% in 2025, given its essential role in clarifying high-density mAb bioreactor harvests by efficiently removing cell debris. It is widely used as a pre-filtration step before ultrafiltration and virus filtration to reduce fouling. Single-use depth filters further support rapid GMP batch turnover and contamination control.

Nanofiltration is expected to grow at a CAGR of 9.75% during the forecast period due to its ability to precisely remove divalent ions and trace organics in monoclonal antibody polishing, which enhances yield retention. It is increasingly used in mRNA vaccine purification to eliminate nucleic acids and lipid nanoparticle residues, while enabling buffer exchange in continuous bioprocessing systems.

By ApplicationPharmaceutical production accounted for a dominant share of 59.41% of the pharmaceutical membrane filtration market, by application, in 2025. This is due to high-volume biologics manufacturing requiring multi-step membrane filtration in mAb and ADC purification. Strict GMP compliance mandates extensive sterile filtration usage. Rising single-use bioprocessing adoption in commercial-scale drug production significantly increases consumable membrane demand across continuous manufacturing lines.

The process water purification segment is expected to have the fastest growth, registering a CAGR of 10.18% during the forecast period. GMP-driven real-time water monitoring is replacing legacy systems, while single-use bioprocessing platforms increasingly integrate pre-sterilized water loops, boosting membrane filtration consumption in pharma facilities.

By End UsePharmaceutical & biotechnology companies accounted for the largest share of the end-use segment in the pharmaceutical membrane filtration market in 2025, accounting for a share of 63.20%. In-house biologics manufacturing requires multi-stage membrane filtration in mAb and ADC production pipelines, which boosts segmental demand. Strong adoption of single-use systems in GMP facilities increases consumable usage. Continuous expansion of cell and gene therapy pipelines drives high-purity downstream filtration demand.

The research & academic institutions segment is expected to register a CAGR of 10.64% during the forecast period due to rising bioprocess R&D for mAb and vaccine prototyping using membrane filtration systems. Government-funded cell and gene therapy studies require ultrafiltration tools, while expansion of pilot-scale GMP training labs increases adoption of single-use filtration for process optimization research.

Competitive LandscapeThe pharmaceutical membrane filtration market is moderately consolidated, with a few global bioprocessing leaders controlling high-value sterile and single-use filtration demand, while several niche players compete in specialized applications. Dominant companies include Merck KGaA, Danaher Corporation, Sartorius AG, Thermo Fisher Scientific, 3M Company, and Asahi Kasei Corporation, which lead in integrated bioprocess filtration systems. Mid-tier participants such as Parker Hannifin Corporation, Eaton Corporation, and Porvair plc focus on process and industrial filtration modules, while specialized firms like Meissner Filtration Products and Repligen Corporation emphasize single-use and perfusion technologies. Competition is intensifying through acquisitions, capacity expansion, and innovation in high-throughput membrane platforms.

List of Key and Emerging Players in Pharmaceutical Membrane Filtration Market Merck KGaA Danaher Corporation Sartorius AG Thermo Fisher Scientific Inc. 3M GE HealthCare Technologies Asahi Kasei Corporation Parker Hannifin Corporation Eaton Corporation plc Alfa Laval Repligen Corporation Meissner Filtration Products Inc. Donaldson Company Inc. Corning Incorporated Saint-Gobain Life Sciences GEA Group Porvair plc Graver Technologies Recent Developments-

In September 2025, Merck KGaA deepened its collaboration with Siemens (industrial and digital integration) to enhance digitalization and efficiency in downstream bioprocessing, including filtration and purification workflows.

In September 2025, Sartorius AG expanded its manufacturing and R&D site in Illkirch, France.

In September 2025, Thermo Fisher Scientific announced the acquisition of Solventum's purification and filtration business, amounting to USD 4.1 billion.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.88 Billion |

| Market Size in 2026 | USD 9.68 Billion |

| Market Size in 2034 | USD 19.61 Billion |

| CAGR | 9.22% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Material, By Technology, By Application, By End Use |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Pharmaceutical Membrane Filtration Market Segments By Material-

MCE Membrane Filters

Coated Cellulose Acetate

Nylon

Polyethersulfone

Polyvinylidene Difluoride

Other Materials

-

Microfiltration

Ultrafiltration

Nanofiltration

Reverse Osmosis

-

Pharmaceutical Production

Wastewater Treatment

Process Water Purification

Other Applications

-

Pharmaceutical & Biotechnology Companies

Research & Academic Institutions

Other End Uses

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment