403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Coffee Pods And Capsules Market Size, Top Share, Demand Industry Report, 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

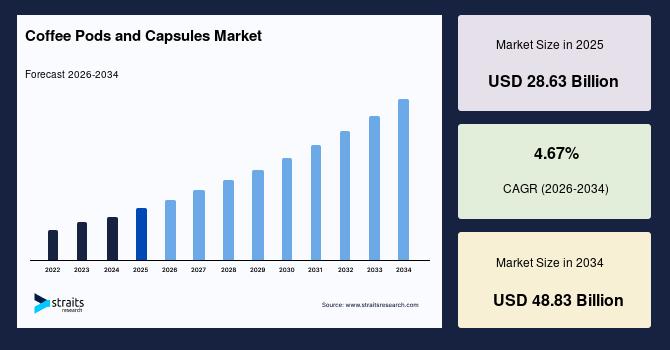

| 2025 Market Valuation | USD 28.63 Billion |

| Estimated 2026 Value | USD 31.75 Billion |

| Projected 2034 Value | USD 48.83 Billion |

| CAGR (2026-2034) | 4.67% |

| Dominant Region | Europe |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Nestle SA, The Kraft Heinz Company, inspire brands inc. (DUNKIN BRANDS), Luigi Lavazza SpA, JAB Holding Company |

Download Free Sample Report to Get Detailed Insights.

Emerging Trends in Coffee Pods and Capsules Market Shift toward compostable and biodegradable capsulesManufacturers are rapidly transitioning to compostable materials due to growing environmental concerns and increasing scrutiny on single-use waste. Some coffee pods are now engineered to biodegrade within 2–3 months under suitable composting conditions, reflecting a significant shift in material innovation across the industry. This transition is reshaping product development priorities, as companies invest in bio-based polymers and certified compostable solutions to meet regulatory expectations and evolving consumer preferences. The shift also supports brand positioning around sustainability while encouraging the development of improved disposal infrastructure and clearer labeling standards, ultimately influencing purchasing behavior and long-term market adoption.

Rising adoption of lightweight capsule designs for resource efficiencyIncreasing emphasis on lightweight and material-optimized coffee capsule designs is reshaping product engineering and manufacturing strategies across the market. Manufacturers are adopting advanced design optimization techniques to reduce material usage while maintaining the pressure resistance and sealing integrity required for high-quality brewing performance. These thin-material capsule structures enhance manufacturing efficiency by lowering raw material consumption and associated costs, while also reducing the environmental footprint at the production stage. In parallel, companies are leveraging precision molding and material science innovations to achieve an optimal balance between durability and minimal material input. This trend is strengthening scalability and operational efficiency while aligning with sustainability objectives, without compromising product functionality or consumer experience.

Market Drivers Expansion of home-based coffee consumption and single-serve machine ecosystems drives market growthThe expansion of single-serve coffee machine installations is significantly driving recurring demand in the coffee pods and capsules market. The growing installed base of capsule-compatible machines, particularly within proprietary systems, creates a closed-loop consumption model where users repeatedly purchase compatible pods, strengthening brand loyalty and revenue predictability. This ecosystem-based structure enhances customer retention while enabling manufacturers to control product compatibility, pricing strategies, and distribution channels. As machine penetration increases across households and commercial settings, it establishes a sustained consumption cycle, directly accelerating market growth and reinforcing long-term demand stability.

The growth in at-home coffee consumption habits is further accelerating the adoption of coffee pods and capsules, driven by shifting consumer preferences toward convenience and premium experiences within residential settings. Consumers increasingly seek café-style beverages at home, supported by rising ownership of coffee machines and evolving lifestyle patterns that prioritize comfort and personalization. This shift expands the addressable consumer base while increasing consumption frequency, as individuals replace out-of-home coffee purchases with in-home alternatives. As a result, manufacturers are focusing on offering diverse blends, flavors, and intensity levels tailored to home users, strengthening product differentiation and driving sustained demand in the market.

Market Restraints Competition from alternative brewing methods and limited affordability in price-sensitive regions restrain market growthCompetition from alternative brewing methods remains a significant restraint for the coffee pods and capsules market, as traditional formats such as drip coffee, French press, and instant coffee continue to be widely adopted due to their lower cost and minimal packaging waste. These methods offer greater flexibility in coffee selection and preparation while eliminating dependency on proprietary machines and single-use capsules. As a result, a large segment of consumers, particularly those prioritizing cost efficiency and sustainability, prefer conventional brewing approaches. This substitution effect limits the conversion of traditional coffee users to capsule-based systems and restricts the overall expansion potential of the market.

Limited adoption in low-income and rural markets further constrains the growth of the coffee pods and capsules market, primarily due to the high upfront cost of compatible coffee machines and the recurring expense associated with capsule purchases. Price-sensitive consumers in these regions tend to favor more economical coffee preparation methods that require minimal investment and offer lower per-serving costs. Additionally, limited access to organized retail and e-commerce distribution channels in rural areas reduces product availability and awareness. These factors collectively hinder market penetration, restricting geographic expansion and slowing the pace of adoption in emerging and underserved regions.

Market Opportunities Expansion of premium hospitality and localization offerings offers growth opportunities for coffee pods and capsules market playersThe penetration into HoReCa (Hotels, Restaurants, and Cafés) premium segments is creating significant growth opportunities for the coffee pods and capsules market, as high-end hospitality providers increasingly prioritize consistency, efficiency, and premium beverage experiences. Capsule-based systems enable standardized brewing quality with minimal training requirements, ensuring uniform taste and presentation across multiple service locations. This is particularly valuable for luxury hotels, upscale restaurants, and boutique cafés that aim to deliver high-quality coffee while optimizing operational efficiency. As the hospitality sector continues to focus on enhancing customer experience and service speed, the adoption of capsule systems is expanding, creating sustained demand and new revenue streams for market players.

The localization of coffee flavors and regional blends is also unlocking strong growth opportunities within the coffee pods and capsules market. Manufacturers are increasingly developing region-specific flavor profiles tailored to local taste preferences, such as stronger brews, traditional preparation styles, and culturally familiar flavor notes. This approach enhances consumer relevance and acceptance, particularly in emerging markets where coffee consumption patterns vary significantly. By aligning product offerings with regional preferences, companies can expand their customer base, improve market penetration, and differentiate their portfolios. This localization strategy not only strengthens brand positioning but also supports deeper market integration across diverse geographic regions.

Regional Insights Europe: market leadership driven by established coffee culture, mature retail channels, and growing sustainable packagingEurope held a dominant share of 42.45% in 2025, driven by well-established coffee consumption habits and widespread adoption of single-serve systems. High awareness of premium coffee experiences and convenience has led to strong demand for both pods and capsules across households and offices. The region's mature retail infrastructure, including supermarkets, hypermarkets, and specialty stores, supports broad product availability, while online platforms are contributing to growing direct-to-consumer sales. Sustainability considerations are increasingly influencing packaging preferences, with biodegradable and compostable options gaining traction alongside traditional plastic and aluminum capsules. On-trade channels, such as cafés and restaurants, continue to supplement home consumption, but off-trade remains dominant. Consumers' preference for high-quality coffee, coupled with the presence of leading coffee machine manufacturers, reinforces market stability. These factors collectively position Europe as the key region in terms of market size, with steady growth expected to continue over the forecast period.

The UK coffee pods and capsules market is increasingly shaped by evolving consumer habits and broader food trends. Official data from the UK government indicates that British families have shifted away from traditional tea consumption, with coffee playing a growing role in everyday diets, reflecting broader dietary diversification in recent years. Coffee's rising prominence as a preferred beverage supports demand for convenient formats such as coffee pods and capsules, especially among younger urban consumers who value quick, highquality brews at home. While comprehensive per capita coffee consumption figures are not provided directly by government sources, these dietary trend shifts imply a stronger preference for coffee beverages within households. Government publications also highlight broader food price inflation, including for coffee products, which influences consumer purchasing behavior and may accelerate the transition toward singleserve consumption formats as consumers seek convenience and perceived value. This combination of shifting dietary patterns and economic influences underpins the increasing integration of pods and capsules within the market.

The Germany coffee pods and capsules market is driven by high consumer engagement and extensive industry infrastructure. According to official tradelinked statistics, nearly 89 % of Germans consume coffee regularly, and average annual per capita coffee consumption stands at about 5.4 kg, exceeding the broader European average. This strong consumption intensity reflects ingrained coffee culture, where coffee is part of daily routines at home and in social settings. Germany's significant role in the European coffee value chain is also evident in its major roasting capacity, producing hundreds of thousands of tonnes of roasted coffee and positioning it as one of the continent's leading coffee processing hubs. Furthermore, the country is a major importer of green coffee beans, including organic and Fairtradecertified varieties, which support growth in premium and sustainabilityoriented products. These structural dynamics provide favorable conditions for expansion in formats such as singleserve pods and capsules, particularly as consumer preferences evolve toward convenience and quality.

Asia Pacific: fastest growth driven by preference for premium experience and shifting consumption patternAsia Pacific is expected to register the fastest growth with a CAGR of 7.20% during the forecast period, driven by changing consumer lifestyles and increased urbanization. Rising disposable incomes and the expansion of the middle-class population have led to a growing preference for convenient, high-quality coffee consumption at home and in offices. Urban centers are fostering café culture, which encourages experimentation with single-serve coffee formats that combine ease of use with consistent quality. Expanding retail networks and the proliferation of e-commerce platforms further enhance accessibility to coffee pods and capsules, allowing consumers to explore a wide variety of flavors and blends. Additionally, younger demographics are increasingly attracted to premium and specialty coffee products, supporting diversification of offerings. This combination of economic growth, evolving consumption habits, and improving retail and distribution infrastructure positions Asia Pacific as the fastest-growing region in the global coffee pods and capsules market, with strong momentum expected over the forecast period.

The China coffee pods and capsules market is gaining strong momentum as consumer preferences shift toward convenient and premium coffee experiences. Increasing urbanization and evolving lifestyles have driven more people to seek ready‐to‐brew coffee formats that offer consistency and ease. Traditional tea culture is gradually complemented by coffee consumption, particularly in major cities where modern café culture is expanding. Young professionals and students are showing heightened interest in single‐serve coffee formats that fit their fast‐paced routines and preference for high‐quality beverages at home or work. Retail infrastructure, including supermarkets, specialty stores, and online platforms, has broadened access to a wide range of coffee pods and capsules, enabling easier exploration of different brands and flavor profiles. Improvements in e‐commerce and delivery systems further support consumer adoption by allowing quick and convenient access to products. All these factors contribute to sustained growth in China's coffee pods and capsules market.

The India coffee pods and capsules market is emerging as an attractive segment within the broader beverage industry, driven by shifting consumption patterns and rising interest in Western coffee culture. As lifestyles become increasingly modern and urban consumers seek convenience, single‐serve coffee formats are gaining traction among young adults and white‐collar professionals who value simplicity without compromising taste. The expansion of retail networks, including supermarkets, convenience stores, and especially online channels, has made it more accessible for consumers to try and adopt pods and capsules. Additionally, a growing preference for premium and flavored coffee options adds appeal to single‐serve offerings that provide a consistent and high‐quality brewing experience. Cultural shifts toward café visits and at‐home brewing routines further support market development. With these evolving preferences and broader accessibility, India's coffee pods and capsules market is poised for gradual but sustained growth.

By TypeThe pods segment dominated the market in 2025 and is expected to grow at a CAGR of 4.67% over the forecast period due to their wide compatibility with coffee machines, ease of use, and affordability. They appeal to consumers seeking consistent flavor and a quick brewing experience at home or in offices. The simple design and compact packaging make them convenient for storage and disposal. Pods also offer a broad variety of coffee blends, meeting diverse consumer taste preferences. Their accessibility through multiple retail channels further reinforces their dominance. Consumer familiarity and preference for tried-and-tested formats keep pods as the leading type in the market, driving consistent demand across regions.

The capsules segment represents the fastest-growing segment at a CAGR of 6.32% during the forecast period, as consumers increasingly seek premium coffee experiences. Their airtight, sealed design preserves freshness and flavor, making them attractive for specialty coffee enthusiasts. Capsules support diverse blends, single-origin offerings, and flavored coffees, catering to the demand for high-quality beverages. Growing interest in at-home brewing, combined with compatibility with advanced coffee machines, accelerates their adoption. The format aligns with trends toward convenience without compromising taste. Marketing campaigns emphasize luxury, variety, and sustainable packaging options. They further stimulate growth, positioning capsules as the fastest-growing type in the coffee pods and capsules market.

By Packaging MaterialThe plastic segment dominated the market with a share of 44.46% in 2025, due to its cost-effectiveness, durability, and ability to maintain product integrity. It provides reliable protection from moisture and contamination while keeping production and logistics efficient. Consumers appreciate the lightweight and convenient design, which allows easy handling and storage. Plastic packaging supports mass production and broad retail availability, making it accessible to a wide consumer base. Its versatility accommodates various coffee blends and flavors, reinforcing its continued preference in the market. Despite sustainability concerns, plastic packaging remains dominant due to practicality, affordability, and widespread adoption in existing coffee pod and capsule infrastructure.

The biodegradable and compostable segment is expected to register a CAGR of 8.50% during the forecast period, driven by rising environmental awareness and demand for sustainable alternatives. Consumers are increasingly conscious of the ecological impact of single-use products, prompting manufacturers to adopt materials that decompose naturally. These eco-friendly formats maintain freshness and flavor while aligning with sustainability trends, attracting environmentally minded buyers. Growth is supported by innovation in renewable materials and improvements in compostable designs, making them comparable in convenience to traditional packaging. Marketing focused on environmental responsibility further drives consumer adoption. As governments and organizations emphasize sustainability, biodegradable and compostable packaging is becoming the fastest-growing material segment in the coffee pods and capsules market.

By Distribution ChannelThe off-trade segment dominated the market in 2025 and is expected to grow at the CAGR of 5.96% over the forecast period due to widespread accessibility and convenience. Consumers prefer purchasing coffee pods and capsules from these outlets for consistent availability, variety, and the ability to compare products. Off-trade retail allows bulk purchases and home stocking, catering to habitual consumption patterns. Extensive distribution networks ensure products reach urban and suburban areas efficiently, supporting high penetration. The channel also accommodates promotional activities, discounts, and loyalty programs that reinforce consumer preference. Its reliability, convenience, and variety make off-trade the leading distribution method in the coffee pods and capsules market.

The on-trade segment is expected to register a CAGR of 4.82% during the forecast period. The segment includes cafés, restaurants, hotels, and other foodservice outlets, offering consumers freshly prepared coffee in controlled settings. This segment is growing steadily as it provides experiential value, allowing customers to enjoy high-quality beverages and explore diverse coffee flavors. On-trade channels often promote premium and specialty coffee offerings, reinforcing brand visibility and consumer loyalty. While convenience-oriented home consumption favors pods and capsules, on-trade remains important for introducing new products, sampling, and cultivating coffee culture. The segment also supports trends in customization, such as milk alternatives and flavored options, which enhance the overall consumer experience and maintain engagement with coffee products.

Competitive LandscapeThe coffee pods and capsules market is moderately fragmented, with a mix of global beverage corporations, established coffee roasters, machine manufacturers, and agile regional or specialty brands all vying for share. Established players primarily compete on brand recognition, extensive distribution networks, machine ecosystem compatibility, and consistent product quality, leveraging long-standing consumer trust and partnerships with retail and foodservice channels. Emerging players often differentiate through innovation in sustainable materials, niche flavor profiles, localized blends, and direct‐to‐consumer engagement via e‐commerce and subscription models. While price, convenience, and sustainability are universal competitive levers, newer entrants tend to focus more on agility, unique positioning, and targeted marketing. Going forward, the market will increasingly be shaped by advances in sustainable packaging solutions and deeper integration between coffee formats and brewing technologies.

List of Key and Emerging Players in Coffee Pods and Capsules Market Nestle SA The Kraft Heinz Company inspire brands inc. (DUNKIN BRANDS) Luigi Lavazza SpA JAB Holding Company Starbucks Corporation Gloria Jeans Coffees Strauss Group Keurig Dr Pepper Recent Developments-

In April 2026, Keurig Dr Pepper completed acquisition of JDE Peet's (96% stake), forming“Global Coffee Co.” and initiating a strategic spin-off to separate coffee and beverage businesses.

In October 2025, Keurig Dr Pepper, KKR, and Apollo Global Management established an approximately USD 4 billion joint venture to expand global K-Cup pod manufacturing capacity.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.63 Billion |

| Market Size in 2026 | USD 31.75 Billion |

| Market Size in 2034 | USD 48.83 Billion |

| CAGR | 4.67% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Type, By Packaging Material, By Distribution Channel |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Coffee Pods and Capsules Market Segments By Type-

Pods

Capsules

-

Plastic

Aluminum

Biodegradable/Compostable

-

On-trade

Off-trade

Supermarkets & Hypermarkets

Specialty Stores

Online Platforms

Other Distribution Channels

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment