403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Hydrogen Buses Market Size, Share And Forecast To 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

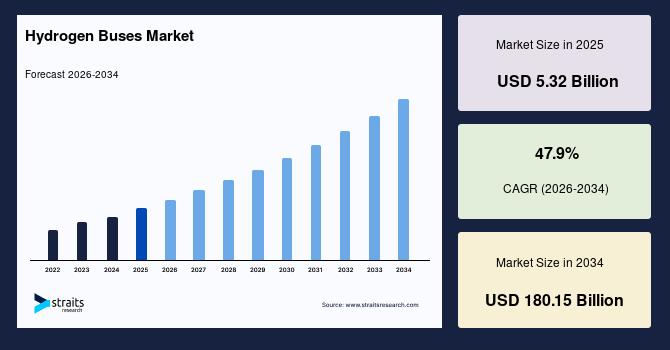

| 2025 Market Valuation | USD 5.32 Billion |

| Estimated 2026 Value | USD 7.87 Billion |

| Projected 2034 Value | USD 180.15 Billion |

| CAGR (2026-2034) | 47.9% |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | Ballard Power Systems, Toyota Motor Corporation, Hyundai Motor Company, Daimler Buses, Volvo Group |

Download Free Sample Report to Get Detailed Insights.

Emerging Trends in Hydrogen Buses Market Introduction of Stricter Emission Norms and Net-Zero TargetsGovernments worldwide are introducing strict emission norms and net-zero targets to reduce urban air pollution and carbon emissions. Public transport authorities are responding by shifting from diesel and CNG buses to cleaner alternatives. For instance, the European Union's European Green Deal mandates significant reductions in transport emissions, prompting cities like Hamburg to phase out diesel buses and adopt hydrogen-powered buses as part of their zero-emission public transport strategy. Thus, hydrogen buses gain preference where battery electric buses face range or charging limitations to support longer routes and faster refueling, improving operational efficiency for transit agencies. As policy support strengthens through subsidies and pilot programs, fleet operators accelerate hydrogen bus deployment across major cities.

Increasing Green Hydrogen InvestmentsInvestments in green hydrogen production and distribution networks strengthen fuel availability. For instance, India's National Green Hydrogen Mission, where pilot mobility projects are being implemented with 37 hydrogen-powered buses and trucks supported by 9 hydrogen refueling stations, strengthening hydrogen production and distribution infrastructure for transport applications. Governments and private players are developing hydrogen refueling stations along key transport corridors and urban centers, which reduces range anxiety and operational uncertainty for fleet operators. For example, the US Department of Transportation invested USD 635 million in 2025 to develop hydrogen refueling and EV infrastructure across 27 states, directly supporting the expansion of hydrogen refueling stations along key transport routes. As infrastructure becomes more reliable, transit agencies gain confidence to scale hydrogen bus fleets. The improved ecosystem supports continuous operations and encourages long-term investments in hydrogen mobility.

Hydrogen Mobility Programs and Urban Air Quality Regulations Driving Hydrogen Bus AdoptionGovernment-backed hydrogen mobility programs are playing a critical role in accelerating hydrogen bus deployment by identifying public buses as early adoption vehicles due to their centralized refueling and fixed-route operations. For example, under India's National Green Hydrogen Mission, the government sanctioned 5 pilot projects involving 37 hydrogen-powered buses and trucks and 9 hydrogen refueling stations, supported by USD 22.13 million in financial assistance. Such government-supported pilot deployments reduce operational risks, validate vehicle performance in real-world conditions, and encourage public transport authorities to include hydrogen buses in long-term fleet procurement programs, thereby supporting market expansion.

Urban air pollution reduction policies are also contributing significantly to hydrogen bus adoption, particularly in densely populated metropolitan regions where diesel buses are a major source of particulate emissions and nitrogen oxides. Many cities are implementing clean air action plans and low-emission public transport policies that require transit agencies to transition toward zero-emission bus fleets. Hydrogen buses are increasingly being deployed on high-frequency urban routes where emission reduction impact is the highest, helping cities meet air quality targets while maintaining public transport capacity and operational efficiency. These environmental regulations and clean mobility initiatives are therefore acting as a major demand driver for hydrogen buses in large urban transportation networks.

Market Restraints Hydrogen Storage Safety Regulations and Land Requirements for Refueling Infrastructure Restrain Hydrogen Buses Market GrowthHydrogen storage and transportation are subject to strict safety regulations due to their flammable nature, which increases compliance requirements for hydrogen bus operations and infrastructure deployment. Hydrogen refueling stations and storage facilities must comply with hazardous gas handling standards, fire safety regulations, pressure vessel certifications, and transport regulations for compressed hydrogen. These regulatory requirements involve multiple approvals from safety authorities, environmental agencies, and local planning bodies, which increases project approval timelines and delays hydrogen refueling infrastructure development. As hydrogen buses depend on dedicated refueling infrastructure, such regulatory complexity slows down large-scale fleet deployment and infrastructure expansion.

Hydrogen production and refueling stations also require dedicated land along with defined safety buffer zones to ensure safe storage and dispensing of hydrogen fuel. In densely populated urban areas, securing large parcels of land near bus depots or transit corridors is a major challenge due to high land costs, zoning restrictions, and urban planning limitations. Since hydrogen refueling infrastructure must be located within operational range of bus fleets, land availability becomes a critical constraint for transit agencies planning hydrogen bus deployment. This infrastructure-related land constraint is therefore a significant barrier to rapid expansion of hydrogen bus networks in major metropolitan areas.

Market Opportunities Renewable Energy Generation and Smart City Mobility Offers Growth Opportunities for Hydrogen Bus PlayersSolar and wind energy generation often produces excess electricity during off-peak hours due to variability in demand and supply mismatch. This surplus power can be diverted to electrolyzers to produce green hydrogen, enabling efficient energy storage instead of curtailment. Transit agencies and energy providers are increasingly forming integrated models where renewable energy plants directly supply hydrogen for public transport fleets, improving cost efficiency and energy utilization. For example, cities like Hamburg have linked wind energy projects with hydrogen production to fuel public buses, while Foshan uses locally produced hydrogen from industrial and renewable sources to operate large hydrogen bus fleets. This approach reduces dependency on grid balancing mechanisms and minimizes renewable energy wastage. The convergence of power generation and mobility sectors enhances system efficiency, stabilizes energy demand cycles, and accelerates the transition toward integrated, low-carbon transport ecosystems.

Integration of hydrogen buses into smart city mobility systems is also creating significant growth opportunities as cities are increasingly adopting integrated, low-emission public transport networks. Hydrogen buses are being incorporated into multimodal transport systems that include metro, electric buses, and shared mobility services to create sustainable urban transportation ecosystems. These smart mobility frameworks focus on reducing urban emissions, improving public transport efficiency, and optimizing energy usage across transport networks. As hydrogen buses can operate on long routes with centralized refueling infrastructure, they are becoming an important component of smart city transportation planning, creating long-term deployment opportunities in urban mobility modernization projects.

Regional Insights North America: Market Dominance through Public Transit Electrification Programs and Hydrogen Infrastructure InvestmentsNorth America accounted for a dominant share of 34.68% in 2025, supported by structured zero-emission public transit programs, hydrogen infrastructure investments, and long-term fleet electrification targets across major transit agencies. Public transport authorities across the region are transitioning toward fuel cell buses for routes requiring long range and high utilization, supported by dedicated funding programs for clean transit vehicles and hydrogen refueling infrastructure. In addition, several large transit agencies are planning multi-year zero-emission bus procurement programs through 2030, which include hydrogen fuel cell buses as part of diversified fleet strategies. The expansion of hydrogen corridors and depot-based refueling infrastructure is further supporting hydrogen bus deployment across metropolitan and regional transport networks.

The US market is expanding due to federal zero-emission transit funding and large-scale procurement programs by city transit agencies. The Federal Transit Administration's Low or No Emission Vehicle Program continues to allocate funding for hydrogen fuel cell buses and supporting infrastructure, enabling transit agencies to procure hydrogen buses for long-distance and high-capacity routes. In addition, the development of regional hydrogen hubs is expected to support hydrogen supply for transportation applications, including public bus fleets, creating long-term infrastructure support for hydrogen mobility.

The Canadian market is growing due to national hydrogen strategy initiatives and investments in zero-emission public transport projects. Canadian cities are deploying hydrogen fuel cell buses as part of public transit decarbonization plans, supported by federal clean transportation funding and hydrogen infrastructure development programs. The country's long-distance regional transport routes and cold climate conditions make hydrogen buses suitable for reliable year-round public transport operations, supporting continued deployment in municipal and regional transit systems.

Asia Pacific: Fastest Growth Driven by National Hydrogen Roadmaps and Large-scale Fleet Deployment ProgramsAsia Pacific is expected to register the fastest growth with a CAGR of 49.6% during the forecast period, driven by large-scale hydrogen mobility programs, expansion of hydrogen production capacity, and increasing deployment of hydrogen buses in high-capacity public transport systems. Several countries in the region are investing in hydrogen-powered public transport to reduce urban emissions and support long-distance public transportation where battery-electric buses face operational limitations. The region is also developing hydrogen refueling networks and localized manufacturing ecosystems, which is enabling large-scale fleet deployment and reducing dependency on imported fuel technologies. These developments are positioning Asia Pacific as the fastest-growing market for hydrogen buses over the forecast period.

China is witnessing large-scale deployment of fuel cell buses in urban transport systems and the development of regional hydrogen supply networks to support fuel cell vehicle operations. Several provinces are investing in hydrogen-powered public transport fleets as part of clean transportation programs and industrial hydrogen development strategies. China's strong domestic bus manufacturing industry and fuel cell supply chain are enabling large-scale production and deployment of hydrogen buses across multiple cities.

Japan focuses on a hydrogen-based transportation strategy and fuel cell mobility in public transport systems. Hydrogen buses are being deployed in metropolitan transport networks and major public events transportation systems as part of long-term hydrogen mobility development plans. The country is investing in hydrogen refueling infrastructure and fuel cell vehicle deployment programs to support the expansion of hydrogen-powered public transportation.

By Bus TypeThe single-decker hydrogen buses segment accounted for a share of 52.41% in 2025. The key factor contributing to the dominance of single-decker hydrogen buses is their extensive usage in urban public transportation networks, where passenger capacity requirements, route flexibility, and operational efficiency make them suitable for city transit systems. These buses are widely deployed on short- to medium-distance routes with frequent stops, making them the preferred choice for municipal transport authorities transitioning toward zero-emission fleets.

The articulated hydrogen buses segment is expected to grow at a CAGR of 50% during the forecast period. This growth is attributed to the increasing demand for high-capacity buses on densely populated routes, including bus rapid transit corridors and metropolitan transport networks. Articulated hydrogen buses enable transit operators to transport more passengers per trip while maintaining zero-emission operations, making them suitable for high-demand public transport corridors.

By TechnologyThe Solid Oxide Fuel Cells (SOFC) segment led the market with a revenue share of 38.12% in 2025. This dominance is attributed to the ability of SOFC technology to deliver high electrical efficiency and stable performance over extended operating cycles, making it well-suited for long-duration public transportation routes and intercity operations. The technology's efficiency and durability make it suitable for buses operating on long-distance routes requiring continuous power output.

The Proton Exchange Membrane Fuel Cells (PEMFC) segment is expected to register a CAGR of 48.7% during the forecast period. The growth is driven by increasing adoption of PEM fuel cells in public transportation due to their quick start-up capability, high power density, and suitability for stop-and-go urban driving conditions. Increasing standardization and production scale of PEM fuel cell systems are further supporting segment growth.

By Hydrogen SourceThe green hydrogen segment held the largest share of 46.32% in 2025, as green hydrogen enables completely zero-emission public transport operations and supports government decarbonization targets. Transit agencies and transport authorities are increasingly prioritizing green hydrogen to ensure that hydrogen bus operations contribute to long-term carbon reduction goals and sustainable urban mobility.

The blue hydrogen segment is expected to grow at a CAGR of 48.9% during the forecast period. This growth is primarily attributed to its role as a transitional hydrogen source in regions where renewable hydrogen production capacity is still developing. Blue hydrogen enables early deployment of hydrogen buses by providing relatively lower-emission hydrogen fuel while renewable hydrogen infrastructure continues to expand, thereby supporting the gradual transition toward fully green hydrogen-based public transportation systems.

By ApplicationThe public transit buses segment dominated the market with a revenue share of 58.64% in 2025. This dominance is attributed to the large-scale deployment of hydrogen buses by city transport authorities aiming to reduce emissions from urban transportation networks. Hydrogen buses are increasingly being integrated into metropolitan bus fleets due to their long operating range, fast refueling capability, and ability to operate on high-frequency routes without significant downtime. As cities continue to modernize public transport infrastructure and replace conventional diesel buses, public transit remains the primary application area supporting consistent demand for hydrogen buses.

The intercity coaches segment is expected to grow at a CAGR of 49.2% during the forecast period, driven by the increasing need for zero-emission solutions for long-distance routes where range, refueling time, and operational continuity are critical factors. Hydrogen buses are well suited for intercity transportation due to their extended driving range and ability to operate across long routes without frequent refueling stops, making them an emerging solution for sustainable intercity mobility.

Competitive LandscapeThe hydrogen buses market is moderately fragmented, with a mix of established commercial vehicle manufacturers, fuel cell technology providers, and emerging hydrogen mobility startups operating across the value chain. Established players primarily compete on technological reliability, vehicle range, fuel cell efficiency, large-scale manufacturing capability, and long-term contracts with public transit authorities. These companies also focus on strategic partnerships with hydrogen fuel suppliers and infrastructure providers to offer integrated mobility solutions. Emerging players, on the other hand, compete on niche innovations, flexible vehicle platforms, cost-competitive designs, and pilot project participation in developing hydrogen mobility markets. Many new entrants are targeting specific applications such as airport transport, intercity buses, and smart city mobility projects to establish their market presence.

List of Key and Emerging Players in Hydrogen Buses Market Ballard Power Systems Toyota Motor Corporation Hyundai Motor Company Daimler Buses Volvo Group Wrightbus Van Hool Solaris Bus & Coach CaetanoBus BYD Company Foton Motor New Flyer Industries ElringKlinger Plug Power Hyzon Motors IVECO Group Yutong Bus CRRC Corporation NFI Group Scania Recent Developments-

In March 2026, Ballard Power Systems announced a commercial agreement to supply 500 FCmove-HD+ fuel cell engines (50 MW capacity) for New Flyer's Xcelsior CHARGE FC hydrogen fuel cell buses, with deliveries starting in 2026.

In March 2026, Hyundai Motor Company launched the Universe Fuel Cell Electric Bus, designed for long-distance and intercity transportation. The hydrogen bus offers a driving range of up to 960 km on a single refueling and can be refueled in approximately 10 minutes, making it suitable for high-utilization transport routes.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.32 Billion |

| Market Size in 2026 | USD 7.87 Billion |

| Market Size in 2034 | USD 180.15 Billion |

| CAGR | 47.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Bus Type, By Technology, By Hydrogen Source, By Application |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Hydrogen Buses Market Segments By Bus Type-

Single Decker Hydrogen Buses

Double Decker Hydrogen Buses

Articulated Hydrogen Buses

-

Proton Exchange Membrane Fuel Cells

Direct Methanol Fuel Cells

Phosphoric Acid Fuel Cells

Zinc-Air Fuel Cells

Solid Oxide Fuel Cells

-

Green Hydrogen

Blue Hydrogen

Grey Hydrogen

-

Public Transit Buses

Airport Shuttles

Intercity Coaches

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment