403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

South Korea: Monthly Activity Data Suggest A Patchy Recovery Ahead

| -3.2% | Industrial production % MoM, sa |

| Lower than expected |

Manufacturing industrial production declined 3.2% MoM sa in March (vs revised 2.9% in February, 0.5% market consensus), with declines across all industries. Even though we think manufacturing will be one of the main drivers of growth this year, we are concerned that the strength will be quite narrowly concentrated in the semiconductor industry.

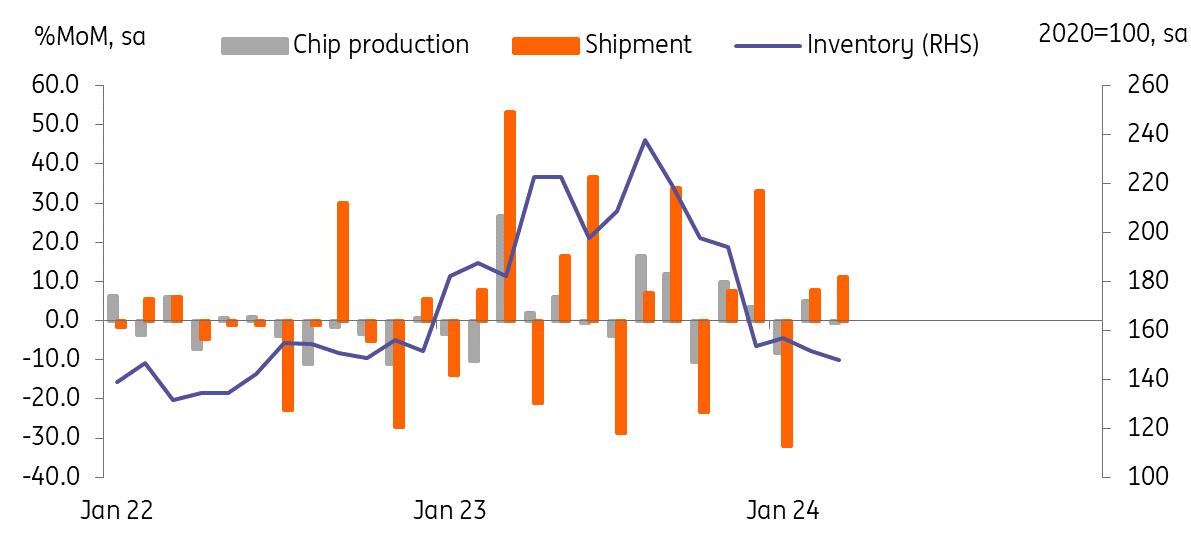

Semiconductor output declined -0.7%, but shipments rose smartly by 11.1% on the back of strong exports (14.5%) while domestic shipments were down -8.8%. Given that domestic chip usage is mainly for automobiles and electronic devices, the decline in domestic shipments suggests weak demand in legacy chip markets. However, strong exports suggest that demand for high-end chips remains solid, mainly driven by global investment in AI technology. Ongoing inventory cutting by semiconductor producers is also likely to be supportive of semiconductor production in the near term.

As for transportation equipment, motor vehicles (2.3%) and motor vehicle bodies (8.5%) rebounded but motor parts (-4.1%) and other transportation equipment (-5.9%) dropped more strongly. We think motor vehicle production is likely to recover but at a slower pace than last year.

High-end semiconductors will be the main growth driver

Source: CEIC Retail sales rose 1.6% MoM sa in March, partially reversing the previous month's 3.0% fall

The monthly gain in retail sales was mostly from strong automobile sales (11.3%) while other durable goods sales such as household appliances, telecom equipment, and furniture - were down. The three-month comparison dropped -0.2% showing that the underlying trend has been softening. Consumer sentiment and retail sales have held up relatively well, and we also saw a gain in private consumption in the recent GDP release. However, we believe that this will turn negative in the current quarter as tight financial conditions remain for longer than expected.

Investment should remain a concern for growth in the current quarterMachinery orders dropped -18.7% MoM sa in March, with both public and private orders falling. Given the volatile nature of this data, we tend to focus on the three-month comparison trend, which deepened its contraction to -9.4% 3Mo3M sa in March. So, we expect facility investment to fall in the current quarter.

For construction, both orders (-20.8% MoM sa) and construction completed (-8.8%) declined in March. Construction completed have now declined for two months in a row after a sharp rise in January. The current run of data suggests that the unexpected 1Q24 construction GDP rebound was temporary and we expected it to turn negative in the current quarter.

GDP forecastsGiven the stronger-than-expected 1Q24 GDP result (1.3% QoQ sa vs 0.6% market consensus), we have revised up our annual GDP outlook from 1.7% YoY to 2.5% YoY. Forward-looking data point to weak investment and services activity, while we expect the net export contribution to growth to diminish given the recent fast rise in commodity prices. Private consumption is still rather puzzling, but as tight financial conditions become more extended, it will start to bite more seriously into consumption in the current quarter. In sum, quarterly growth is expected to decelerate sharply to 0.1% QoQ sa in the current quarter from 1.2% in 1Q24. We will fine tune our quarterly growth outlook as more data becomes available.

Author:Min Joo Kang

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment