403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Poland's April 12-Month Current Account Deficit Above 3% Of GDP

(MENAFN- ING)

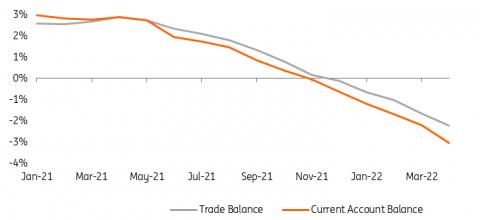

ING estimates based on NBP data.

The current account deficit was €3.9bn in April (consensus €2.3bn, our forecast €3.2bn), following a €3.0bn deficit in March. We estimate that on a 12-month basis the balance deteriorated from -2.2% of GDP to -3.0% of GDP (the largest 12-month deficit since April 2013). The merchandise trade deficit was €2.5bn in April after €3.3bn in March. On a cumulative 12-month basis, this represents an increase in the deficit from around 1.7% of GDP to 2.2% of GDP. A surplus in services balance of €2.2m did not offset high deficits: in primary income (€2.8m) and secondary income (€0.9m).

Foreign trade performance in April 2022 reflects the impact of the war in Ukraine: an increase in fuel import bills and a collapse in trade with Russia. The annual dynamics of imports of goods, expressed in euro (22.6% year-on-year) clearly exceeded the dynamics of exports (6.7%).

The National Bank of Poland communiqué indicates a significant influence of the disturbances in global supply chains and the war in Ukraine on Polish foreign trade. Global disruptions contributed to a decline in exports of automotive parts, TV sets and household appliances. A deep decline in sales to Russia also translated into a decline in export dynamics – Russia fell to 23rd place among Poland's largest export partners in April 2022 from 7th place a year ago. The high import dynamics was driven by 75% higher crude oil prices than a year ago, as well as record high prices of natural gas and coal. Russia was no longer the most important import destination for coal and refined oil products in April, replaced by Australia and Germany respectively.

– China's Zero-Covid policy and local lockdowns in Shanghai make it difficult to defuse tensions in global supply chains. We write about the reaction of Polish companies to disruptions in international trade in our report Poland in Global Supply Chains during Pandemic and War (link: [The report is in Polish, its English version will be available late this week].

Today's data are slightly negative for the zloty, as the deterioration of the external balance indicators continues very quickly, although it is mainly due to external factors – the pandemic and the war. The exchange rate of the zloty remains under the influence of the war in Ukraine and expectations of further NBP interest rate hikes, as well as expectations of an inflow of EU funds from the National Recovery Plan. In the coming months, we expect the current account deficit to widen further to around 5% of GDP by year-end.

Poland's current account and marchandise trade balances, 12-month cumulative, % of GDPING estimates based on NBP data.

Author:Leszek Kasek

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment