403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

Water Purifier Market Size, Share, Growth, Analysis, 2034

| Timeline | Company | Funding/Investment Activity | Funding Value (USD) | Strategic Focus |

|---|---|---|---|---|

| 2025-2026 | Government of India-Jal Jeevan Mission | National infrastructure investment program | USD 50+ billion cumulative allocation | Expansion of rural safe drinking water access, indirectly driving water purifier adoption |

| March 2026 | DrinkPrime | Extended Series A funding round led by Artha Continuum Fund and Mirabilis Investment Trust | USD 2.2 million | Expansion of IoT-enabled subscription-based water purifiers, strengthening AI-driven monitoring, scaling operations to 20 cities |

| November 2025 | Eureka Forbes | R&D and product innovation investment | USD 24 million (₹200 crore R&D+A&SP combined investment scale) | Development of IoT-enabled purifiers, new product launches, and smart water purification systems with increased R&D intensity |

| Market Metric | Details & Data (2025-2034) |

|---|---|

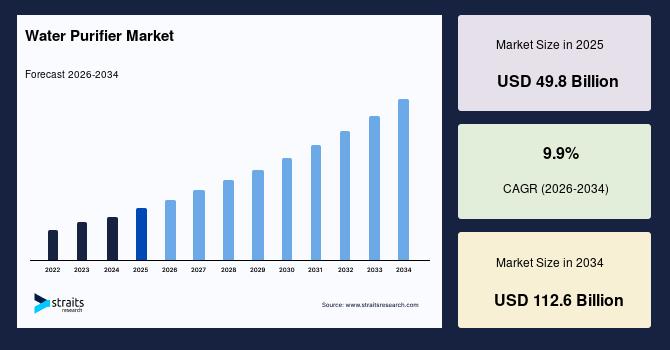

| 2025 Market Valuation | USD 49.8 Billion |

| Estimated 2026 Value | USD 53.1 Billion |

| Projected 2034 Value | USD 112.6 Billion |

| CAGR (2026-2034) | 9.9% |

| Study Period | 2022-2034 |

| Dominant Region | Asia Pacific |

| Fastest Growing Region | Middle East & Africa |

| Key Market Players | A. O. Smith (US), Pentair (US), Culligan International (US), 3M Company (US), BWT Holding GmbH (Austria) |

Download Free Sample Report to Get Detailed Insights.

Water Purifier Market Dynamics Market DriversIntegration of Mineral Rebalancing Post-RO Purification Stages and Increasing Use of Anti-biofilm Internal Tank Coatings Drives Market

Post-treatment mineral restoration is being increasingly embedded into household RO purifier designs as manufacturers respond to the shift toward multi-layered water conditioning rather than only contaminant removal. This is influencing product engineering toward cartridges that reintroduce essential minerals like calcium and magnesium after high-efficiency membrane filtration, improving both taste profile and consumer acceptance of purified water. Stronger demand is emerging for hybrid purification systems that combine RO purification with controlled mineral balancing, particularly in regions dependent on high-TDS groundwater. RO membrane systems are widely documented by the US Environmental Protection Agency to remove around 90 to 99% of dissolved solids, which explains the need for post-treatment mineral correction in finished drinking water systems.

Internal tank design in storage-based purifiers is evolving toward antimicrobial surface engineering. A 2025 study found that stagnant drinking water conditions can significantly increase biofilm growth and promote the proliferation of pathogens and antibiotic resistance genes, encouraging manufacturers to adopt antimicrobial tank linings and silver-ion infused materials. Biofilms can begin forming on untreated water storage container surfaces within 24 hours, while silver-based antimicrobial technologies substantially delay microbial colonization and improve stored water quality.

Market RestraintsHigh Upfront Installation Cost and Space Constraints in Compact Urban Housing Restrain Market

Advanced RO+UV+UF water purification systems require higher initial investment due to multi-stage filtration units, electronic components, and installation charges. This pricing structure increases entry cost for households, especially in price-sensitive segments. It slows down adoption of premium purification systems and pushes consumers toward basic or gravity-based alternatives, particularly in emerging urban and semi-urban markets.

Modern urban apartments often have limited kitchen and utility space, making it difficult to accommodate bulky purifier units with external tanks and multiple filtration stages. This physical limitation restricts installation flexibility and reduces suitability of large systems in compact homes. It shifts consumer preference toward smaller countertop or portable purifiers, limiting penetration of advanced multi-module purification systems in densely populated cities.

Market OpportunitiesIntegration of Water Purifiers with Packaged Real Estate Projects and Expansion of Subscription-based Water-as-a-Service Models Offer Growth Opportunities

A key water purifier market growth opportunity stems from the growing residential construction activity. This is creating opportunities for purifier manufacturers to partner directly with real estate developers and integrate water purification solutions into new housing projects. This provides builders with an additional value proposition while enabling purifier companies to secure large-volume installations at the project stage. For example, Godrej Properties reported sales of over 275 homes worth more than USD 234 million (₹2,000 crore) at the launch of its Godrej Riverine project in Noida in April 2025, illustrating the scale of residential developments where integrated water purification solutions can be deployed from the outset.

Rising preference for flexible, service-oriented appliance consumption is creating opportunities for water purifier providers to move beyond one-time product sales and offer subscription-based access models. This creates growth opportunities for companies offering purifier installation, maintenance, filter replacement, and performance monitoring under recurring payment structures. The model lowers upfront ownership costs for consumers while generating predictable recurring revenue for service providers. Growing adoption of connected appliances and digital service platforms is supporting the expansion of water-as-a-service offerings across urban residential markets.

Market ChallengesIncreasing Proliferation of Counterfeit Filters and Fragmented Regulatory Standards Challenges Water Purifier Market Growth

The growing availability of counterfeit filters and non-certified replacement components is creating quality and performance concerns across the water purifier market. These products often fail to meet filtration specifications, leading to poor purification outcomes and reduced consumer trust in branded systems. This challenge affects aftermarket revenues for legitimate manufacturers and can slow market growth by increasing skepticism toward purifier effectiveness.

Differences in water quality regulations, certification requirements, and testing protocols across countries create complexity for manufacturers operating in multiple markets. Companies often need to modify product designs, compliance documentation, and certification processes for each region, increasing development costs and extending product launch timelines. This limits economies of scale and slows international expansion, particularly for small and mid-sized purifier manufacturers seeking entry into new geographic markets.

Water Purifier Regional Outlook Asia Pacific Water Purifier MarketAsia Pacific: Market Dominance Led by Expansion of Smart City Infrastructure and Increasing Reliance on Advanced Treatment

The Asia Pacific water purifier market accounted for the largest regional share of 41.85% in 2025 due to strong dependence on groundwater sources with varying contamination levels across densely populated urban and rural areas. Rapid urban expansion and rising middle-income households are increasing the need for reliable household water treatment solutions. Frequent variability in municipal water quality is encouraging adoption of multi-stage purification systems in residential and commercial spaces. Expanding real estate development and compact urban housing layouts are also supporting demand for wall-mounted and space-efficient purifiers.

China Water Purifier MarketThe China water purifier market was estimated to be USD 11,850 million in 2025. Rapid industrialization and urban water stress in China are increasing reliance on advanced municipal-to-home purification systems, especially in tier-1 and tier-2 cities. Expansion of smart city infrastructure is pushing integration of IoT-enabled filtration units in residential complexes and commercial buildings. The continued upgrade of urban water treatment infrastructure under China's national water security initiatives, where large-scale municipal systems are being modernized to improve drinking water standards across cities like Shanghai and Beijing.

India Water Purifier MarketThe water purifier market in India was valued at USD 9,400 million in 2025. The market is supported by rapid urban population growth, which is pushing government-led upgrades in municipal water infrastructure to ensure continuous and safe piped water delivery in cities. The AMRUT 2.0 mission, approved by the Government of India with a total outlay of ~USD 29 billion (₹277,000) crore, is targeting universal water supply coverage in 4,378 statutory towns and emphasizing water quality improvement and digital monitoring of supply systems. This strengthens demand for point-of-use purification in urban households where municipal variability persists.

Japan Water Purifier MarketThe Japan water purifier market was estimated to be USD 4,250 million in 2025, shaped by high urban-density housing structures and strong consumer preference for compact, high-efficiency filtration systems. Aging population demographics are also encouraging demand for easy-to-maintain purification devices with low operational complexity. Japan's Ministry of Health, Labour and Welfare maintains stringent drinking water quality standards under the Water Supply Act, encouraging household-level purification for taste and safety enhancement in residential units.

Middle East & Africa Water Purifier MarketMiddle East & Africa: Fastest Growth Driven by Extreme Aridity and Near-total Dependence and Deteriorating Municipal Water Infrastructure

The Middle East & Africa water purifier market is expected to grow at a CAGR of 10.68% during the forecast period due to increasing water scarcity and heavy reliance on desalination and groundwater sources of variable quality. Growing urban development projects and rising population concentration in Gulf cities are increasing demand for advanced purification systems in residential and commercial buildings. The region also shows higher adoption of point-of-use systems as consumers seek additional safety after desalination and municipal treatment.

Saudi Arabia Water Purifier MarketThe water purifier market in Saudi Arabia, which was estimated at USD 2,350 million in 2025, is driven by extreme aridity and near-total dependence on desalinated seawater for municipal supply. The Kingdom is the world's largest producer of desalinated water, with total production exceeding 7.5 million m3/day, forming the backbone of urban water supply systems. This reliance creates demand for household RO and UV purifiers for mineral adjustment and taste correction. The Shuaiba-5 desalination system surpassing 665,000 m3/day output, reinforcing stable but highly processed water supply chains.

UAE Water Purifier MarketThe UAE water purifier market was valued at USD 1,420 million in 2025, driven by near-total reliance on desalinated seawater for municipal supply, making post-treatment purification important for improving taste, mineral balance, and household consumption quality. The country operates large-scale desalination infrastructure managed by government utilities, particularly in Dubai and Abu Dhabi, to ensure continuous potable water availability. Dubai Electricity and Water Authority (DEWA) regularly report expansion and optimization of desalination-linked water production to meet rising urban demand from population growth and tourism activity.

South Africa Water Purifier MarketThe South Africa water purifier market was estimated to be USD 780 million in 2025, driven by deteriorating municipal water infrastructure, intermittent supply, and localized contamination risks in major urban centers. The Department of Water and Sanitation reports persistent strain on water services infrastructure, with aging pipelines and leakage contributing to reliability challenges across metropolitan municipalities such as Johannesburg, Ekurhuleni, and Cape Town. This has increased household reliance on point-of-use filtration systems including RO, activated carbon, and UV purifiers.

Water Purifier Market Segmentation Analysis By TechnologyBy technology, reverse osmosis (RO) systems accounted for the largest market share of 46.85% in 2025 due to their strong capability to remove dissolved salts, heavy metals, and a wide range of chemical contaminants from diverse water sources. Their adaptability to high TDS conditions makes them highly suitable for regions with inconsistent groundwater quality. Continuous improvements in membrane efficiency and integration with UV and UF stages further strengthen their position in the market.

The ultraviolet (UV) purification systems segment is projected to grow at a CAGR of approximately 8.11% during the forecast period due to their chemical-free disinfection capability and low maintenance requirements. These systems are increasingly being adopted in areas with relatively lower dissolved solid content but higher microbial contamination risks.

By Installation TypeBased on installation type, wall-mounted systems accounted for a share of 38.90% in 2025 due to their space-efficient design and suitability for modern kitchen layouts. Their fixed installation ensures stable operation and consistent water supply, making them a preferred choice in urban households. These systems offer a balanced combination of capacity, performance, and ease of maintenance.

The under-sink systems segment is projected to grow at a CAGR of 10.92% during the forecast period due to increasing demand for aesthetic, clutter-free kitchen environments. These systems are concealed within kitchen cabinetry, offering high purification performance without occupying visible counter space. Growing adoption of modular kitchen designs in urban housing is accelerating their demand.

By Distribution ChannelBy distribution channel, offline retail stores accounted for a share of 52.30% in 2025, as consumers prefer physically evaluating water purifiers before purchase. Demonstrations, in-store consultations, and after-sales service assurance play a key role in influencing buying decisions. Established dealer networks and appliance stores provide strong accessibility across urban and semi-urban regions.

The online platforms segment is projected to grow at a CAGR of 11.25% during the forecast period due to increasing digital adoption and convenience-driven purchasing behavior. Consumers are increasingly comparing product features, pricing, and reviews before making purchase decisions through e-commerce channels. Doorstep delivery, easy installation scheduling, and attractive financing options are further accelerating adoption.

By End UserBy end user, residential accounted for a share of 61.41% in 2025 due to widespread household concerns about drinking water quality and safety. Increasing urbanization and dependency on treated or groundwater sources have made home-based purification systems essential. Residential users prefer compact, easy-to-operate systems that ensure continuous access to safe drinking water.

The commercial segment is expected to grow at a CAGR of 8.72% during the forecast period, driven by increasing installation in offices, hospitality establishments, healthcare facilities, and educational institutions. These environments require high-capacity and continuous water purification systems to serve large user bases. Rising focus on hygiene standards and workplace health safety is accelerating adoption.

Competitive LandscapeThe water purifier market competitive landscape is moderately fragmented, with a mix of global water treatment corporations, established home appliance brands, regional filtration manufacturers, and emerging private-label and direct-to-consumer purifier brands. Large players compete through strong product reliability, advanced multi-stage filtration technologies such as RO, UV, and UF integration, established distribution networks, certified water safety compliance, and long-term service and maintenance ecosystems. Emerging players in the water purifier market ecosystem focus on cost-effective systems, compact and portable purifier designs, rapid customization for urban households, and aggressive digital-first marketing strategies targeting price-sensitive and first-time buyers.

List of Key and Emerging Players in Water Purifier Market-

A. O. Smith (US)

Pentair (US)

Culligan International (US)

3M Company (US)

BWT Holding GmbH (Austria)

Brita (The Clorox Company) (US)

Coway Co., Ltd. (South Korea)

LG Electronics (South Korea)

Samsung Electronics (South Korea)

Panasonic Corporation (Japan)

Kent RO Systems Ltd. (India)

Eureka Forbes Ltd. (India)

Blue Star Limited (India)

Whirlpool Corporation (US)

Veolia Water Technologies (France)

January 2026: V-Guard launched its upgraded Rejive RO water purifier series with enhanced 40% water recovery efficiency, BIS compliance, and improved durability features targeting high TDS water conditions across residential markets.

December 2025: Livpure launched its new 2X Power Filter water purifier series designed to extend filter life up to two years, significantly reducing maintenance cost and improving long-term affordability for residential consumers in high-contamination regions.

Report Scope| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 49.8 Billion |

| Market Size in 2026 | USD 53.1 Billion |

| Market Size in 2034 | USD 112.6 Billion |

| CAGR | 9.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Technology, By Installation Type, By Distribution Channel, By End User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

Water Purifier Market Segments By Technology-

Reverse Osmosis (RO) Systems

Ultraviolet (UV) Purification Systems

Ultrafiltration (UF) Systems

Gravity Based Purifiers

Activated Carbon Filtration Systems

-

Wall Mounted Systems

Countertop Systems

Under Sink Systems

Faucet Integrated Systems

Portable Purifiers

-

Offline Retail Stores

Direct Institutional Sales

Online Platforms

-

Residential

Commercial

Industrial

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment