403

Sorry!!

Error! We're sorry, but the page you were looking for doesn't exist.

3D Metrology Market Size, Top Share, Demand Industry Report, 2034

| Market Metric | Details & Data (2025-2034) |

|---|---|

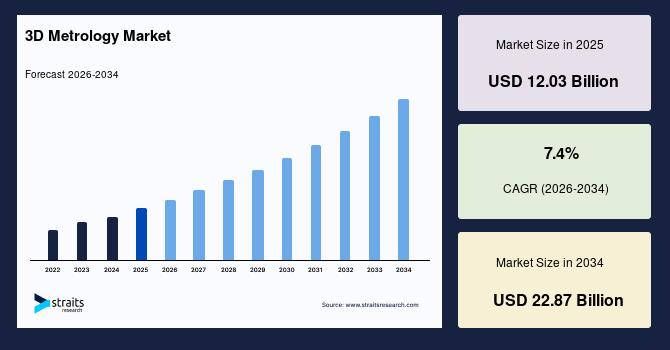

| 2025 Market Valuation | USD 12.03 Billion |

| Estimated 2026 Value | USD 12.92 Billion |

| Projected 2034 Value | USD 22.87 Billion |

| CAGR (2026-2034) | 7.4% |

| Dominant Region | North America |

| Fastest Growing Region | Asia Pacific |

| Key Market Players | 3D Systems Inc, Zeiss International, FARO Technologies Inc, Hexagon AB, Nikon Corporation |

Download Free Sample Report to Get Detailed Insights.

3D Metrology Market Trends The Market is Shifting From Device Sales To Quality EcosystemsVendors are increasingly bundling scanners, CMMs, CT systems, analytics, training, and support into integrated software-driven environments. As a result, the commercial focus is shifting from standalone hardware to end-to-end workflows that connect data capture, analysis, collaboration, and lifecycle service delivery.

Recurring Revenue is Entering a Historically Capex-led CategoryThe adoption of cloud platforms, subscription models, and tokenized services is transforming how metrology solutions are procured and scaled. This shift enables vendors to generate recurring revenue through software usage, collaboration tools, and remote processing, reducing dependence on cyclical hardware sales.

Shift Toward In-line and Process-integrated MetrologyThe industry is moving beyond incremental improvements in measurement accuracy toward embedding metrology directly into production environments. Increasingly, customers prioritize systems that enable real-time defect prevention and process control over those limited to post-production inspection.

Service-led Adoption Models Lowering Entry BarriersOrganizations are increasingly engaging through application consulting, outsourced CT services, programming support, and system integration before investing in full-scale equipment. This service-first approach is broadening market access by reducing technical complexity and upfront investment barriers.

3D Metrology Market Drivers Yield Protection is Emerging As A Strategic PriorityIn batteries, electronics, and precision assemblies, metrology investment is increasingly driven by the cost of escaped defects rather than the cost of measurement itself. Technologies such as industrial CT and integrated inspection systems are gaining prominence, as internal defects, alignment issues, and structural inconsistencies can significantly impact downstream yield and overall production efficiency.

Production Ramp-ups are Exposing Measurement BottlenecksAircraft, EV, and advanced manufacturing programs are scaling output while maintaining stringent quality requirements. As production volumes increase, metrology is transitioning from a laboratory function to a critical production constraint, driving investments in high-throughput inspection solutions to sustain first-pass quality during ramp-up phases.

Supplier Qualification is Becoming More Measurement-intensiveOEMs are extending dimensional accountability across multi-tier supplier networks, particularly in complex sourcing environments. This shifts 3D metrology demand beyond primary manufacturing sites into toolrooms, contract manufacturers, and supplier quality operations that require faster first-article inspection and deviation approval cycles.

Regulated Manufacturing is Increasing The Cost of Undocumented VariationIn medical devices and other compliance-driven industries, measurement data is becoming essential not only for conformance but also for auditability and process control. As regulatory frameworks increasingly align with standards such as ISO 13485 and oversight from US Food and Drug Administration, the importance of traceable and well-documented dimensional data continues to rise.

3D Metrology Market Opportunities Build Supplier-quality Platforms for Mid-tier ManufacturersA significant gap exists between enterprise-grade metrology systems and basic measurement tools. Vendors that provide simplified first-article inspection, digital approval workflows, and seamless OEM–supplier data exchange tailored for smaller facilities can unlock a large, underpenetrated segment.

Examples: Companies like Hexagon AB (e.g., cloud-based quality platforms) and Autodesk (Fusion ecosystem with inspection workflows) are enabling more accessible, digitally connected quality systems for distributed manufacturing environments.

Own the Battery Inspection Stack Before Standards HardenBattery manufacturing remains an evolving space with unmet needs in high-speed internal defect detection, electrode alignment, and failure analysis. Companies that integrate CT, analytics, and production workflows early can establish strong positioning and influence process standards in this defect-sensitive segment.

Examples: ZEISS Group and Nikon Corporation are actively advancing industrial CT solutions for battery inspection, while players like Tesla are pushing in-house quality and inspection capabilities for battery production.

Manufacturing environments typically operate with multi-brand metrology systems, creating fragmentation in data and workflows. Platforms that unify data across CMM, optical scanning, CT, and SPC systems can establish themselves as central control layers, driving recurring software value regardless of hardware mix.

Examples: Hexagon AB (Nexus platform) and Siemens AG (Teamcenter and digital thread solutions) are building interoperability layers that integrate multi-source inspection data across production ecosystems.

Expand Metrology-as-a-service For Capex-constrained BuyersMany manufacturers require advanced inspection capabilities primarily during product launches, validation phases, or root-cause investigations. Flexible service models, including on-demand inspection, rental access, and batch-based analysis, can capture demand that may not justify full-scale capital investment.

Examples: ZEISS Group and SGS SA offer contract measurement and CT inspection services, while Element Materials Technology provides outsourced testing and validation solutions for complex components.

While the value of metrology is clear from an engineering perspective, it is often difficult to quantify in financial terms. Benefits such as avoided scrap, reduced recalls, and faster product approvals are real but not always directly reflected in procurement metrics, slowing investment decisions for advanced systems with integrated software and automation.

Workflow Complexity Still Limits Scaled DeploymentThe primary challenge lies not in acquiring individual systems but in standardizing data formats, inspection methodologies, training, and response protocols across sites. Without a cohesive operating model, organizations struggle to fully utilize metrology investments or translate measurement data into closed-loop process improvements.

High-end Use Cases Remain Bottlenecked By Speed And SkillsAdvanced applications such as inline CT, automated inspection programming, and multi-sensor data analysis require both specialized expertise and acceptable cycle times. In many cases, technical capabilities outpace organizational readiness, limiting widespread deployment in production environments.

Market Evolution Is Constrained By Operational And Structural BarriersThe 3D metrology market is evolving beyond precision measurement toward a broader role in yield optimization, supplier control, and digital quality workflows. However, adoption is moderated by organizational inertia, integration challenges, and the difficulty of transitioning from episodic measurement investments to continuous, software-driven quality infrastructure.

Regional Analysis North America Dominates The 3d Metrology MarketNorth America is the largest shareholder in the global 3D metrology market, accounting for a 22% share in 2025. The region is mainly driven by the strong presence of automotive, aerospace, and pharmaceutical OEMs, especially in the U.S. In addition, the adoption of advanced technology in aerospace and defense, as well as in the industrial sector in the United States and Canada, is likely to fuel market growth in North America. Rapid mechanization of automotive production facilities is one of the crucial factors behind the rising demand for inline dimensional metrology systems. Additionally, due to the growth of data centers and the rollout of the 5G network in the region, North America now holds a monopoly on the 3D metrology market. Several Body-In-White (BIW) and powertrain manufacturers might replace conventional measurement solutions, such as CMMs, with inline metrology solutions.

Asia Pacific: Fastest Growing RegionAsia Pacific is expected to grow at a CAGR of 9.10% over the forecast period. The Asia-Pacific region is expected to remain the most lucrative market for 3D metrology over the forecast period. The growth is mainly driven by growing automotive production across emerging countries, such as China and India. The rising deployment of metrology solutions in the construction and engineering and medical industries, especially in emerging economies within the region, is driving the market demand over the forecast period. The Asia-Pacific region is the most industrialized products manufacturing and engineering hub. Furthermore, China is prominent in manufacturing output products, including steel, iron, chemical, consumer product, food processing, transportation, and equipment manufacturing. Therefore, 3D metrology is used in power generation and diverse industrial applications, such as raw casting, forging inspection, die and mold design, and scrutinizing power generation machinery.

Europe is expanding rapidly due to the region's considerable use of the automotive and aerospace sectors, and this tendency is expected to continue over the forecasted period. The existence of extensive production facilities in Europe is anticipated to accelerate the industry's expansion in the coming years. Germany is expected to dominate the regional market over the forecast period due to the sizeable manufacturing facilities there. Furthermore, France is also growing at a considerable rate in Europe as a result of the country's significant aerospace and automotive industries.

In the Middle East and Africa and South America, the market growth is moderate due to the delayed adoption of advanced metrology technology and the shortage of skilled professionals necessary to operate Video Measuring Machines (VMM) and Coordinate Measuring Machines (CMM).

Based on ComponentsThe hardware segment accounted for 45.00% of the market revenue in 2025. 3D metrology hardware is used to test and analyze the performance of a machine to scan its strengths and weaknesses depending on the objects to be scanned. The increasing embracing of 3D metrology equipment by numerous industries, such as automotive, aerospace, heavy machinery, construction and engineering, and energy and power to uphold the quality of the product is the foremost driver for the growth of the hardware segment. In addition, the hardware segment is further subdivided into a Coordinate Measuring Machine (CMM), 3D Automated Optical Inspection System (AoI), Video Measuring Machine (VMM), and Optical Digitizer and Scanner (ODS). The growing demand for CMM also drives the growth of the hardware segment in the 3D metrology market.

The software segment is projected to grow at a CAGR of 7.80% during the forecast period. Therefore, it gives comprehensive and self-explanatory textual and graphical reports that distinguish production tendencies and assess real-time deviations. Furthermore, the applications of CAM/CAD software for manufacturing and designing processes include production engineering, tooling, metal fabrication, sheet metal, stone, and woodworking. It results in attaining production efficiencies and value enhancement to the process, which, consecutively, has driven the demand for software applications. Inspection of certain minute parts of a machine requires high accuracy, which metrology software achieves.

Based on ApplicationThe reverse engineering segment owns the highest market and is estimated to grow at a CAGR of 7.60% over the forecast period. Reverse engineering is a method of creating a 3D virtual model from an existing physical part for use in 3D computer-aided design (CAD), computer-aided manufacturing (CAM), computer-aided engineering (CAE), or other software. The process involves measuring an object and then reconstructing it as a 3D model. Reverse engineering helps analyze product functionality and subcomponents, estimate costs, and identify potential patent infringement. The surge in demand for smart reverse engineering solutions with the convention of CAD model or by assessment of the archetype of the CAD model, essentially in the automobile industry, has also transformed the application setup of the metrology system.

Quality inspection is a measure aimed at checking, measuring, or testing one or more product characteristics and relating the results to the requirements to confirm compliance. This task is usually performed by specialized personnel and falls outside the responsibility of production workers. In addition, products that comply with the specifications are not accepted or returned for improvement. The trend certification of standardization laboratories by A2LA is critical for the endowment of quality service to temporary customer assurance. Moreover, manufacturers are implementing globally recognized quality standards and guidelines, such as ISO-9001, QS-9000, and Six Sigma, to meet the necessities of international clients. Hence, the quality control and inspection segment will record the highest growth over the forecast period.

Based on the End-UserThe automotive segment is the highest contributor to the market and is projected to grow at a CAGR of 6.90% during the forecast period. The automotive industry has always led most other industries in implementing new advanced manufacturing technology due to ever-shortening product life cycle times. One technology critical to delivering quality automotive products, with the necessitated increasing of productivity and lowering of costs, is 3D metrology. Component precision within the automotive industry is imperative. In addition, as quality standards rapidly rise, so does the need for equipment that allows our customers to verify component accuracy and increase throughput. The growth in the demand for fuel-efficient transport and high-end vehicles is expected to propel the demand for 3D metrology solutions over the forecast period.

In healthcare systems worldwide, measuring medical equipment is frequently utilized for illness prevention, diagnosis, and treatment. The safety and accuracy of these devices' measures are a growing discussion area because they are crucial to medical professionals' day-to-day operations and how their measurements affect patients' health. Medical devices must pass tests for metrological safety assessment and control under the Medical Devices Act. It enables a high degree of accuracy in implants, prostheses, dental applications, and critical assemblies of medical devices, such as CT scanning and X-ray machines that need access to hard-to-reach spots, thereby driving the market growth.

List of Key and Emerging Players in 3D Metrology Market 3D Systems Inc Zeiss International FARO Technologies Inc Hexagon AB Nikon Corporation KLA Corporation Keyence Corporation Perceptron Inc Automated Precision Inc Applied Materials Recent Developments-

In April 2026, Transcat, Inc. completed the acquisition of SCM Metrology and Laboratories S.A. (Costa Rica), marking its first operational entry into Latin America and strengthening its regional calibration and metrology service capabilities to support multinational customers.

In September 2025, FARO partnered with Autodesk to integrate 3D measurement data directly into design and digital twin workflows, improving interoperability between scanning and CAD environments.

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.03 Billion |

| Market Size in 2026 | USD 12.92 Billion |

| Market Size in 2034 | USD 22.87 Billion |

| CAGR | 7.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, Environment & Regulatory Landscape and Trends |

| Segments Covered | By Component, By Applications, By End-User |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, UK, Germany, France, Spain, Italy, Russia, Nordic, Benelux, China, Korea, Japan, India, Australia, Taiwan, South East Asia, UAE, Turkey, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Mexico, Argentina, Chile, Colombia |

Download Free Sample Report to Get Detailed Insights.

3D Metrology Market Segments By Component-

Hardware

Software

Services

-

Quality Assurance and Inspection

Reverse Engineering

Virtual Simulation

3D Scanning

-

Aerospace

Automotive

Medical

Construction and Engineering

Heavy Machinery

Others

-

North America

Europe

APAC

Middle East and Africa

LATAM

Legal Disclaimer:

MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Most popular stories

Market Research

More Story

Comments

No comment