(MENAFN- ING) 25bp hike, but we are close to the peak

The Federal Reserve has hiked the fed funds target rate range 25bp to 4.75-5% as largely expected by the markets and economists. This was a unanimous decision with the committee backing the view that“some additional policy firming may be appropriate". This is a slight language shift having previously said that“ongoing increases in the target range will be appropriate” (our emphasis).

Their dot plot chart shows that their end-2023 Fed funds median forecast is 5.1%, which is the same as it was in December, whereas surveys of economists suggested an expectation they would have raised that to 5.4%. So again it does appear to be a little more dovish than expected.

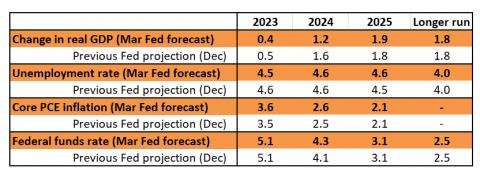

Federal Reserve economic projections

Federal Reserve, ING

Nonetheless, the Fed appears quietly confident the economy won't be heavily disrupted by recent banking sector woes. It

argues that the“US banking system is sound and resilient” so their fourth quarter year-on-year

GDP forecast for 2023 has only been cut from 0.5% to 0.4% while 2024 is now 1.2% versus 1.6% expected three

months ago. The unemployment and inflation expectations are little changed. Moreover, the Fed

are now looking for only 75bp of rate cuts in 2024 rather than 100bp of cuts that it

had projected back in December. Chair Powell used

the press conference to separate the Fed's price stabilty role and financial

stability role, saying that it has

the tools to deal with both, echoing comments from the ECB's Christine Lagarde last week.

We are more nervous about the economic threat from the banking stresses

We are a little more pessimistic, having been on the more dovish end of expectations for interest rate

moves in 2023 for quite some time. Our concern was that this has been the most aggressive monetary policy tightening cycle for 40 years and by going harder and faster into restrictive territory you naturally have less control over the outcome. This heightens the chances of economic and financial stress and that is what we have seen over the past couple of weeks.

Even before the recent banking woes borrowing costs have been rising rapidly, but significantly, the economy has also experienced a tightening in lending conditions, which we felt would increasingly weigh on credit flow to the detriment of economic growth.

It's our view that the recent events will make banks more nervous about who they lend to, how much they lend and at what interest rate. With regulators also likely sensing a need to

be more proactive, this could intensify risk aversion and make banks tighten lending standards even more. This will hamper credit flows, weigh on the economy and allows inflation to fall even more quickly. The Fed does acknowledge this stating“recent developments are likely to result in tighter credit conditions... and to weigh on economic activity, hiring and inflation”. We are therefore a little confused as to why it

didn't adjust their economic projections more than it

did, although Chair Powell did acknowledge that it is difficult for them to assess the impact of recent events because they are indeed so recent and added that a "pathway still exists" for a soft landing, but recent events don't make this more likely.

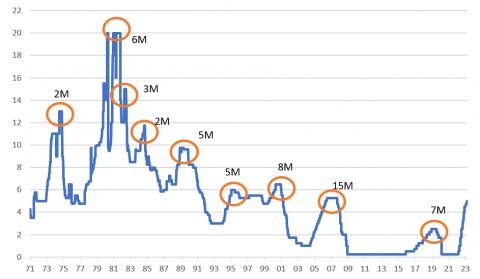

The Federal Reserve never leaves it long between the last hike in a cycle and the first rate cut

Macrobond, ING

Rate cuts in the second half 2023 remains our call

Just over two weeks ago the expectation was that the Fed could be looking to get the Fed funds rate up to 5.5-5.75%, with some commentators talking about 6%. Markets are now barely pricing one further rate rise (around 15bp at the May meeting currently) and are looking for cuts later this year (somewhere between 50bp and 75bp from the peak).

We agree that we could get one final 25bp hike in May, leaving the Fed funds range at 5-5.25%. But higher borrowing costs and reduced access to credit mean

a greater chance of a hard landing for the economy. Rate cuts, which we have long predicted, are likely to be the key theme for the second half of 2023 and we are favouring 75bp of easing in the fourth quarter of this year. As the chart above shows, it is important to remember the Fed never leaves it long between hiking and cutting rates. Historically it has been just six

months between the last hike and the first rate cut.

The Fed lets its facilities do their work, betting for resumed status quo, and system stability

The impact effect has been for lower market rates, in particular on the front end as the market takes on board as Fed that seems to be almost done. On theme that we think continues is the dis-inversion of the curve, and we've seen

another material move in that direction as a response to the Fed's decision.

Market rates had been edging higher as we headed into the Federal Open Market Committee

meeting, which no doubt helped to embolden the Fed to deliver the 25bp hike that the market had (practically) discounted. The market will also be comforted by the fact that the Fed decided to go ahead and hike, when the alternative could have been to hold and nod towards bank angst as the rationale. There is enough in that combination for market rates to re-nudge higher in the weeks ahead, at least till we get to a point where the disinflation story has become more compelling, notwithstanding the impact effect towards lower market rates.

Market technicals are in an interesting place right now. The Fed's balance sheet increased by US$140bn last week as a consequence of support being provided to some banks, including Silicon Valley Bank, Signature Bank and First Republic Bank. And indeed the regional Fed breakout of support confirms that the bulk of additional liquidity went through the New York Fed and the San Francisco Fed.

The consequence of this from a balance sheet perspective is to push against the quantitative tightening policy where US$95bn is being allowed to roll off from the Fed's bond holdings on a monthly basis. This, the Fed argues, is the various mechanisms doing their work. The same logic obtains for the reverse facility, which continued to act to mop up excess liquidity, and has popped higher in the past week in part reflection of that. No new angle on this from the Fed today.

Dollar to come under more pressure

Looking at the negative dollar reaction after the announcement, the FX market had clearly anticipated a good deal of the rate hike, leaving the

surprise being driven almost entirely by the new dot plot projections. With markets perceiving the unchanged 2023 median projections at 5.1% as moderately dovish and the general investors' sentiment on the banking crisis having gradually improved in the past couple of days, the dollar was left without a floor.

Before the Fed meeting, we had flagged risks of a small EUR/USD correction on a potential hawkish surprise, but the road for a break above 1.0800 appeared paved barring another major shock to the banking sector. The next key handle for EUR/USD is 1.1000: that is an important benchmark level that may see some significant resistance unless markets feel substantially confident the worst of the banking shock – especially in Europe – is past us.

But even if the Fed has pushed ahead with tightening today, its rhetoric compared to the ECB is appearing more dovish, particularly when it comes to rate cuts. All this points to a supported EUR/USD in the remainder of this year and we target 1.15 in the second half of 2023.