(MENAFN- ING) Poland: end of the cycle

NBP rate in December (6.75% - unchanged)

The Polish Monetary Policy Council officially declared a pause in its rate hiking

though in practice, this is the end of the cycle. With CPI inflation moderating from 17.9% year-on-year

in October to 17.4% YoY in November (flash estimate) and GDP growth

pointing to

weak

household

spending

and fixed investment, the Council is unlikely to tighten further anytime soon. Policymakers will wait for the impact of rate hikes delivered so far and hope that further tightening by central banks in core markets, along with a

global economic slowdown, will bring

Polish inflation down. However, the National Bank of Poland's

target of 2.5% (+/- 1 perc. point.) is not in sight over the medium term.

Turkey: risks are still on the upside

In November, we expect annual inflation to change direction and drop to 84.4% (2.9% on monthly basis) from 85.5% a month ago, as base effects start to

kick

in. These will become

more pronounced in December and early next year. Stability in the currency is another factor for some moderation in the pace of increase lately. However, the risks lie to

the upside given the deterioration in pricing behaviour and still prevailing cost-push pressures.

Hungary: year-on-year indices of inflation rise further

October economic activity data is due next week in Hungary. We expect the retail sector to post a slowdown in sales volume, as household

purchasing power is increasingly hit by rising inflation. Business survey indicators, including the PMI, suggest that we might also see a

temporary slowdown in industrial production in October,

after a surprisingly strong September. The next big thing however is the November inflation print. We see food prices

rising further as domestic producer prices are skyrocketing in the food industry (close to 50% YoY). Still, the strengthening of the forint may ease some pressure on

imported inflation,

and as

aggregate demand retreats, inflation in

services could

also slow down. In all, we see the month-on-month headline inflation rate at around 1.8% and core inflation at 1.7%. But these rates are still higher than last year's figures

from the same month, thus the year-on-year indices are going to rise further, with the headline and core rates surpassing

22% and 23%,

respectively. When it comes to the budgetary situation, unlike in the previous two months, we see a monthly deficit. This is fuelled by the extra pension adjustment by law due to high inflation. This payment triggered a significant outflow of cash in November, pushing the monthly budget balance into negative territory despite rising revenues from

high inflation and windfall taxes, in our view.

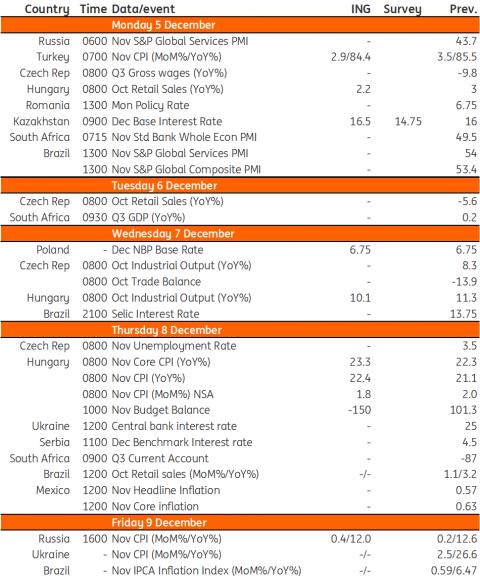

Key events in EMEA next week

Refinitiv, ING

MENAFN02122022000222011065ID1105261268

Author:

Adam Antoniak , Muhammet Mercan, Peter Virovacz

*Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/about/disclaimer/

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.