(MENAFN- ING) Another 50bp hike, but hints of a slower pace of tightening

Norges Bank delivered another much-anticipated 50bp rate hike today, bringing the policy rate to 2.25%. The move was fully in line with the Bank's determination to fight elevated inflation, as firmly reiterated by Governor Ida Wolden Bache in her post-meeting statement.

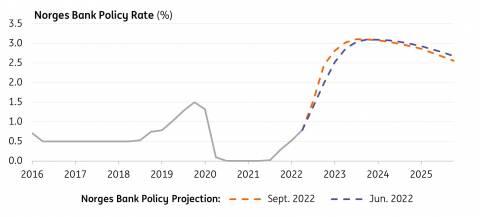

The Bank also released its updated economic and policy rate projections. While the inflation forecast was revised higher, the rate path was nearly unchanged from the June 2022 projections, with a peak expected at 3% in 2023 and remaining around that level into 2024.

Perhaps surprisingly, the Bank explicitly mentioned that“monetary policy is starting to have a tightening effect on the Norwegian economy”, which“may suggest a more gradual approach to policy rate setting ahead”. This appears in contrast with other developed central banks which are refraining from diverging from their hawkish rhetoric with the aim of keeping inflation expectations in check.

There are two more Norges Bank meetings in 2022, on 3 November and 15 December. Today's statement suggests that to get to the 3.0% projected terminal rate (so 75bp from the current level) with more gradual tightening, we could see 25bp hikes in November, December, and at the first meeting of 2023.

Rate projections unchanged since June

Norges Bank, ING

We don't rule out a 50bp move in November

We had previously forecasted another 50bp hike in November, although the change in tone by Norges Bank does suggest a 25bp move is likely the baseline scenario for the Bank.

Still, we would not rule out a half-point move just yet, mainly because for one thing, the statement still points to some flexibility in the rate setting moving forward. Also, inflation may surprise to the upside, and Norges Bank may attempt to lift the krone by surprising markets on the hawkish side.

NOK: Monetary policy impact very limited

In her statement today, Governor Bache said:“a higher policy rate may also contribute to strengthening the krone exchange rate, which may curb imported goods inflation further out”. In practice, however, the correlation between short-term rate differentials (which absorb monetary policy expectations) and the krone's performance has faded in recent months as it has in many other developed currencies. The example of the neighbouring Riksbank in Sweden is emblematic; earlier this week, a massive 100bp rate hike only seemed to offer an opportunity for SEK bears to sell the currency at more attractive levels, and SEK plunged in the hours after the announcement.

The reason the correlation has faded is down to the numerous global and European macro factors along with geopolitical concerns and their impact on global risk sentiment as FX drivers. We think the unstable risk environment should continue to prevent a relinking of high-beta currencies with their rate differentials in the coming weeks.

We still see room for a recovery in NOK in the medium term, potentially starting later this year, and any risk stabilisation should allow the krone to benefit from the attractive commodity picture and high interest rates. We currently forecast a move to 9.80 in EUR/NOK in the first quarter of next year. However, downside risks in the near term remain elevated for NOK, especially considering its relatively low liquidity character which leaves it more exposed to swings in risk sentiment.

MENAFN22092022000222011065ID1104909957

Author:

Francesco Pesole

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.