(MENAFN- ING) Last week cost the CNB around EUR2.2bn

The CNB's policy meeting last week marked another milestone for the FX intervention regime and with the first data available, it is time to look again at the overall costs and implications for the months ahead. The CNB yesterday published official figures for June showing that FX reserves sold increased to EUR7.1bn from EUR3.5bn in May, above our estimates. However, more interesting will be the figure for July, when CEE currencies underwent a massive sell-off. According to our estimates, FX reserve sales rose to EUR10.8bn last month.

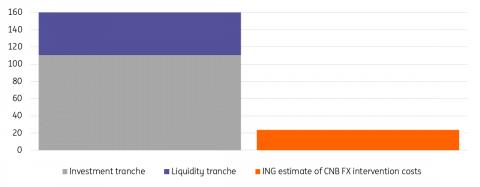

On the other hand, when the CNB left rates unchanged last week, and disappointed market expectations, the central bank sold around EUR2.2bn. Overall, we thus see the cost of FX intervention from mid-May to the end of last week at around EUR23.6bn, representing almost 15% of all FX reserves held by the CNB at the end of April.

Weekly cost of FX intervention (EURbn)

Macrobond, ING calculation

CNB has tamed the markets but hasn't won yet

The last CNB meeting made it clear that an early end to FX intervention is not on the table. Compared to the previous meeting, the commitment to prevent 'any excessive fluctuations in the exchange rate of the koruna' was included in the announcement of the Board's decision. Although we did not take away anything really new from the meeting regarding the CNB's approach to FX intervention, it is clear to us that the new board is more open to using FX reserves and, moreover, in a situation where it no longer wants to hike interest rates further, this seems like the only option.

Based on the cost of FX intervention in recent weeks, it seems that markets have become comfortable with the CNB's presence in the market and for now do not want to test the central bank's commitment to defend the koruna. As we mentioned earlier, we think the current situation is not about the domestic economy and the CNB, but about global developments. The markets have accepted that another rate hike by the central bank is unlikely and the latest inflation number makes this decision easier. We have already seen short CZK positions liquidated several times, which has discouraged the market from attacking the central bank further for now. Thus, at least until the next inflation number in the first half of September, the CNB can rest easy unless another EM sell-off comes into play, which is not our baseline view.

Size of CNB FX reserves in April and costs of intervention since mid-May (EURbn)

Macrobond, ING estimate

MENAFN10082022000222011065ID1104678592

Author:

Frantisek Taborsky

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.