(MENAFN- ING) Poland: July CPI in focus

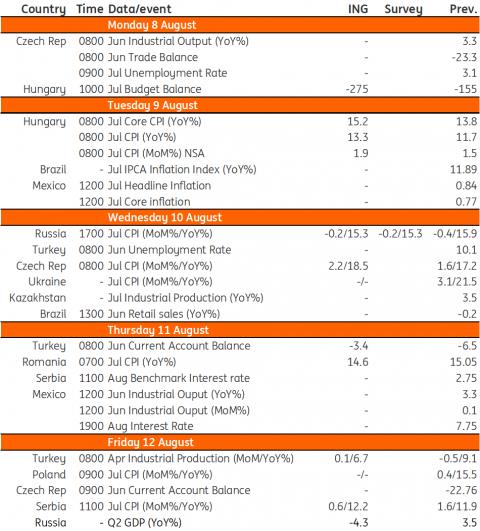

The final CPI reading is unlikely to differ markedly from the flash estimate of 15.5% YoY. However, given that gas prices at the pump continued to decline in the final week of July, we do not rule out a downward revision to 15.4% YoY (our initial forecast). We expect the summer months to be marked by relatively stable, albeit very high, inflation. Inflationary pressure is projected to re-emerge with the beginning of the heating season in autumn and at the beginning of 2023 due to the upswing in regulated prices.

Czech Republic: Energy prices show their full power

Announced price hikes by the country's major suppliers in July should be the main driver of inflation over the coming months. Although the direction is certain, the impact is difficult to calculate due to the uneven pass-through of energy prices into the CPI, based on the different proportions of fixed and floating contracts. Food prices may see a month-on-month decline (1.6%) for the first time since last October. Fuel prices should also counteract the rise in energy prices with a 0.3% MoM decline. Overall, we expect prices to jump by 2.2% MoM and 18.5% YoY in July.

In the longer term, August and September should bring another massive hike in energy prices, which should push the peak in inflation to around 20.0% YoY in September. However, with energy prices gradually being written into the CPI, we should stay around this level until the end of the year with another price spike to be expected in January amid a seasonal repricing.

Hungary: Inflation is expected to accelerate both in monthly and annual terms

Next week's highlight is the July CPI reading in Hungary. There is a high degree of uncertainty surrounding the forecast, but one thing is clear: inflation is expected to accelerate both in monthly and yearly terms. Based on industrial and agricultural producer prices, we expect further strengthening in food and durables inflation. On top of that, EUR/HUF moved to a record high during July, possibly adding further pressure to price increases. The proverbial icing on the cake is the tax change which came into effect from 1 July, raising the excise duty and the so-called public health product tax. These mainly impact prices of tobacco, alcoholic beverages and processed foods. We expect a close to 2% month-on-month inflation with the yearly index moving up above 13%, while year-on-year core inflation will jump through the 15% threshold. Though rising inflation is a pain for households, it is a gain for the budget (via increased revenues). On the other hand, the one-off pension correction (since the value of pensions must be maintained in real terms by law) will push the monthly deficit higher than usual in July.

EMEA Economic Calendar

Refinitiv, ING

MENAFN05082022000222011065ID1104653438

Author:

Adam Antoniak , Frantisek Taborsky, Peter Virovacz

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.