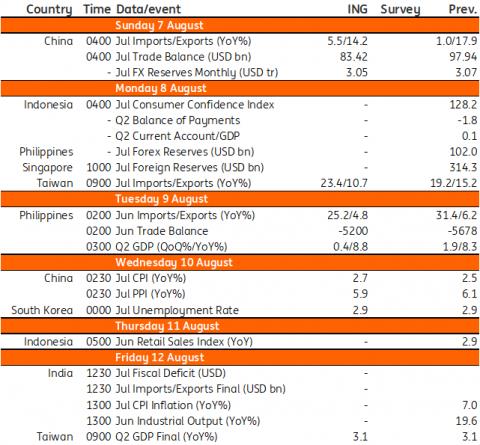

(MENAFN- ING) Trade reports from the region

China exports likely expanded by around 15% year-on-year in July as shipments for the winter holiday season were sent out in advance to avoid port congestion issues. Imports on the other hand should pick up moderately as domestic consumption recovers.

Meanwhile, Taiwan's trade figures are also expected to expand but weakness in industrial production points to a possible slowdown in growth in the coming months.

Philippine trade data is also scheduled for next week and we are likely to see recent trends hold. Exports should post modest gains while imports are likely to record another strong double-digit rise due to bloated energy imports. The trade balance will likely widen to $5bn which points to renewed depreciation pressure for the peso.

China inflation release, bucking the regional trend

Unlike the sharp acceleration in prices for the region, CPI inflation is expected rise gently in China while PPI inflation could slow to 5%YoY from 6% in July as raw material prices fell on slower real estate construction activity.

Philippine 2Q GDP to sustain recent momentum

Also on deck for next week is the Philippine second-quarter GDP report. Election-related spending will likely boost growth to 8.8%YoY with household consumption getting an extra lift after mobility curbs were relaxed in March. Improved growth prospects coupled with above-target inflation point to Bangko Sentral ng Pilipinas staying hawkish for the rest of the year.

Other key reports out next week: China loan growth and Korea's labour data

Other important data scheduled for release in the coming days are China's bank lending numbers and Korea's labour report.

China releases monetary data sometime next week and we expect a more moderate pickup in loan growth for July. This would be a slowdown from the jump in June as the People's Bank of China tightened liquidity after mid-July.

Meanwhile, Korea's labour report is expected to show the sector's resilience with the unemployment rate staying below 3%, delivered largely by the services sector. With the summer season starting in late July, job creation for leisure and hospitality is likely to increase and support service sector employment further.

Asia Economic Calendar

Refinitiv, ING

MENAFN04082022000222011065ID1104647817

Author:

Iris Pang , Nicholas Mapa, Min Joo Kang

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.