(MENAFN- ING)

The corporate bond market will be the first to feel an impact in due course. However, other bond asset classes, such as preferred senior and covered bonds, will unlikely remain observing bystanders as the ECB moves forward on its climate roadmap. That said, Monday's announcements did still lack the detail needed to trigger any performance implications in the near term.

Tilting corporate sector purchases

This week, the ECB announced that as of October it will begin to decarbonise its corporate bond holdings by tilting towards environmental, social, and corporate governance (ESG) via its reinvestments of the corporate sector purchase programme (CSPP). The ECB aims to focus on issuers with better climate performance. As the central bank proclaims: “Better climate performance will be measured with reference to lower greenhouse gas emissions, more ambitious carbon reduction targets and better climate-related disclosures.” For now, this does remain rather ambiguous and prompts the questions:

- What specific metrics will the bank use?

- Will it focus on/omit any specific sectors?

- To what extent will the holdings be tilted towards ESG?

Reinvestments pick up to €2-4bn per month from January onwards

Now that CSPP has officially ended net purchases, the ECB will rely on just reinvestments to make this tilt. Reinvestments are specifically very low in the second half of this year, with average monthly reinvestments for October, November and December at just a little more than €1bn. Although, reinvestments do pick up in January 2023 onwards, with an average of €2-4bn per month.

Actual and projected CSPP (& PEPP) net purchases and reinvestments

ING, ECB

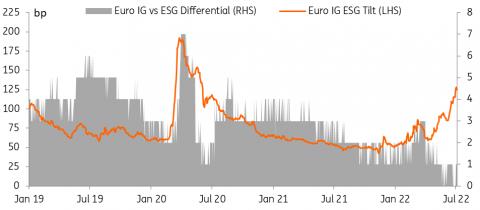

Little ESG outperformance so far this year

As it stands, ESG is not seeing any outperformance in secondary markets. As shown below, there is very little differential between the ESG tilted index and the overall index.

EUR IG ESG Tilted index vs overall EUR IG Non-financial index

ING, ICE

Similarly, demand for ESG bonds in the primary market has slipped. The oversubscription levels this year have been very much in line for ESG bonds and sustainably-linked bonds (SLBs) compared to vanilla bonds. The new issuer premium levels are actually showing higher new issue premiums (NIPs) for ESG and SLBs, however this is distorted due to more higher beta (BBB rated) corporates bringing more ESG bonds to the market this year.

ESG not outperforming in primary

ING

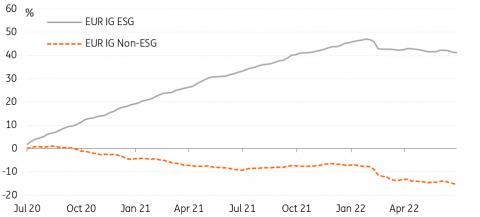

Nonetheless, fund flows have been substantially positive for ESG funds over the past couple of years, as demand for ESG is insatiable. Naturally, ESG funds have also seen some outflows in recent weeks during this bear market, however it has not been as drastic as non-ESG funds.

EUR IG ESG fund flows vs non-ESG fund flows

ING, EPFR

This is another small piece in the jigsaw contributing to ESG outperformance in the long run

The ECB tilting its index towards corporates with better climate performance will likely mean more outperformance of ESG in the future. But for now, too many questions remain. We will likely see little benefit in 2022, as there will really only be two tradeable months (October and November), as well as the lower reinvestment levels. But long term, this will contribute to the ESG market. It will be another reason for issuers to set and achieve strong ESG goals, thus growing the ESG market. We expect to see the greenium increase, as demand for ESG debt will rise. Much like we saw during the Covid-19 crisis, the majority of inflows that retrace will likely be into ESG funds. Therefore, we do expect ESG outperformance overall in the long run.

Collateral framework – penalizing polluters A new limits regime for polluting corporate exposures

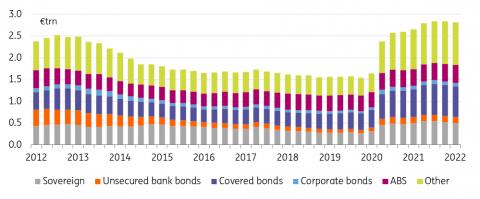

For the purpose of its collateral system, the ECB will introduce a new limits regime, restricting the share of assets issued by entities with a high carbon footprint that can be pledged as collateral. At first, these limits will only be applied to the marketable debt instruments of non-financial corporations, such as corporate bonds. This will comprise just a small portion of all the assets that are pledged as collateral, however. After all, corporate bonds only make up 22% of the marketable debt used as collateral with the ECB. The new limits regime may be expanded to other asset classes at a later stage though as the quality of climate-related data improves.

Corporate bonds are not most prominently used as collateral at the ECB

ING, ECB

Details, including the timelines, have yet to be announced. This leaves the market for now still guessing the exact metrics and limits the central bank will use regarding a company's carbon footprint. Will the central bank base these limits on a company's disclosures of its Scope 1, 2 and 3 GHG emissions versus its enterprise value? Would the future extended environmental taxonomy for significantly harmful activities and the potentially related disclosures play a role for the purpose of the ECB's limits regime?

These specifics still have to be published. The ECB does anticipate however that the new limits regime will apply before the end of 2024 if the necessary technical preconditions are in place. The Eurosystem will offer banks the opportunity to prepare though, by running tests of the new limits regime ahead of its implementation.

Climate change risks as part of haircut reviews

Besides, as of this year, the ECB will also consider climate change risks when reviewing the haircuts applied to corporate bonds used as collateral. Details on the 'how exactly' have not been announced yet. Exposures to companies with a less negative environmental footprint will likely receive more favourable haircuts than companies with a stronger carbon footprint going forward. This should be a modest performance positive for such companies. It is still uncertain though. Will the disclosed Taxonomy KPIs play a role, or will ESG ratings be taken as a reference for the determination of such haircuts, etc?

When it comes to haircut reviews, the ECB also appears to be focusing on corporate exposures first. However, to have a more meaningful impact, these climate change risk considerations should ultimately be reflected in the haircuts of other bond asset classes accepted as collateral, such as covered bonds and preferred senior bonds. In addition, it will be interesting to see if the ECB at some point decides to differentiate between more and less polluting exposures, not only on a company level but also on a bond level. In this regard, one could still think of a more favourable haircut treatment for green bonds issued in line with the forthcoming European green bond regulation.

Collateral acceptance will be linked to compliance with the CSRD…

Importantly, the ECB also anticipates accepting as collateral in 2026 only marketable assets and credit claims from companies and debtors that comply with the Corporate Sustainability Reporting Directive (CSRD) once the directive is fully implemented. This applies to companies in scope of the CSRD, which includes all large (financial and non-financial) corporations and all listed corporations (excluding listed micro-enterprises). The ECB will run test exercises a year ahead of the actual implementation to encourage stakeholders to align with the new rules at an early stage. The importance of this measure is foremost to improve disclosures and generate better data for e.g financial institutions and investors. As such, this measure should mainly be seen as a disclosure incentive, which from a collateral acceptance point of view will not have much of a differentiating performance impact on or among the assets from corporations that do meet these disclosure requirements.

…but ECB hints at separate disclosures for covered bonds and securitisations

The ECB acknowledges that a significant proportion of the assets that can be pledged with the Eurosystem for collateral purposes, such as asset-backed securities and covered bonds, do not fall under the CSRD. To ensure a proper assessment of climate-related financial risks for those assets as well, the ECB says it will support better and harmonised disclosures of climate-related data, and engage closely with the relevant authorities to make this happen. Where covered bonds are concerned, this suggests that the ECB may not find the CSRD disclosures, to be made on the level of the issuing or parent bank entity, sufficient for a proper climate-related risk assessment.

In this regard, it is good to be aware of the developments in the field of securitisations. Think for instance of the ESAs Joint Consultation Paper on STS securitisations-related sustainability disclosures of 2 May 2022, which sets information standards on the principal adverse impacts on sustainability factors of assets financed by the underlying exposures of securitisation notes. The EBA also published a report on the development of a framework for sustainable securitisations on 2 March 2022. In this report the EBA proposes amendments to the EU green bond standard for securitisation transactions, that would allow for a use of proceeds approach at the level of the loan originator, not at the level of the issuer (ie the SPV). Against this backdrop, the EBA does see merits in separate green disclosure requirements for the assets securing the securitisation transaction on top of the disclosure requirements applicable to the green loan portfolio financed with the proceeds of a green securitisation note. Besides, when it comes to a further evaluation of a separate green securitisation framework, the EBA would favour a holistic view of all asset-backed securities, including covered bonds, before a framework would be developed for green securitisations alone.

This suggests that ESG disclosures will remain a topic of further debate, not only for securitisation transactions but possibly also for covered bonds, including at the ECB.

Risk assessment and management – climate risks and ratings

The ECB also aims to further enhance its risk assessment tools and capabilities to better include climate-related risks. For this purpose, the central bank will urge ratings agencies to become more transparent on how they incorporate climate risks into their ratings and to be more ambitious in their disclosure requirements on climate risks. This should improve the external assessment of climate-related risks.

Meanwhile, the Eurosystem also agreed on common minimum standards on how the in-house credit assessment systems of national central banks should include climate-related risks in their ratings. These standards will come into force by the end of 2024.

The ECB's climate agenda 2022

The ECB has three strategic objectives on climate change:

- Manage and mitigate financial risk of climate change and assess its economic impact.

- Promote sustainable finance to support an orderly transition to a low carbon economy.

- Share its expertise to foster wider changes in behaviour.

These objectives are put into action through a focus on six priority areas:

Assess the macroeconomic impact of climate change and mitigation policies on inflation and the real economy. Improve the availability and quality of climate data to better identify and manage climate-related risks and opportunities. Enhance the climate change-related financial risk assessment. Consider options for monetary policy operations and assess the impact of climate change on monetary policy. Analyse and contribute to policy discussions to scale up green finance. Increase transparency and promote best practices to reduce the environmental impact. Monday's announcements primarily cover priority area four, which focuses on:

The introduction of climate change-related disclosures as an eligibility requirement in the collateral framework and asset purchases. Climate change-related risks in the collateral framework and the consideration of related policy proposals. The consideration of climate change in the corporate sector asset purchases. The assessment of the impact of climate change on the monetary policy stance and transmission mechanism. The ECB's review and evaluation of the climate change-related risks in credit ratings and the development of minimum standards for the in-house credit assessment systems are also part of the central bank's priority area three.

The details published on Monday are all part of the ECB's work on its roadmap of climate-change-related actions announced in July 2021.

MENAFN05072022000222011065ID1104482052

Author:

Timothy Rahill, Maureen Schuller, Jeroen van den Broek