(MENAFN- ING)

US retail sales plunged in December on consumer caution resulting from the Omicron wave and the squeeze on real incomes due to surging inflation. January movement and dining data isn't offering much encouragement for a swift turnaround. We are likely to see growth expectations cut although the market still thinks the Fed will hike rates in March

In this article - Broad based declines on Omicron fears and income squeeze

- Downside risks for GDP growth

- 2Q rebound still likely while Fed remains focused on inflation

Share

Download article as PDF

Newsletter

Stay up to date with all of ING's latest economic and financial analysis.

Subscribe to THINK

| -1.9% | Retail sales fall in December

Month-on-Month |

| Worse |

Broad based declines on Omicron fears and income squeeze

Weaker auto sales and a drop in restaurant dining meant the market was looking for a modest fall of 0.1% in December retail sales, but instead we got a 1.9% MoM plunge. Today's evidence suggests that the Omicron wave has had a more damaging impact on Americans' willingness to go out and spend money than most thought likely, while high inflation may also have contributed to more cautious consumer attitudes.

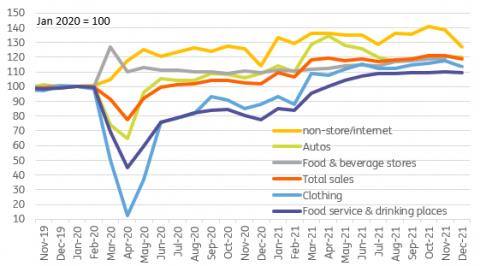

In terms of the major weakness, it was surprisingly led by non-store retail, which saw an 8.7% MoM drop after a 1.5% decline in November. We had thought this would be an area of strength given Covid fears might have led to more of a switch from physical stores to online. In the end, it seems the majority of stores took big hits in December with furniture falling 5.5%, clothing dropping 3.1%, sporting goods falling 4.3% and department stores seeing sales drop 7%. Only building materials (+0.9%), health (+0.5%) and miscellaneous (+1.8%) experienced a rise.

Retail sales index levels versus pre-pandemic sales

Macrobond, ING

Downside risks for GDP growth

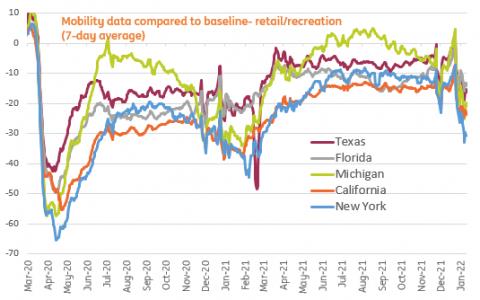

This means that the“control” group for retail sales, which excludes the volatile auto, food service, building materials and gasoline station sales, and typically better matches broader consumer spending trends, fell 3.1%MoM. As such we are likely to see downward revisions to 4Q GDP forecasts. Movement and dining data for January are even worse than December so I wouldn't expect a massive turnaround in next month's retail sales report. We had already cut our 1Q GDP forecast from annualised growth of 4.5% down to 1.3%, but even this may be a little optimistic unless we see a massive turnaround in spending for February and March.

People movement continues to fall in January

Macrobond, ING

2Q rebound still likely while Fed remains focused on inflation

The one crumb of comfort is that retail sales are still 19% above pre-pandemic levels and employment and wages are rising. Although incomes are failing to keep pace with the cost of living right now we expect inflation to subside through 2022 and real income growth should turn positive in the second half of the year.

It may bring a little more doubt on the March Fed rate hike story, but the hope is that based on South Africa and UK numbers we will see the Omicron wave fade and activity will rebound sharply in 2Q. Moreover if we get a strong reading for the employment cost index on January 28th it will be difficult to argue against a March rate hike given embedded inflation fears.

MENAFN14012022000222011065ID1103542121

Legal Disclaimer:

MENAFN provides the information “as is” without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the provider above.